“Tumultuous” doesn’t do justice to the events that unfolded over the course of just a few days in March, shocking the banking industry.

And to adapt a quote from Winston Churchill, we may not even be at the end of the beginning. In remarks concerning the events, President Joe Biden said he would ask Congress and federal banking regulators to “strengthen the rules for banks to make it less likely that this kind of bank failure will happen again and to protect American jobs and small businesses.”

The collapse of Silicon Valley Bank, the nation’s 16th-largest bank, on Friday, left many in banking with increasing unease over a long weekend of question marks. It was accentuated when the Federal Deposit Insurance Corp. took over Signature Bank on Sunday.

But federal authorities unveiled an extraordinary response to those two failures, saying all deposits at those banks, most of them uninsured, would be fully covered and available as soon as Monday.

They also introduced a program to add to industry liquidity and quell the potential for widespread panic.

Here’s a more detailed timeline of the fast-moving events that sent multiple banks into a spiral, in what is perhaps the most momentous week in banking since the autumn of 2008.

The timeline also details the fallout, which includes a historic emergency response from federal agencies.

- Silvergate, Then Silicon Valley Bank, Then Bigger Trouble

- Deposit Run Topples One Bank, Threatens Others, as Panic Spreads

- Regulators Take Emergency Action to Restore Confidence

- The White House Promises Stiffer Regulation and Supervision

- From Washington to Main Street

- From Washington to Wall Street and Beyond

- Another Day Begins in the SVB Case

- A Day Marked by Major Bank Cooperation Amid Industry Stress

- First Capitol Hill Inquiry into SVB and Signature Bank Failures Announced

- New York Institution Acquires Most of Signature Bridge Bank Deposits

- Second Week of Banking Turmoil Begins

- Treasury’s Yellen Talks Deposit Insurance with Bankers at ABA Summit

- Citigroup’s Jane Fraser Shares Some Behind-the-Scenes Crisis Insights

- FDIC Finds Buyer for Silicon Valley Bank Deposits and Loans

- Federal Reserve and FDIC Testimony for Senate Banking Committee Hearing Revealed Early

- First Republic Goes to JPMorgan Chase via FDIC Deal

Silvergate, Then Silicon Valley Bank, Then Bigger Trouble

Wednesday, March 8:

• Silvergate Bank in La Jolla, Calif., announced its intent to wind down operations and voluntarily liquidate.

A crypto specialist, Silvergate had been thrown into turmoil when fraud caused FTX, a high-flying crypto exchange and hedge fund co-founded by Sam Bankman-Fried, to collapse in the fall. The trouble sent many of Silvergate’s crypto customers scrambling for liquidity, and the deposit drain had forced Silvergate to sell securities at huge losses.

It could not recover.

• In a case of extremely poor timing, this was the same day that Silicon Valley Bank in Santa Clara, Calif., announced it had to take a $1.8 billion loss on the sale of $21 billion of U.S. treasuries and mortgage-backed securities. It also announced plans to raise capital.

The tech startups that make up much of the San Francisco bank’s customer base have been burning through cash and drawing down their deposits. To cover those withdrawals, the bank had to sell off some of the bonds it had invested in.

The announcement took the market by surprise, and the venture capital firms that also had been Silicon Valley Bank customers saw danger. The bank had more securities with unrealized losses, and now would have to mark them down.

The VC firms began to urge the startups in their portfolios to withdraw their cash from Silicon Valley Bank, and word spread quickly across social media.

Thursday, March 9:

• Silicon Valley Bank executives tried in vain to reassure both depositors and investors. By the end of the day, $42 billion of deposits had been withdrawn from the bank.

Deposit Run Topples One Bank, Threatens Others, as Panic Spreads

Friday, March 10:

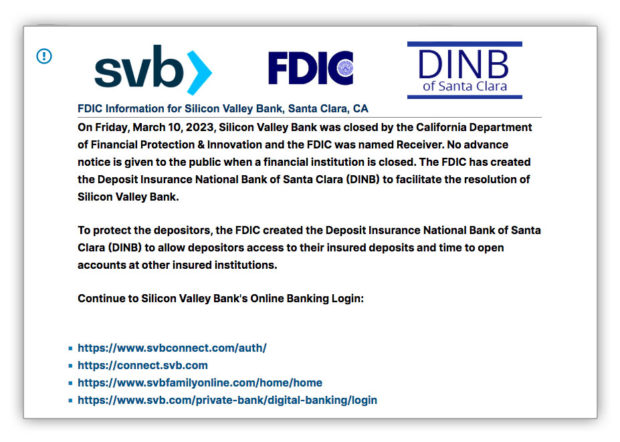

• The $209 billion-asset Silicon Valley Bank was closed Friday morning California time by the state Department of Financial Protection and Innovation. FDIC was named receiver.

In a terse “findings of fact,” the state regulator recounted that on March 8 the bank announced a $1.8 billion loss from the sale of investments and a plan to raise capital.

“Despite the bank being in sound financial condition prior to March 9, 2023, investors and depositors reacted by initiating withdrawals of $42 billion in deposits from the bank on March 9, 2023,” the regulator’s statement said. “The bank is now insolvent.”

The takeover early in the day is an indication of the speed of Silicon Valley’s collapse. Regulators typically wait until after the close of business on Friday to announce a bank failure.

• FDIC set up a “Deposit Insurance National Bank,” a mechanism used to handle a failed bank when an immediate full or partial acquisition by another institution is not arranged to coincide with the closure.

• The FDIC said that insured deposits would be available Monday and that it would issue certificates for the uninsured deposits over $250,000.

An estimated 93% of Silicon Valley Bank’s deposits were uninsured — a reflection of its unusual customer base.

The certificates would allow depositors to potentially be paid later, based on how much the FDIC could recover when disposing of the remnants of Silicon Valley Bank.

This sent many startup founders spiraling, as it put millions in funding they had raised for their companies at risk. Some said their immediate concern was whether they could even make payroll in the coming week.

• A handful of other large regional banks with concentrations in the tech sector and wealth management — and large amounts of uninsured deposits — came under so much pressure that trading of their stocks was halted during the day because of volatility.

• This included First Republic Bank in San Francisco, which lost as much as half of its stock value early in the day. (It later rebounded to close the day down 15%.)

In a Securities and Exchange Commission filing and in a post on the homepage of its website, the $213 billion-asset First Republic, the nation’s 14th-largest bank, sought to reassure depositors and investors. Its note recounted its diversified deposit base, its borrowing capacities with the Federal Home Loan Bank System and the Federal Reserve, and the quality and accounting status of its investment portfolio. Later this was followed by additional notices on the homepage highlighting its capital status and an FAQ on FDIC insurance. Then, on Sunday, March 12, the homepage displayed a letter to customers emphasizing the bank’s strength.

• Western Alliance Bank in Phoenix and Pacific Western Bank in Los Angeles also saw their stocks fall. Both issued press releases containing unaudited, updated numbers and reviewing their capital and liquidity strategies. The $68 billion-asset Western Alliance ranks as number 40 and the $41 billion-asset PacWest as number 53 among banks in terms of asset size.

• Silicon Valley Bank customers started to disclose how much money they had there in the form of uninsured deposits and to worry aloud about their ability to make payroll.

Saturday, March 11:

• Social media continued to churn with dire predictions, as billionaires like Bill Ackman and Mark Cuban called on the government to act quickly to avoid a slew of bankruptcies and job losses at companies in the tech sector.

Some raised concerns about the ripple effects of Silicon Valley Bank’s failure on the future of innovation in America.

There were also indications that other institutions — including fintechs like Jiko — were attracting business from those that had succeeded in withdrawing their money from Silicon Valley Bank. Still other institutions were ramping up to reel in customers of the failed bank.

Regulators Take Emergency Action to Restore Confidence

Sunday, March 12:

• Federal officials finally began to speak out on Sunday morning news talk shows, following what had been near silence after the FDIC took over Silicon Valley Bank on Friday.

In an appearance on CBS’ “Face the Nation,” Treasury Secretary Janet Yellen said: “We want to make sure that the troubles that exist at one bank don’t create contagion to others that are sound. We are concerned about depositors and are focused on trying to meet their needs.”

• In the early evening, the New York State Department of Financial Services announced that it had closed Signature Bank and appointed FDIC as receiver.

Just a few months earlier, the $110 billion-asset Signature, the nation’s 29th-largest bank, had announced that it would be shrinking its exposure to companies in the crypto sector. It also was known for serving law firms and real estate companies.

Like Silicon Valley Bank, most of its deposits (roughly 90%) were uninsured, as it served mainly businesses and wealthy people.

Signature had been slammed with deposit withdrawals on Friday, and its stock ended the day down 23%.

• In a joint statement, the Federal Reserve, the FDIC and the Treasury Department announced that they were “taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system.”

One facet of the response is that systemic risk exceptions will be made for the Silicon Valley Bank and Signature Bank resolutions. In both cases, all depositors — insured and uninsured — will be made whole. All of their money will be made available to them as soon as Monday.

This will be done at no cost to taxpayers, according to the joint announcement. Any loss to the FDIC Deposit Insurance Fund will necessitate a special assessment on banks, according to the press release. Shareholders and certain unsecured debtholders will not be protected, and senior management of both institutions has been removed.

• The trio of federal agencies also announced the Bank Term Funding Program. This makes additional funding available to financial institutions so that they’ll have the ability to provide deposits on demand when needed.

“The Federal Reserve is prepared to address any liquidity pressures that may arise,” the statement said.

The new program will offer loans of up to one year to banks, savings associations, credit unions and other eligible depository institutions. Loans will be secured by such collateral as Treasuries and mortgage-backed securities.

The program will be backstopped by the Treasury’s Exchange Stabilization Fund.

• The FDIC transferred all the deposits and substantially all of the assets of Signature Bank to a new entity called Signature Bridge Bank, a full-service bank that will be operated by FDIC as it markets the institution to potential bidders.

Greg Carmichael, the former president and chief executive officer of Fifth Third Bancorp, will serve at CEO of the bridge bank.

• First Republic Bank announced that it will avail itself of the brand-new Bank Term Funding Program. It will have access to additional funding from JPMorgan Chase, the nation’s largest bank, and continued funding through the Federal Home Loan Bank System.

• In the wake of the federal announcements, President Joe Biden issued a statement. In part it said: “The American people and American businesses can have confidence that their bank deposits will be there when they need them. I am firmly committed to holding those responsible for this mess fully accountable and to continuing our efforts to strengthen oversight and regulation of larger banks so that we are not in this position again.”

The White House Promises Stiffer Regulation and Supervision

Monday, March 13:

• President Biden gave brief remarks in the morning recounting the federal response of the weekend. He called for action to “make it less likely this kind of bank failure would happen again.” He said he will ask Congress and the regulators to strengthen rules on the banking industry.

“During the Obama-Biden administration, we put in place tough requirements on banks like Silicon Valley Bank and Signature Bank, including the Dodd-Frank Law, to make sure the crisis we saw in 2008 would not happen again,” said Biden. “Unfortunately, the last administration rolled back some of these requirements.”

He also stated: “We must get the full accounting of what happened and why those responsible can be held accountable.”

“No one is above the law,” he said.

• The views from Capitol Hill

• Sherrod Brown (D.-Ohio), chairman of the Senate Banking Committee, and Maxine Waters (D.-Calif.), ranking member of the House Financial Services Committee, issued a joint statement March 12, saying in part: “As we work to better understand all of the factors that contributed to the events of the last several days and how to strengthen guardrails for the largest banks, we urge financial regulators to ensure the banking system remains stable, strong and resilient, and depositors’ money is safe.

• Sen. Tim Scott (R.-S.C.), the ranking Republican on the banking committee, stated that: “Building a culture of government intervention does nothing to stop future institutions from relying on the government to swoop in after taking excessive risks.”

Stated Patrick McHenry, chairman of the House Financial Services Committee, on March 12: “This was the first Twitter-fueled bank run. At this time, it is important to remain levelheaded and look at the facts — not speculation — when assessing the right path forward. I have confidence in our financial regulators and the protections already in place to ensure the safety and soundness of our financial system.”

• Deregulation gets slammed in hindsight

A frequent claim being made by politicians and others in social media and other venues is that the crisis would not have happened if the Trump administration had not engineered the rollback of stringent rules that affected banks the size of SVB and Signature Bank.

A notable step was raising the threshold for the designation of systemic importance from $50 billion to $250 billion in assets. Below the new threshold regulators could “tailor” the regulatory framework to fit varying business models and risk profiles.

This was done through S. 2155, the “Economic Growth, Regulatory Relief, and Consumer Protection Act.” However, Barney Frank, former democratic chairman of the House Financial Services Committee — and the “Frank” in “Dodd-Frank Act — said in media interviews that this legislation had not caused the trouble.

A key detail: Frank was a member of the Signature Bank board of directors and had lobbied for the regulatory reform bill’s passage.

More data isn’t convincing investors, apparently

Keefe, Bruyette & Woods analysts noted after the markets closed on Monday that the intra-quarter updates issued by banks (see earlier items) “are falling on deaf ears.”

From Washington to Main Street

Monday, March 13:

• Selling SVB by the slice? Far, far from Silicon Valley, HSBC Holdings plc announced that its HSBC UK Bank plc subsidiary was acquiring Silicon Valley Bank UK Limited (SVB UK) for £1. (You read that correctly — one British pound.)

• Sand in the gears of FDIC’s sales process? From a March 13 Wall Street Journal editorial: “Rohit Chopra, the Elizabeth Warren acolyte on the FDIC board, is hostile to bank mergers on ideological grounds, and the purchase terms could be too onerous for some potential buyers. The biggest banks are now the safest, and deposits are flooding into them. J.P. Morgan can park that money at the Federal Reserve and earn interest on its reserves. Why take on a new political headache?”

[Editor’s note: Chopra serves on the FDIC board in his role as director of the Consumer Financial Protection Bureau.]

(See The Financial Brand story, “Making Sense of the Silicon Valley and Signature Bank Failures,” for more on how bank rescues and politics get tangled up.)

• For the Fed, humility begins at home. The Federal Reserve Board announced that Vice Chair for Supervision Michael S. Barr — a Biden appointee — will lead a review of the supervision and regulation of Silicon Valley Bank, in light of its failure. The review is slated for release by May 1.

Said Barr: “We need to have humility, and conduct a careful and thorough review of how we supervised and regulated this firm, and what we should learn from this experience.”

Watch out for your next bank exam:

“On the regulatory side, the fallout will play out over time, but it certainly puts a wind at the back of those who want to amend the tailoring regime and subject more regional banks to higher regulatory standards,” said Brian Gardner, chief Washington policy analyst at Stifel, parent of Keefe, Bruyette & Woods in a March 12 podcast. “Even though there won’t be formal changes to the rules for community banks, there’s always a cascading … community banks can expect to see heightened scrutiny from bank examiners.“

From Washington to Wall Street and Beyond

Monday, March 13:

• Key banking voices — and both of Utah’s U.S. senators — took part in a podcast by Silicon Slopes, a Utah nonprofit devoted to promoting the state’s tech sector.

Zions Bancorporation‘s A. Scott Anderson, EVP at the $90 billion in assets company, the nation’s 36th largest bank, noted that while the company has been caught up in the pounding of regional banks in the wake of SVB’s failure, its deposit profile is wholly unlike the failed bank’s heavy uninsured funding.”

“We don’t seek to fill the bank with mammoth wholesale deposit accounts,” said Anderson. He said the company’s funding was diversified by geography, sources and types of deposit.

Anderson stated that Zions was working to onboard former SVB clients who need a new corporate bank.

A new banking maxim? In a quote worth remembering, Howard Headlee, president of the Utah Bankers Association, told listeners:

“If capital is king, then confidence is queen, and the queen in many cases runs the show.”

Headlee blamed the run that put the nail in SVB’s coffin on venture capitalists who advised tech firms they backed to withdraw funds. “The folks who made the phone calls saying, ‘Get your money out,’ killed the bank — a bank that served its industry really, really well,” Headlee insisted.

An economic observation worth noting:

From Dan Wantrobski, technical strategist and associate director of research at Janney Montgomery Scott LLC:

“The Fed is effectively going to expand its balance sheet to backstop both depositors and banks, effectively injecting more liquidity into the system and expanding money supply to accomplish its mission. Although the bank term funding program (BTFP) is scheduled to operate within a finite, 12-month window, we view the weekend developments as an obvious extension of the QE [Quantitative Easing] and rescue operations that occurred during the GFC [Global Financial Crisis] and 2020 pandemic. The difference: the scope of securities protected under the new program has been notably expanded, as the central bank prints more money to allow the marking of discounted collateral to par. This in our view is really an inflationary event…” [Emphasis added.]

• A word from NCUA.“The credit union system remains well-capitalized and on a solid footing,” stated National Credit Union Administration Chairman Todd Harper. “The National Credit Union Administration continues to monitor credit union performance through both the examination process and offsite monitoring, and it will continue to do so into the future.”

Harper noted that credit unions have access to a wide range of liquidity sources: “The NCUA, along with its Central Liquidity Facility, is able to provide a back-up source of liquidity to member credit unions as needed.”

• Something to watch for, from the same Wall Street Journal editorial cited earlier: “Will a universal uninsured deposit guarantee be next? This would be a monumental policy surrender, essentially admitting that the regulatory machinery established in 2010 by Dodd-Frank failed. We may be the only people in the world who still worry about ‘moral hazard.’ But a nationwide guarantee for uninsured deposits, even for a limited time, means this will become the default policy any time there is a financial panic.”

• Silicon Valley Bridge Bank opened its doors. The FDIC named Tim Mayopoulos as CEO of the interim institution. Mayopoulos is former president and CEO of the Federal National Mortgage Association, having joined as part of a team that came in after the financial crisis. He most recently served as president of Blend Labs, a mortgage software fintech. He remains on the board at Blend and also serves on the board of LendingClub, a fintech peer-to-peer lender that now has a banking charter.

A bridge bank is a chartered national bank that operates under a board appointed by the FDIC. It purchases certain assets of a failed bank and assumes its deposits and certain other liabilities. This “bridges” the gap between the failure of a bank and the point when FDIC can implement a permanent resolution.

• Federal Reserve publishes FAQ on Bank Term Funding Program. More details about the special Fed lending program were published in a FAQ document that can be downloaded from the central bank’s new funding program page.

Another Day Begins in the SVB Case

Tuesday, March 14:

• Federal investigations of SVB open. The Wall Street Journal reported this morning that both the Justice Department and the Securities and Exchange Commission have opened investigations of the Silicon Valley Bank failure.

• Bring your money back. That’s the message coming from Silicon Valley Bridge Bank. In a letter on its website, Tim Mayopoulos, the bridge bank’s CEO, wrote: “The number one thing you can do to support the future of this institution is to help us rebuild our deposit base, both by leaving deposits with Silicon Valley Bridge Bank and transferring back deposits that left over the last several days.”

A Day Marked by Major Bank Cooperation Amid Industry Stress

Thursday, March 16:

• First Republic Bank received a $30 billion deposit infusion from 11 major U.S. banks.

In a rare joint statement, the banks said: “The actions of America’s largest banks reflect their confidence in the country’s banking system. Together, we are deploying our financial strength and liquidity into the larger system, where it is needed the most. Smaller- and medium-sized banks support their local customers and businesses, create millions of jobs and help uplift communities. America’s larger banks stand united with all banks to support our economy and all of those around us.”

The 11 banks, and their contributions to the total, are as follows:

- Bank of America: $5 billion

- Citigroup: $5 billion

- JPMorgan Chase: $5 billion

- Wells Fargo: $5 billion

- Goldman Sachs: $2.5 billion

- Morgan Stanley: $2.5 billion

- BNY Mellon: $1 billion

- PNC Bank: $1 billion

- State Street: $1 billion

- Truist: $1 billion

- U.S. Bank: $1 billion

The announcement came out at 3:22 P.M. Eastern Daylight Time, ahead of the closing of the New York stock exchange.

The list accounts for 11 out of the top 15 U.S. banks by asset size as listed by the Federal Reserve based on yearend 2022 data. (First Republic is the 14th institution by assets.)

First Republic Bank’s Jim Herbert, founder and executive chairman, and Mike Roffler, president and CEO, thanked the banks for the support with a statement that said in part: “Their collective support strengthens our liquidity position, reflects the ongoing quality of our business, and is a vote of confidence for First Republic and the entire U.S. banking system.”

Read More:

- Why Silence Isn’t Golden on SVB & Signature Bank Failures

- 3 Effective Tactics to Calm Customer Fears in a Banking Crisis

- 8 Deposit-Raising Tactics You Might Not Be Trying

• Who was the “Mr. Potter” of the Silicon Valley Bank run?

During Treasury Secretary Janet Yellen’s March 16 testimony on the Biden administration’s budget proposal some members of the Senate Finance Committee took advantage of the opportunity to talk about the recent bank closures.

Sen. Sheldon Whitehouse, D.-R.I., focused on the role of social media in starting the run on Silicon Valley Bank deposits. Certain prominent venture capitalists were among the voices beating the drum for withdrawals from the beleaguered bank. He implied they were the “Mr. Potters” of the debacle, in reference to the villain banker of the classic holiday film, “It’s a Wonderful Life.”

“I’ve been supportive of the venture capital community,” said Whitehouse, “… but I think there were some bad actors in the VC community who literally started to spur this run by virtually crying fire in a crowded theater, in terms of rushing all these deposits out.” He said he knew of no restrictions in federal regulation on such speech. He expressed frustration with the social media posters from the venture capital community “who are libertarian until the stuff hits the fan, and then they want relief.” He said this was “more than a little repugnant.”

“This will go down as history’s first internet driven run,” said Whitehouse.

He asked Yellen for her thoughts.

She said that no matter how strong an institution’s capital and liquidity are, an “overwhelming run that’s spurred by social media” could put the bank into danger of failing.

“One of the reasons we intervened and declared a systemic risk exception is because of the recognition there can be contagion in situations like this, and that other banks can then fall prey to the same kinds of runs,” said Yellen.

“But this was a bank that had a very high ratio of uninsured depositors,” she added. “… We tend not to see runs among insured depositors.” She said the vulnerability of banks with heavy reliance on uninsured deposits needs to be examined.

First Capitol Hill Inquiry into SVB and Signature Bank Failures Announced

Friday, March 16:

• House Financial Services Committee sets bipartisan inquiry on SVB and Signature Bank of New York for March 29.

New committee chairman Patrick McHenry, R.-N.C., and ranking committee member Maxine Waters, D.-Calif., announced a hearing into the two failed banks. The two witnesses scheduled so far are Michael Barr, vice chair for supervision, Federal Reserve Board, and Martin Gruenberg, Chairman of the Federal Deposit Insurance Corp.

As previously reported in this Timeline, Barr is leading a Federal Reserve internal investigation of the supervision and regulation of Silicon Valley Bank. His report has been promised by May 1.

The two committee leaders also sent a letter instructing the Government Accountability Office to begin an investigation of the two failures. GAO is “to examine the factors that led to mismanagement of both banks, including any regulatory or examination failures.” They asked GAO to submit an interim report of its findings by April 28.

• President Biden issued a statement on holding executives of failed banks accountable.

Following up on points he made in the wake of federal regulators’ response to the closures of Silicon Valley Bank and Signature Bank of New York, Biden stated: “The law limits the administration’s authority to hold executives responsible. When banks fail due to mismanagement and excessive risk taking, it should be easier for regulators to claw back compensation from executives, to impose civil penalties, and to ban executives from working in the banking industry again.”

He called on Congress to create tougher penalties for senior bank executives “whose mismanagement contributed to their institutions failing.”

• Western Alliance Bank deposits appeared to be stabilizing, per a KBW report and bank announcement.

In a March 17 press release/investor update the bank reported that it “experienced elevated net deposit outflows on Monday, March 13, immediately following the announcement of the Signature Bank closure on March 12, concentrated primarily in our Technology & Innovation group. Since then, net outflows have fallen sharply, with deposit balance fluctuations returning to normalized levels in recent days, including significant inflows and new account openings.”

A March 17 week-end report from bank stock analysts at Keefe, Bruyette & Woods saw this as good news: “This should provide confidence that deposit outflow risk is primarily contained to the tech/innovation deposit portfolio.”

The brokerage firm said its calculations suggest that about 50% of the bank’s tech and innovation group may have run-down, which is consistent with the proportion not subject to lending covenants. (These are deposits that borrowers are required to maintain.) The firm said that tech and innovation deposits now comprise 8% of total deposits versus 14% at the end of 2022.

New York Institution Acquires Most of Signature Bridge Bank Deposits

Sunday, March 19:

• New York Community Bancorp assumes all but crypto-connected deposits of FDIC’s Signature Bridge Bank.

Flagstar Bank, N.A., part of New York Community Bancorp, entered into a “purchase and assumption” agreement with the Federal Deposit Insurance Corp. for most of the deposits and some loan portfolios of Signature Bridge Bank, N.A., the organization created by FDIC to temporarily succeed New York’s Signature Bank. Historically “P&A” transactions are FDIC’s most common way of resolving failed or failing banks.

The former Signature Bank had deposits of $88.6 billion and total assets of $110.4 billion at the end of 2022. Flagstar will acquire all deposits with the exception of $4 billion in cryptocurrency related deposits. (FDIC will work with crypto related depositors.) Flagstar will also $38.4 billion of assets from the bridge bank. Of this amount were loans of $12.9 billion purchased at a discount of $2.7 billion.

Approximately $60 billion in loans will stay in FDIC hands, awaiting disposition. FDIC estimates that resolution of the New York bank’s failure will cost the Deposit Insurance Fund $2.5 billion.

As part of the deal, FDIC received equity appreciation rights in New York Community Bancorp common stock. This could have a value of up to $300 million.

At yearend 2022 New York Community Bancorp was the 35th-largest U.S. bank. At that point it had $90.1 billion in assets and $58.7 billion in deposits. The company completed its acquisition of Flagstar Bancorp in December 2022.

On Monday, March 20, the Office of the Comptroller of the Currency, as regulator of Flagstar, released its approval letter for the deal. It contains some conditions for the transaction.

Read More:

- When ‘Signature’ or ‘Republic’ in Your Name Creates a Marketing Emergency

- SVB Post-Mortem: Communications Lessons Amid the Collapse

Second Week of Banking Turmoil Begins

Monday, March 20:

• Citing strong interest, FDIC extended the deadline for SVB bids.

“There has been substantial interest from multiple parties, and the FDIC and the bidders need more time to explore all options in order to maximize value and achieve an optimal outcome,” the Federal Deposit Insurance Corp. said in a statement.

FDIC has decided that separate bids can be submitted for Silicon Valley Bridge Bank, N.A., and for its subsidiary, Silicon Valley Private Bank. The deadline for bids on the former is now 8:00 p.m. EDT on Friday, March 24. The deadline on the private bank is now 8:00 p.m. EDT on Wednesday, March 22.

Read More: NYCB’s Strategy Shift Gets Big Boost from Signature Deal

Treasury’s Yellen Talks Deposit Insurance with Bankers at ABA Summit

Tuesday, March 21:

Treasury Secretary Janet Yellen tackled the controversial topic of coverage for uninsured deposits at failed banks, this time softening her previous comments that community banks would be unlikely to get such consideration. She also called for a review of the current regulations to make sure they address the risks facing banks today. Read the full story

• Senate Banking Committee sets hearings on SVB and Signature Bank failures.

Senate Banking Committee Chairman Sherrod Brown, D.-Ohio, announced that the committee would hold a series of hearings, beginning March 28. The first hearing will include these witnesses: Martin Gruenberg, chair of the Federal Deposit Insurance Corp.; Michael Barr, vice chair of supervision at the Federal Reserve; and Nellie Liang, under secretary for domestic finance at the U.S. Treasury Department.

Read More: What to Do About the Surprise Risks of Social Media and Self-Service Tools

Citigroup’s Jane Fraser Shares Some Behind-the-Scenes Crisis Insights

Wednesday, March 22:

Citigroup CEO Jane Fraser offers a glimpse of what it’s been like behind closed doors amid the first bank runs in an era of social media. The Citigroup CEO discussed her involvement with the lifeline for First Republic Bank and other key moments in the crisis in a frank interview with The Carlyle Group’s David Rubenstein. The Financial Brand presents excerpts from the interview. Read the full story

FDIC Finds Buyer for Silicon Valley Bank Deposits and Loans

• North Carolina’s First-Citizens Bank buys Silicon Valley Bank deposits and loans.

The Federal Deposit Insurance Corp. announced in the wee hours of March 27 that it had struck a deal for all deposits and loans of Silicon Valley Bridge Bank, N.A., the successor to failed Silicon Valley Bank. SVB’s United Kingdom operation had been sold to HSBC on March 13.

The buyer is First-Citizens Bank & Trust Company, Raleigh, N.C., which had $109.8 billion in assets at the end of 2022.

FDIC estimates that net of the deal the SVB failure will cost the Deposit Insurance Fund approximately $20 billion.

SVB’s 17 U.S. branches were expected to open as branches of First-Citizens on March 27. Eleven branches are in California and six are in Massachusetts. The bank already had numerous branches in California, many picked up in its merger with CIT Group (see more below). Prior to the FDIC deal First-Citizens did not have branches in Massachusetts nor any other part of the New England region.

The deal included First-Citizen’s acquisition of $72 billion of the bridge bank’s assets at a $16.5 billion discount. FDIC stated that $90 billion in SVB securities and other assets will stay in the receivership established when SVB failed, for later disposition. The agency’s news release did not give a figure for deposits acquired, only noting that the bridge bank had $119 billion in total deposits as of March 10. The acquiring bank’s news release, released later, stated that it was picking up $56 billion in deposits.

The deal is structured as a purchase and assumption transaction, but also features a loss-sharing agreement. FDIC and the bank “will share in the losses and potential recoveries on the loans covered by the loss-share agreement. The loss-share transaction is projected to maximize recoveries on the assets by keeping them in the private sector.” FDIC published questions and answers on loss-sharing deals.

The deal includes equity appreciation rights for FDIC with a potential value of up to $500 million. The recent FDIC deal for New York’s Signature Bank also included equity appreciation rights, in New York Community Bank, with a potential value of up to $300 million.

First-Citizens calls itself “America’s largest family-controlled bank.” It had over 500 branches in 22 states prior to the announced transaction. The vast majority are in North Carolina. At yearend 2022 it was the 30th-largest U.S. bank. First-Citizens finalized its acquisition of CIT Group in January 2022. During the 2022 earnings call held in late January 2023, First Citizens BancShares Chairman and CEO Frank Holding said the consolidation of First-Citizens Bank and CIT had been completed. First-Citizens was known for its retail banking prowess, while CIT was a strong nationwide commercial lender. The bank traces its history back to 1898.

“First-Citizens has a reputation for financial strength, exceptional customer service and prudent lending that spans 125 years,” Holding said in a company press release marking the acquisition. “We have partnered with the FDIC to successfully complete more FDIC-assisted transactions since 2009 than any other bank, and we appreciate the confidence the FDIC has placed in us once again. We look forward to building relationships with our new customers and positioning our company for continued success as we affirm our commitment to support the integrity of our nation’s banking system.”

First-Citizens has set up a webpage for customers and investors.

Federal Reserve and FDIC Testimony for Senate Banking Committee Hearing Revealed Early

Tuesday, March 28:

Silicon Valley Bank’s sudden demise rattled confidence in healthy banks and threatened the stability of the overall banking system. So the Federal Reserve needs to determine whether it can minimize this type of outcome in the future, and if so, how. That’s the message from Michael Barr, the Fed’s vice chairman of supervision, who lays out a series of questions for Congress to consider in exploring potential legislative action to change how banking is regulated. Barr’s testimony was released on March 27, a day before the March 28 Senate Banking Committee hearing it was written for. Meanwhile, the testimony of FDIC Chairman Martin Gruenberg was also released early. Gruenberg covers several reports, including one on the future of deposit insurance, that are promised for May 1 or sooner. Read the full story

Bank Failure Aftermath: As Solutions Are Sought, Bring on the Politics

Wednesday, March 29:

The hearings held in the House and Senate banking committees in late March are merely the overture for a period of rhetorical point-counterpoint that could go on for a long time. The Dodd-Frank Act of 2010 became law well after the financial crisis of 2008 that sparked it.

The brewing political battle was apparent from the opening moments of the Senate Banking Committee’s March 28 hearing, when the party leaders liberally dosed their opening statements with partisan language.

“The scene of the crime does not start with the regulators before us,” said the committee chairman, Sen. Sherrod Brown, D.-Ohio. “Instead, we must look inside the bank, at the bank CEOs, and at the Trump-era banking regulators, who made it their mission to give Wall Street everything it wanted.” (The panel of witnesses were all Biden appointees.)

Sen. Tim Scott, R.-S.C., the ranking committee Republican, questioned why neither Treasury Secretary Janet Yellen nor Fed Chairman Jerome Powell were at the witness table, instead of Nellie Liang, Treasury’s undersecretary for domestic finance, and Michael Barr, vice chairman of supervision for the Federal Reserve. He suggested the administration was “shielding” Yellen.

Then, pointedly looking in the direction of FDIC Chairman Martin Gruenberg, Scott cast aspersions on how much time the bidding process for Silicon Valley Bank took. “You hear rumors that this process was delayed because the White House doesn’t like mergers in any shape, form or fashion,” he said.

More of the same came during House Financial Services Committee hearings the next day.

Rhetoric breeds long-lasting legislative offspring. And President Biden’s pledge early in the crisis to drive major reform and to roll back Trump-era easing of some requirements has the makings of a campaign trail talking point.

First Republic Goes to JPMorgan Chase via FDIC Deal

Monday, May 1:

Weeks of deposit drainage and speculation about the future of the $229 billion-asset First Republic Bank ended early Monday morning, when regulators seized it.

JPMorgan Chase struck a weekend deal for the embattled San Francisco bank, which focuses on serving wealthy clients. Other bidders reportedly included PNC Financial Services Group and Citizens Financial Group.

In the purchase and assumption transaction, JPMorgan agreed to take over all of the deposits and most of the assets of First Republic. It will pay $10.6 billion to the Federal Deposit Insurance Corp. and benefit from a loss-sharing deal on First Republic’s residential mortgages and commercial loans, in which the FDIC will cover 80% of any losses incurred in the next five to seven years.

The megabank gains 84 branches in eight states, including 70 branches in the Los Angeles, San Francisco, New York and Boston areas that JPMorgan executives said fit well with its wealth management activities. They estimated that the deal will add about $500 million annually to JPMorgan’s earnings.

First Republic, the nation’s 14th largest bank, had been struggling since a massive deposit run at large regional banks across the country in March.

The sudden deposit flight led to the failure of Silicon Valley Bank in Santa Clara, Calif., and Signature Bank in New York, and left First Republic wobbling.

The drain was so severe that JPMorgan got just $92 billion of deposits in the acquisition. That includes a $30 billion infusion that a group of large banks had placed there in March, in an effort to help stabilize First Republic and bolster confidence in the banking system.

JPMorgan agreed to repay $25 billion to those other banks as part of its deal with the FDIC. (JPMorgan itself had put in the remaining $5 billion.)

First Republic was the second-largest bank failure in U.S. history, after Washington Mutual in September 2008. The FDIC estimated that it will cost the Deposit Insurance Fund about $13 billion. Acquired First Republic businesses will be overseen by JPMorgan Chase’s Marianne Lake and Jennifer Piepszak, co-CEOs for its consumer and community banking operation.

During an analyst briefing, JPMorgan Chairman and Chief Executive Jamie Dimon was asked if the resolution of First Republic was “a big signpost that the acute liquidity issues that the industry suffered in March” are mostly over.

“The banking system is very stable,” Dimon replied. “This part of the crisis is over.”

Dimon added that interest rates continue to rise and a real estate recession is looming.

“But for now,” he said, “we should just take a deep breath.”

This timeline and explainer was updated on May 2, 2023, to reflect recent developments.