The report: The Fintech Effect

Published: November 2023

Source: Plaid

Why we picked it: Fintech apps have become a fundamental part of finance, no longer innovative in themselves. In fact, 13% of American consumers surveyed by Plaid say that they use six or more financial apps to manage their finances. Another 34% use between three and five.

Banks need to fight hard for share of screen. Nearly 79% of just over 2,000 consumers use some form of fintech app and almost 37% consider themselves to be heavy fintech users. Plaid projects that by mid-2024 one out of five consumers will be using six or more financial apps.

Payment apps are the most widely used, tapped by three quarters of the 2023 sample.

In a time when speculation continues about an American superapp, these figures suggest two things.

• First, the consumers aren’t waiting for someone to create the ultimate financial package, but instead are assembling their own from the available digital buffet.

• Second, banking institutions must move past the mindset of apps being an “alternate channel.” The report indicates that 56% of consumers say they rely on digital financial tools to deal with economic factors, such as inflation. This is even higher for Millennials (71%) and Gen Z (65%). The apps have become the channel for many.

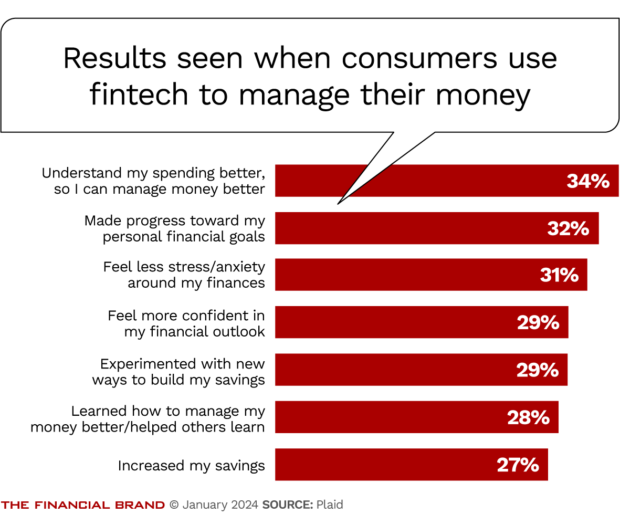

The key evolution? Fintech apps are more than a means of accomplishing financial transactions. Increasingly, consumers told Plaid, they look to apps for education about their finances, including understanding of existing and new opportunities.

At the end of each short chapter in the report, Plaid recommends action steps for fintech companies. Most of these can easily form a handy to-do list for banks and credit unions as well.

An example: “With so many consumers having multifaceted goals, you can turn your app into a financial hub by addressing multiple needs.”

Read more: Stop Fretting About Musk’s ‘Superapp’: Just Make Your Own App Better

Executive Summary

Consumers’ use of fintech apps serves as the hub of the report, but the spokes comprise nine eclectic ways that consumers relate to financial services today.

The unifying theme is that the typical consumer’s financial life has become much more complex, and digital tools can help handle it.

“In essence, fintech solutions aren’t just digital alternatives to traditional finance tools,” according to the report. “They’re transforming everything about how today’s consumers manage their money.”

The nine ways mentioned include:

- Consumer interest in pay-by-bank transactions.

- Consumers’ belief that credit scores don’t solely depict their creditworthiness.

- Fintech’s role in financial inclusion.

- The desire to use fintech to learn more about finance.

- The nearly general comfort with fintech offers.

- Consumers’ shift towards traditional investments and away from crypto products.

- Consumers’ growing reliance on fintech apps to cope with inflation.

- Fintech app’s central role in personal finance.

- How consumers want generative AI to help them, financially — and what controls they want to see on AI.

Quotable: “Up until now, helping consumers manage their finances has largely meant giving them a better perspective of their financial situation, projecting cash flow, and helping them reach their financial goals. Based on this year’s survey, we’re seeing a growing appetite for more financial education and support for things like navigating high inflation and sticking to a budget.”

Key Takeaways

• Nearly 70% of consumers would be willing to try pay-by-bank, even when credit and debit cards are an option for a transaction. Consumers tend to prefer cards for e-commerce, but have already developed a preference for pay-by-bank for recurring household bills. Four additional top uses: sending money to someone; investing; purchasing a big ticket item; and paying for recurring subscriptions. The report says that consumers want more direct links between their accounts and the people they pay, in part to reduce fraud.

• The study reports that 86% of consumers see the benefits of using pay-by-bank. The leading reasons are convenience (32%), security (30%), avoiding extra fees (24%) and ease of tracking expenses (23%).

• While 72% of white consumers have embraced digital tools, 86% of Hispanic Americans use them. Usage by other minorities is slightly higher than whites’: 75% for Asians and 76% for Blacks.

• Consumers say the top five factors keeping them from achieving their financial goals are inflation (54%), insufficient income (29%), poor spending habits (26%), debt (25%) and lack of knowledge (19%).

• Six out of ten consumers would be willing to share their banking data to supplement their credit score, to give a more accurate picture of their ability to repay a loan.

• Just over half — 51% — of the sample want their fintech apps to help them to be more accountable and disciplined in the way they handle money. This even includes accepting restrictions on withdrawing money prematurely.

Read more about mobile apps:

- Offer ‘Test Drives’ of Mobile Banking Apps for a Marketing Advantage

- What Small Businesses Want from Mobile Banking Apps (But Don’t Get)

- Trends 2024: Banks Must Ramp Up Protections as Mobile Fraud Grows

Our Take

What we liked: The overall tone in the report that suggested that it’s time for next-generational thinking even among yesterday’s disruptors. Financial apps are due for fresh innovation.

Honorable mention: Interspersed through the report are a handful of one-page mini case studies about fintechs solving customer problems with data in some way. Several of these were new faces to us and piqued our interest. One in particular is financial tracker Copilot, which charges $95 a year (“No ads, hidden fees, or shenanigans.”) Each case study was linked to a deeper treatment plus a capsule video about the fintech, focusing on a single executive interviewee.

What we didn’t like: One of Plaid’s key roles is connecting banks to fintechs and vice-versa. Something we would have liked to see is a suggestion to create focused apps that can work across fintech offerings, especially in the payment area. Specifically, what we are thinking of is an app that would track buy now, pay later transactions across multiple providers, to help repeat users to understand what they owe all told. A consultant shared the idea with us three years ago but it’s gone nowhere that we’ve seen.

Things that made us go “Hmm”: Besides the survey, the report mentioned another phase of the research involving five-day digital diaries with follow-up interviews. There were only 16 of these, so some sort of anonymized appendix would have been doable, it seems. A peek into the diaries would have been illustrative and useful.

Read more: Personal Financial Management Is the Next Must-Have for Mobile Banking Apps

Consumers Like the Idea of AI Help But Some Still Want Control

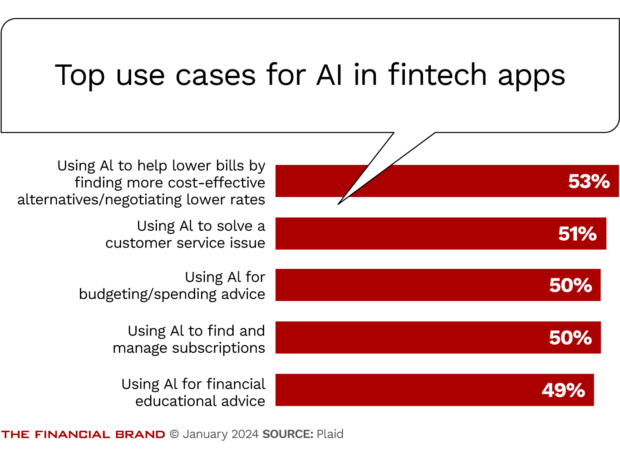

Six in 10 respondents think AI will revolutionize fintech by 2030, with Millennials and Gen Z especially interested in the technology’s potential. The chart below summarizes the top benefits that consumers anticipate.

Quotable and Notable:“Consumers aren’t ready to get out of the driver’s seat just yet. Three-fourths (78%) of heavy users and Gen X (75%) say they want to be able to review any AI decisions around their finances. And 7 out of 10 Americans (70%) want to see regulation around AI in general.” (Emphasis added.)

One respondent quoted in this section of the report was OK with using AI in fintech so long as the provider made it clear where personal data was coming from.