A substantial portion of U.S. small businesses surveyed no longer see their primary financial institution as a partner and they don’t feel that their provider understands their needs. As a result 14% say they will definitely or probably switch financial institutions in the next two years. And 36% report they are thinking about moving, according to a study of more than 1,000 small businesses by Aite Group for Alkami.

“Three out of five respondents have already gone beyond their primary financial institution to obtain financial services that they need.”

Considering how much more complex it can be to unwind a business banking relationship compared to a consumer relationship, those numbers should be sobering. That’s especially so when contrasted with a retail banking study reported by The Financial Brand in which only 5.3% of U.S. consumers said they were considering switching institutions and 16% more indicated that they were considering a move — less than half of the small business survey’s switchers and potential switchers.

Indications in the Aite/Alkami study are that efforts to further “consumerize” small business banking services are actually headed in the exact opposite direction that small business leaders would prefer — homogenous offerings for all small firms go against their desire for something better than “one size fits all” service. They want offerings that change with their needs and size.

In addition, there’s a major disconnect with traditional institutions as a whole failing to comprehend small firms’ desire for better banking technology. And many say banks and credit unions as a group just don’t move fast enough to improve their offerings, especially in mobile services.

But these firms can do their own moving, voting with their feet. Traditional players already face a loosening of connections with small firms and those that don’t adopt carefully considered strategic changes may find themselves losing their share of small business customers as more and more come to be owned by Gen Xers and Millennials. Three out of five respondents have already gone beyond their primary financial institution to obtain financial services that they need, including fintechs among the suppliers of those services.

The only bright spot here: If a traditional institution has an up-to-date lineup of services that can be tailored to a firm’s needs, they stand a good chance of picking up new customers from among the 50% that are at least thinking about switching.

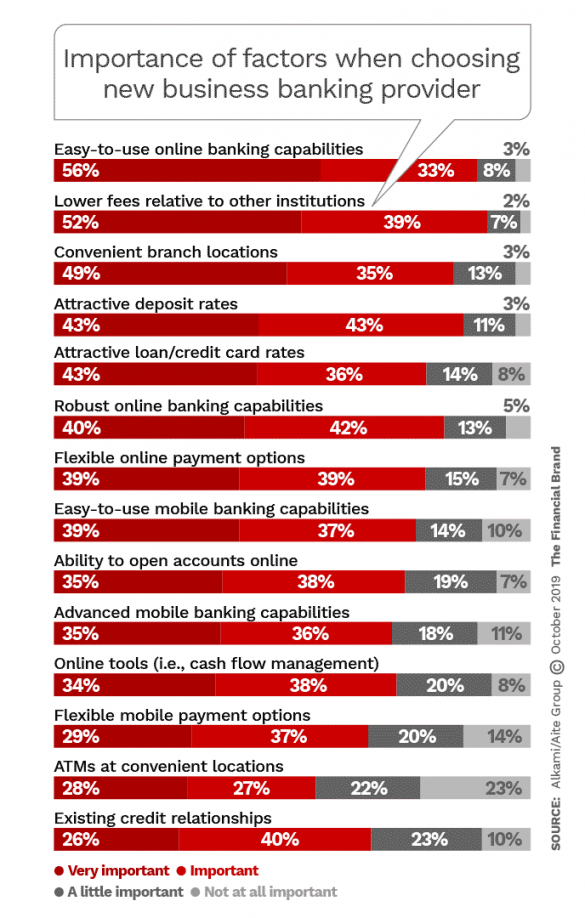

Tech Will Make or Break Small Business Banking

The study found that while many longstanding factors play a part in small firms’ search for new providers, desire for strong technology plays a major role.

The report notes that small businesses whose leaders have a bent for technology make up a big portion of the likely and potential switchers. States the report:”Tech-savvy clients tend to be less expensive to serve since they are more inclined toward self-service and less-expensive digital channels. They also serve as a strong target market for new value-added digital tools from which financial institutions can generate fee-based revenue and offer their institutions greater cross-sell potential.”

Further, according to the report, Millennial-run businesses make up 34% of those firms that definitely or probably will switch.

“This segment represents banks’ and credit unions’ future, and thus is a group they want to hold onto,” says the study.

Many Firms Think Banks and Credit Unions are Out of Touch

The survey found that 40% of the smallest businesses — those generating $100,000 to $999,999 in annual revenue — and 61% of the larger ones — those generating between $10 million and $20 million — don’t think their bank or credit union fathom what they are about or what they need. In between those sizes, the larger the firm, the less likely their provider understands them.

While the size of the bank or credit union serving the responding business had some bearing on this feeling, significant dissatisfaction was seen across the board. Among those banked by the big four banks — Bank of America, Citi, JPMorgan Chase and Wells Fargo — just over half, 52%, don’t think their needs are understood. And 43% of super regional bank customers and 50% of regional bank customers likewise don’t feel understood.

While community bankers often feel closest to small businesses, a disturbing warning comes in this research. Over a third of the sample served by community financial institutions — 35% — don’t believe their providers understand them.

Among the reasons respondents feel this way:

- Square peg problem. Many financial institutions still try pushing small businesses into consumer banking platforms that don’t include business-specific services. “There is no doubt that small businesses are growing in sophistication and that, for most, their needs more closely mirror those of commercial clients than consumers,” the report states.

- Unfriendly user experience. The study found that many firms feel that financial institutions emphasize functionality for their own purposes over usability through a good user experience. Many keep offering “older, less user-friendly online banking platforms.”

- Evolving like a glacier. While the offerings of fintechs reaching out to small business keep growing, traditional players seem stuck. “Financial institutions are undergoing a slower-than-needed evolution of strategies and product offerings,” states the report.

- Why ask customers? Small firms say institutions don’t communicate much with them about current offerings and planned offerings. The customers rarely have any input on product design.

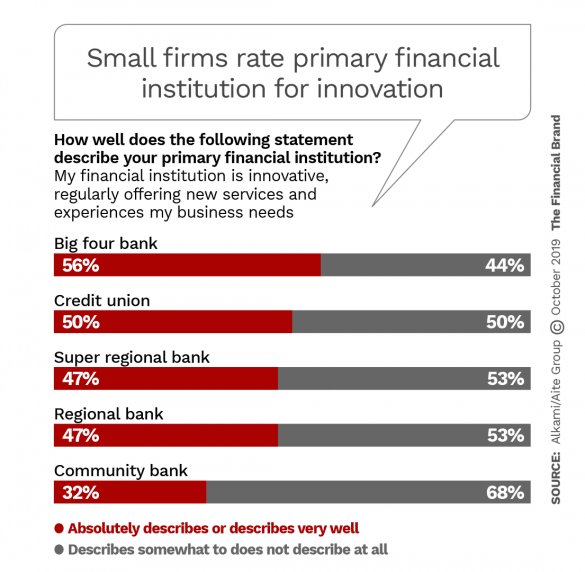

Overall, small businesses see many traditional institutions as failing to be innovative in their offerings. Credit unions ranked higher for innovation ahead of all institutions except for the biggest banks, and they only beat the credit unions by six percentage points.

Read More:

- Alternative Lenders Continue to Steal Business From Banks

- Don’t Kill Business Banking Relationships With Digital

- Five Banks and Credit Unions Rocking The Small Business Market

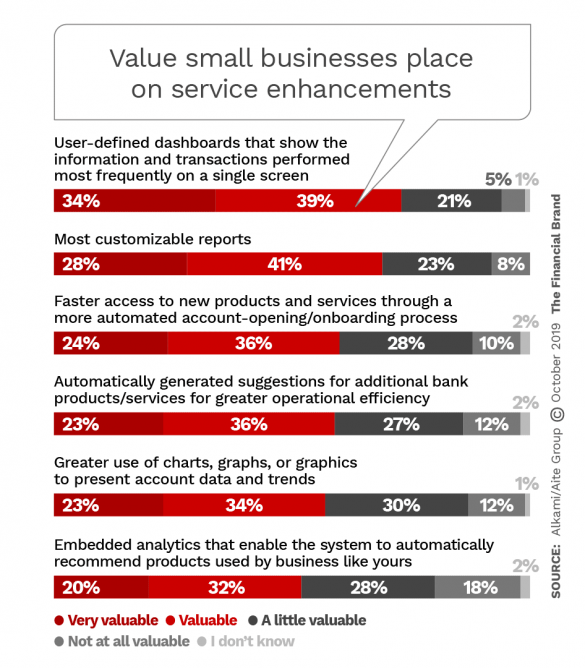

Increasingly Small Firms Want Heavy-Duty Banking Data

There’s a sense in the study that many institutions still think they are serving the same principals of small firms that they were a decade or more ago. Even though many institutions remain believers in branches because they think small businesses want branches, that preference is more limited than some might think, the survey found. Branches have a leg up in terms of deposits and applying for business credit, but not by much. Among the sample, applying for credit at a branch was favored by 38% of the sample, but 32% preferred to apply online and 11% wanted to do so via smartphone or tablet.

The study also found a strong appetite for services that would help small businesses to better understand their own banking data and how to act on it. The report states that many banks and credit unions are seen as not keeping up with what small firms want in this area.

“Financial institutions’ opportunities for differentiation are often less about the core banking products, which most institutions offer,” says the report, “and are instead more about how the information from those products is delivered.” Larger small businesses and firms run by Millennials and Gen Xers particularly value greater use of data analytics.

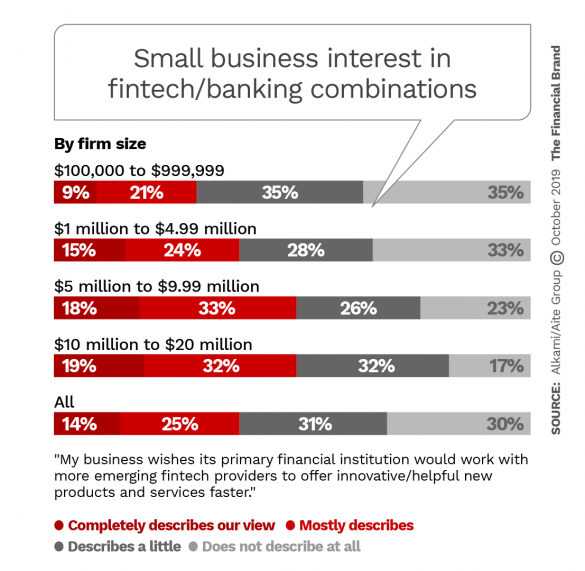

The survey report notes that while some banks and credit unions favor partnerships with fintech firms, many still see them as competitors. Meanwhile, the study found that many small firms see partnerships as a good solution to their needs.

Read More:

- Tech-First Startup Bank Aims to Wipe Out Customer Pain Points

- If You Launched a New Bank Today, What Would It Look Like?

- 5 Ways Traditional Business Lenders Can Beat Digital Disruptors

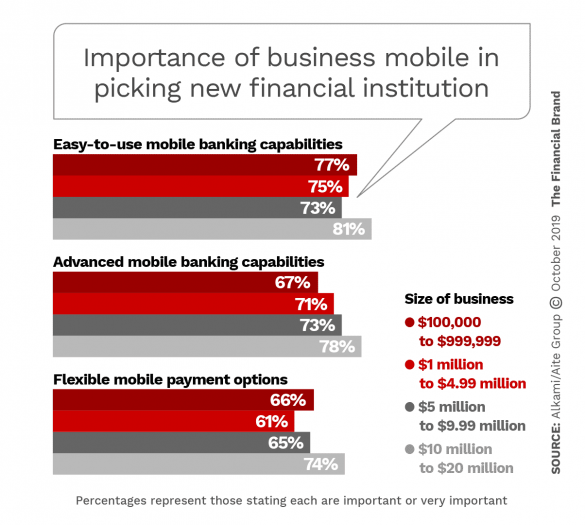

Mobile Plays Huge Role in Perception of Traditional Institutions

There’s a potentially valuable nugget in the report that should draw the attention of financial marketers. Zelle, the person-to-person payments product offered by traditional players, has not only been booming among consumers, but it has made strides among small businesses as well, the survey found.

The study asked about interest in online banking capabilities and 26% of the sample said that they were already using Zelle for real-time payments. Another 30% said they would be interested in using it.

That underscores the study’s finding that mobile banking features will grow increasingly important for serving small businesses. Large portions of the respondent base place major stress on mobile banking capabilities.

The study found that 26% of all respondents use mobile banking for business to some degree already, and that 33% would “definitely or probably” use it if their primary financial institution offered it.

The report suggests that institutions that offer bare-bones mobile because they don’t think small firms need more should consider upgrading.

“Many banks recognize the importance of checking balances, making and approving certain types of payments, and making deposits,” the report states, “but they underestimate the importance of incorporating mobile alerts and leveraging mobile devices for authentication.”

The research found that many respondents prefer to receive account notifications and alerts on their mobile devices.

As Millennials take over more companies, the report says, they will increasingly favor institutions that offer a full business mobile menu.

“They expect a new kind of digital experience, which most financial institutions do not yet offer,” the study says, “that favors their preferences for self-service, mobile access, real-time capabilities, and instant gratification.”