Digital banking alternatives from the largest traditional banks, smaller fintech firms and big tech companies are increasingly making loyalty at most banks and credit unions tenuous. While an entire relationship may not be lost initially, the risk of loss of individual accounts within an existing relationship is increasing, as better digital options become available. This disintermediation of accounts and/or balances makes the overall relationship less profitable.

Unless legacy banks and credit unions respond with greatly improved digital experiences, the ‘hidden defection‘ will only get worse, according to a Bain & Company study. “Developing a seamless digital experience that resolves a customer’s need the first time around, without forcing them to resort to a phone call or branch visit, is key for any financial institution looking to stop leakage and retain customers,” said Gerard du Toit, a partner with Bain & Company and co-author of the report.

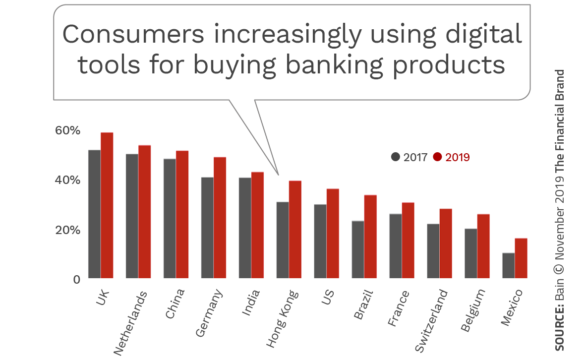

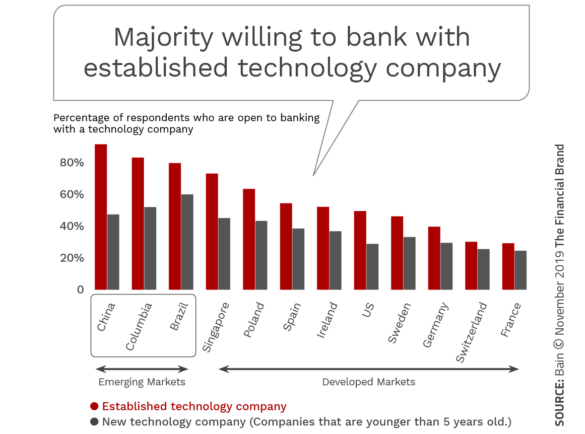

The research found that younger consumers greatly prefer to research and open new relationships using digital channels. This is especially true for less complex services, such as checking accounts, saving accounts and credit cards. These same consumers are also more likely to be willing to test tech companies and fintech alternatives. In fact, 75% of consumers between 18 and 24 said they would use a banking product offered by an ‘established’ tech company.

Read More:

- Loyalty Advantage Now Favoring Digital Banks and Big Tech Firms

- Mobile Banking Drives Satisfaction and Growth

‘Hidden Defection’: The Invisible Threat

Digital alternatives to almost any traditional financial product and service are now being offered by non-traditional financial services providers. From person-to-person payments, to automated savings tools, to consumer loan and mortgage lending options, new digital services are available that can improve the experience for anyone with a computer or a mobile device.

As consumers try different digital alternatives, they may not close their checking account with their primary bank, either because of inertia or because of the perceived difficulty of switching providers. But, as many of these digital offerings from non-traditional firms gain customers and become more prevalent in the marketplace – because of customer satisfaction – the defections will only increase.

Traditional banks and credit unions should not be lulled to complacency because of the small size of many of these alternative providers, because the flow of new business to many of these firms is only increasing. For instance, “while only 2% of U.S. respondents use Rocket Mortgage, the company enjoys a 17% share of the total mortgage outflow from customers’ primary bank.” This increase in new account openings is also true for most of the major challenger banks in the U.K. as well.

Halting Attrition Not Easy – But Rewards are Significant

Stopping the ‘hidden defection’ requires much more than a flashy mobile banking app. Digital processes must be changed from within to provide a seamless experience across the consumer lifecycle. Consumers can’t be expected to use multiple channels to conduct product/service research, open a basic account or complete a rudimentary transaction. Consumers know their bank and credit union can do better.

If a consumer is forced to complete a digital channel engagement in a branch or via a phone call, satisfaction goes down (at best) or the consumer disengages altogether (at worst). Also, if multiple channels are required, the cost to the bank or credit union increases exponentially. “The outflow [of customers] will only get worse for banks unless they significantly improve and digitalize the customer experience and supporting back office operational processes to drive down cost,” said du Toit.

If a seamless digital experience is provided, customers become promoters of the organization. They also spend more on their primary credit card, are more likely to buy their next product from the institution and are less likely to defect to alternative solution providers. Promoters also recommend their bank to others nearly two to six times as much as detractors.

Positive Digital Experience Opens Door for Open Banking

For those organizations that meet the needs of the digital consumer, the benefits could extend beyond the current portfolio of services, according to the Bain study. The organizations with the best extension of digital processes and experiences will be in the best position to develop a broader ecosystem of services beyond the products currently offered.

These new segment offerings within the open banking ecosystem, or even non-traditional services, could lead to new revenue streams. And, because consumers usually prefer one-stop shopping, they will most likely shop their current providers first.

Read More:

- Becoming a ‘Digital Bank’ Requires More Than Technology

- How Bank of America and Chase Get Mobile Account Opening Right

Human Intervention Still Desired … Sometimes

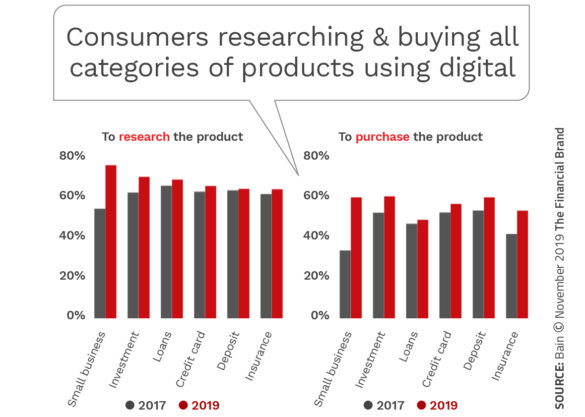

Over time, consumers may trust digital engagement for all service interactions, but currently, consumers still prefer human intervention and advice when they want to purchase more complex services, such as mortgages, investment products, insurance, etc. Often, this preference is a result of perceived ease of engagement, ‘broken’ processes, lack of knowledge that a digital option is available or perceived safety.

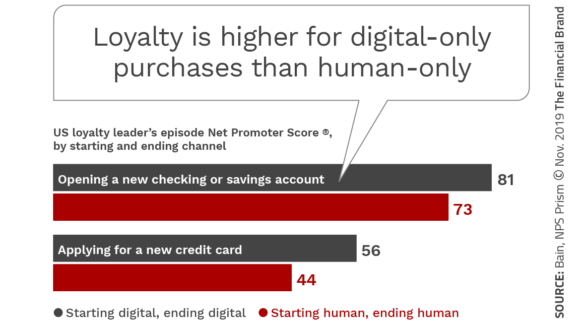

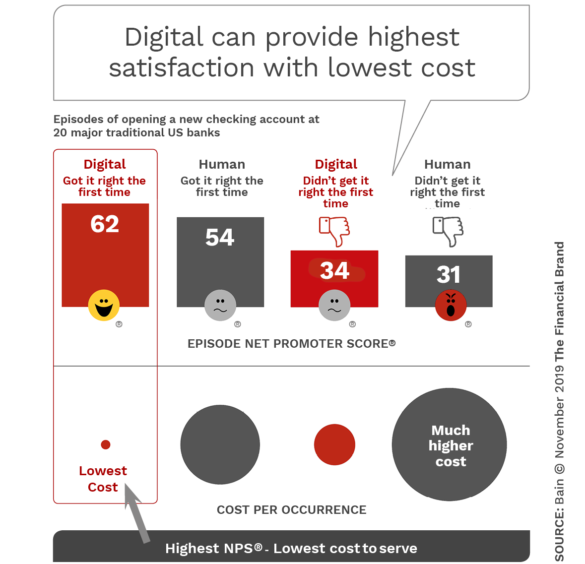

As mentioned, when it comes to more basic service openings (such as checking or credit cards), most consumers prefer digital-first or digital-only engagements. In fact, the satisfaction is higher for digital-only (starting and ending digitally) account openings than for human-only openings.

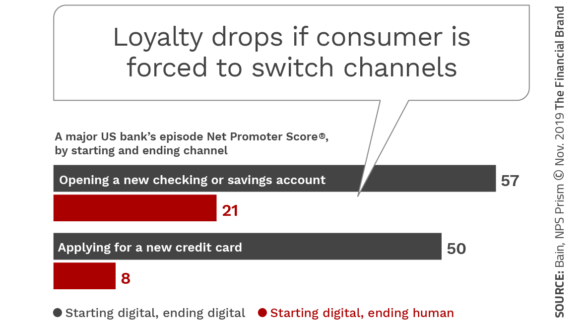

As could be expected, if a consumer is forced to change channels for a ‘simple’ engagement, the satisfaction drops by close to two-thirds (checking or savings account opening) or by a factor of six (credit card opening).

Tech Firms Present Ongoing Threat

As consumers search out banking product solution providers that can save them time and money, the willingness to purchase financial services from large technology companies continues to increase, especially among younger consumers.

Of bigger concern for legacy banks and credit unions is that many of these big tech disruptors receive higher satisfaction ratings than traditional banks. This is particularly true in emerging markets. As fintech firms, big tech alternatives, and other non-traditional providers gain more acceptance, it will be harder for legacy retail banking firms to catch up … either from an internal process basis or from a brand preference perspective.

As a new open banking ecosystem emerges, with new products, services, providers and collaborations, there will be an opportunity for both traditional and non-traditional organizations to leverage data, technology, analytics and digital process transformation to retain and grow customer relationships. This will require a contextual customer journey perspective.

Those firms that are successful will benefit from both a loyalty and revenue advantage.