Almost overnight, the migration from physical stores to computers and mobile devices increased exponentially in every industry as people decided they can do almost any activity safely from their home or their mobile device. In an effort to simplify daily lives that have become increasingly challenging, consumers wanted to complete virtually any task quickly and on the channel of their choice.

The shift to digital has not just been for Millennials either. The COVID-19 crisis has empowered consumers of all ages to become more digitally adept. For financial institutions not able to provide an end-to-end digital experience, portfolio growth has suffered. Alternatively, the largest financial organizations are gaining market share and getting the highest customer satisfaction ratings.

With the onset of the pandemic, consumers were no longer able to visit a branch to open a new account. While the the majority of financial institutions stated consumers could open new checking accounts digitally, the reality was that people who wanted to complete the process still needed to visit a branch. In other words, those financial institutions that were “faking digital” had the dilemma of not being able to open new accounts.

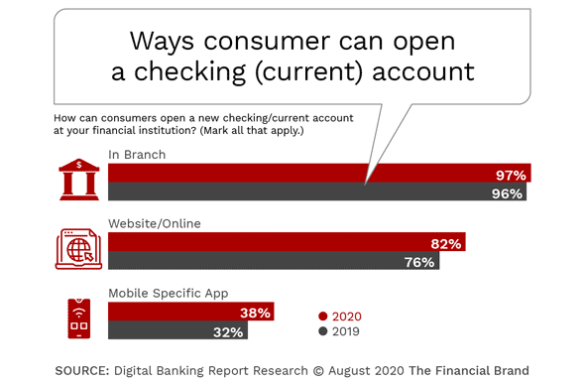

The good news is that while there are still many organizations that cannot support digital account opening, the incidence is far less than in the past. According to research by the Digital Banking Report, the percentage of institutions that offer online/website and mobile new checking account opening has reached 82% and 38%, respectively, compared to 76% and 34% in 2019 and 66% and 18% in 2017.

Interestingly, the percentage of banks with over $50 billion in assets offering online/website new account opening is actually lower than the industry average (75% vs. industry average of 82%) while the offering of mobile account opening significantly eclipses the industry average (50% vs. 38% industry average). This indicates an emphasis on the mobile channel as opposed to online capabilities.

Read More:

- Loyalty Advantage Now Favoring Digital Banks and Big Tech Firms

- Mobile Banking Drives Satisfaction and Growth

- Banks Losing Customers Who Want Seamless Digital Experiences

‘Faking Digital’ Decreasing

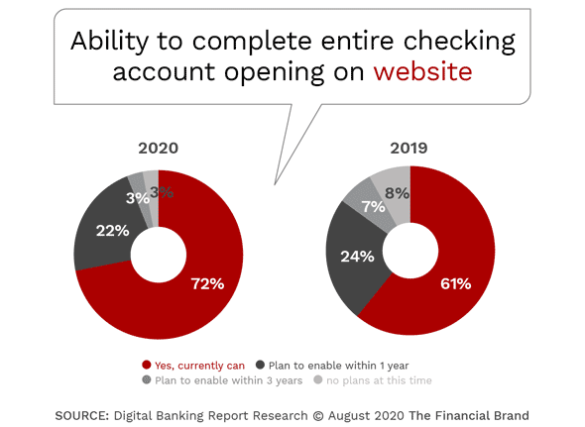

In the Digital Banking Report research, 72% of the institutions surveyed indicated that the entire online/website account opening can be done without coming into the branch. This compares with 61% in 2019 and only 48% in 2017. While historical evidence shows that many institutions do not follow through with their “plan to do next year,” we believe the impact of COVID-19 will result in another significant increase in end-to-end online/website account opening over the next 12 months.

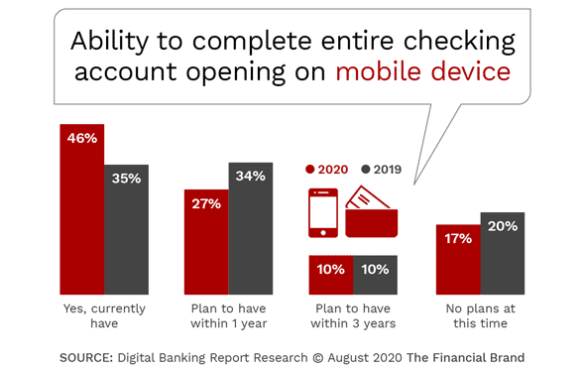

Not surprisingly, the number of financial institutions that provide end-to-end checking account opening with a mobile device in 2020 (40%) is far lower than those who could provide an online/website account opening opening. Despite this rather anemic number, there is a modest improvement over the percentage of organizations that could provide end-to-end mobile opening in 2019 (35%) and far better than in 2017 (24%).

It is still surprising, however, that over 25% of institutions indicated that they either had no plans to offer end-to-end mobile account opening or had plans three years out. Given the importance of mobile devices in a consumer’s life, this appears to be a missed opportunity.

As we have emphasized continuously, if you allow consumers to initiate the process online or on a mobile device, but still require a branch visit for signatures, documentation, ID verification or funding, the process does not have the customer experience as a priority. More importantly, as more digital banking alternatives become available, such as Chime, Varo, Current, Dave, Wealthfront, Betterment, Acorns, etc., will the consumer continue to open accounts where it is harder to initiate a relationship?

Read More:

- Becoming a ‘Digital Bank’ Requires More Than Technology

- How Bank of America and Chase Get Mobile Account Opening Right

The Need for Speed

With digital interactions, speed is everything. The longer a process takes, the more likely a consumer will abandon the process and try elsewhere. In the Digital Banking Report, State of the Digital Customer Journey, it was found that abandonment rates increased significantly as the time to complete an application increased. If the process took over ten minutes for an online/website process, or five minutes for a mobile process, the abandonment rate impacted the account openings by as much as 40%.

Now more than ever, the digital consumer expects simplicity, an intuitive design and speed of completion. Unfortunately, while the number of organizations offering digital account opening continues to increase, the ability to complete an account opening continues to be extremely slow. In fact, many consumers will notice that the digital process could actually be slower than an account opening in a branch.

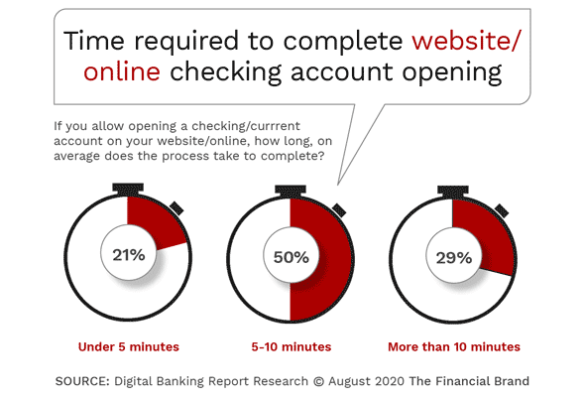

The research from the Digital Banking Report found that more than 75% of online/website account openings took longer than five minutes in 2020, with close to 30% taking longer than ten minutes. Surprisingly the change in time to open a new account online has changed very little since 2017.

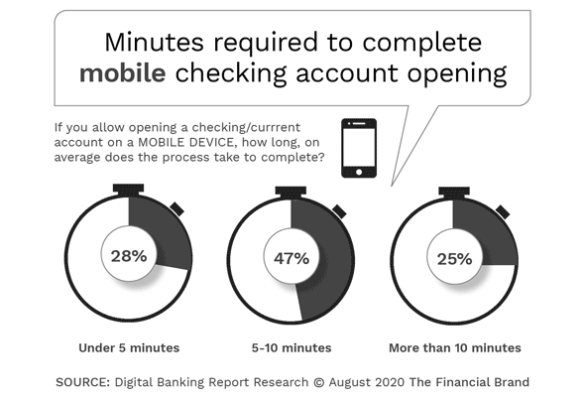

For mobile new account openings, the time to complete a new account opening was only slightly better, with only 28% indicating a process of less than five minutes, but 25% taking longer than ten minutes (compared to 20% in 2019).

It is clear that very few financial institutions have changed back-office processes to reflect digital engagement needs. To meet consumer expectations in a digital world, organizations need to build digital capabilities from the foundation as opposed to simply digitizing current outdated processes.

Providing Digital Account Opening is Only a Start

Becoming a “digital bank” is much more involved than simply enabling a consumer to do a process online or on a mobile device. It is unacceptable for a consumer to take longer to open a checking account digitally than it does to apply for a mortgage, buy a car, create an investment account relationship or get a loan.

For consumers that may no longer want to visit a branch because of safety or time constraints, they will actively seek out the easiest option. Financial institutions should also avoid comparing themselves to other traditional banks and credit unions, instead comparing themselves to digital-only banks that didn’t start with legacy processes.

The good news is that financial institutions do not need to start from scratch. There are many firms that can help to improve the digital account opening process. These firms can help remove friction, increase engagement and improve customer satisfaction using time-tested tools and strategies.

In a world impacted by the pandemic, with consumer behaviors and expectations changed forever, organizations must improve their digital account opening process beyond the basics or be challenged by fintech firms and big tech providers who understand the basics of digital engagement.