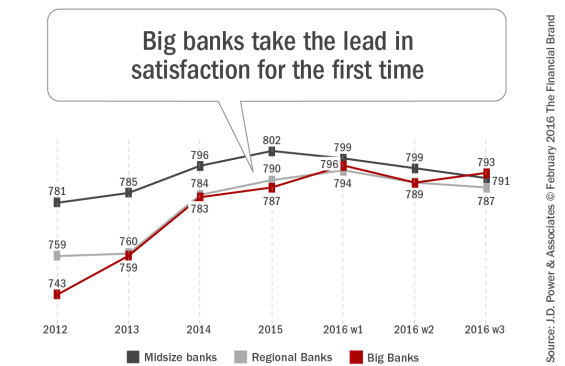

The biggest banks have significantly improved in overall customer satisfaction, while midsize banks have declined and regional banks have plateaued, according to the J.D. Power 2016 U.S. Retail Banking Satisfaction Study. Driven by a focus on digital offerings, improved personal interactions and winning with the key growth segments of Millennials, the emerging affluent and minorities, satisfaction with big banks rose for the sixth consecutive year, while satisfaction with midsize banks dropped for the first time since 2010. More concerning could be that midsize banks’ intended attrition has doubled over the past 5 years, and is currently the highest among the bank segments according to the study.

Continued heavy investment in digital channels by the biggest banks is definitely being rewarded, with the largest banks showing significant improvements in all digital categories. The big banks scored highest in online satisfaction (839), mobile (858) and ATM (841) interactions in the most recent study. The inability for the majority of regional and mid-sized banks to keep pace with investment in digital technology is apparent, with online, mobile and ATM satisfaction levels all being below 2015 levels.

The outlook for the biggest banks remains positive, driven by their ability to invest in digital channels, advanced analytics, and branch transformation, as well as their success in growing customer segments. “Based on their current trajectory, the country’s largest retail banking institutions are expected to achieve a substantial lead in overall customer satisfaction vs. midsize and regional banks by 2020,” said Jim Miller, senior director of banking at J.D. Power. “This trend puts midsize banks most at risk. Regulatory costs have made it difficult for them to invest in strategies to compete with larger rivals, and unless they take proactive steps to change course, we expect this to result in consolidation in the midsize bank marketplace.”

Mobile Banking Impacts Satisfaction

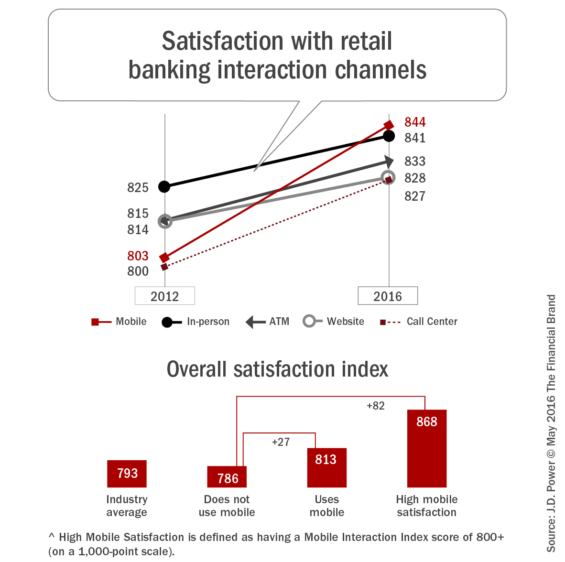

Over the past several years, the usage rate of mobile banking apps has increased exponentially. Correlated with increased usage, satisfaction levels with the mobile channel have also improved, exceeding all other channels and becoming the most satisfying interaction channel.

Mobile banking has an impact on overall customer satisfaction as well, according to JD Power. As shown, there is an immediate lift in overall satisfaction when consumers use mobile banking (+27 points on a 1,000-point scale), with an even greater impact when banks provide their mobile banking customers with a highly satisfying experience (+82). In fact, the impact of mobile extends to all aspects of the customer experience, including the ability to:

- Mitigate the negative impact of a problem or complaint

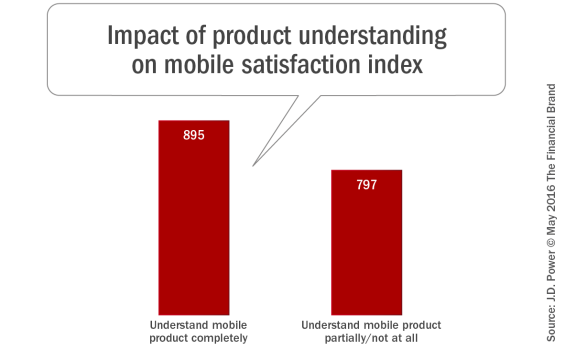

- Help maintain satisfaction with a smaller branch network

- Improve perceptions of available products and services

- Reduce price sensitivity

Mobile Banking Impacts Segment Growth

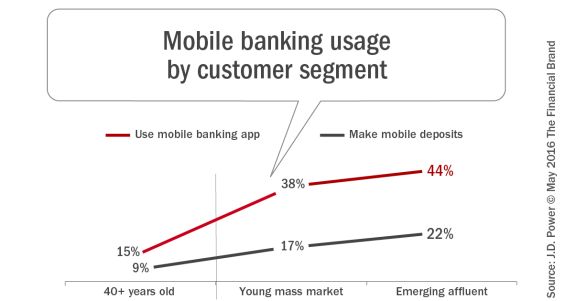

Nearly half of U.S. consumers are under the age of 35, considered part of the Millennial segment, with their proportion of the population continuing to increase. These consumers are experiencing increasing wealth as well as the need for additional financial services. In addition to the Millennial and emerging affluent segments, the proportion of ethnic minorities is also projected to increase significantly over the next 20 years.

These are important demographic shifts since, while mobile banking usage has increased across all customer segments, mobile banking has become an imperative to customers in the emerging affluent segments, who are the heaviest users of mobile banking and most likely to make mobile deposits. While customer attrition has been found to run high among emerging affluent customers, a strong mobile offering can mitigate attrition while also improving customer loyalty and advocacy.

Big banks have experienced growth all virtually all demographic segments over the past several years, but have been the most successful at acquiring and satisfying consumers in emerging growth and minority segments, positioning these banks to reap greater benefits in the future.

Marketing of Mobile Banking

Offering mobile banking functionality is not enough in today’s digital marketplace. A financial institution needs to continually improve the offering and encourage ongoing mobile banking engagement.

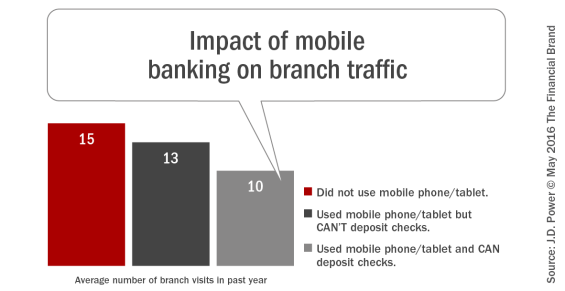

Not only will the marketing of mobile, both inside and outside the branch, drive satisfaction and help acquire the most desirable customers, it can help organizations reduce branch traffic through increased use of this alternative channel. Such reduced traffic will, in turn, help banks reduce branch-related headcount and allow branch employees to build a stronger ‘universal teller’ strategy that revolves around advisory services.

The key components of mobile banking support include a clear communications process during account initiation and during a sequence of onboarding communications after the account is opened. Unfortunately, many organizations are falling short of expectations to educate the customer on mobile banking functionality at account initiation and few organizations meet the minimum standards of communication thereafter (proactively contact customers at least twice per year about product/service features).

Despite the fact that customer satisfaction ratings are increasing for all sized banks, the improvement is not uniform across all banking segments. Those organizations who make their mobile banking offerings ‘best in class’ and who actively promote these offerings will benefit from the potential of increased satisfaction, improved market share and decreased delivery costs.

About the Report

The 2016 U.S. Retail Banking Satisfaction Study is the longest-running and most in-depth survey of the U.S. retail banking industry, with more than 75,000 customers evaluating various aspects of their banking experience. The study measures satisfaction in six factors (listed in alphabetical order): account information; channel activities; facility; fees; problem resolution; and product offerings. Channel activities include six subfactors (listed in alphabetical order): ATM; branch; call center; IVR; mobile; and website. Satisfaction is measured on a 1,000-point scale.

For the report purposes. ‘big banks’ are defined as banks with $180 billion or more in total deposits, ‘regional banks’ are defined as those with $33 billion-$180 billion in total deposits, and midsize banks are defined as those with $2 billion-$33 billion in total deposits. Emerging affluent are defined as being younger than 40 years old with income of $80,000 or more; young mass market are defined as being younger than 40 years old with income less than $80,000. Minorities included African-American, Hispanic, and Asian customers, with non-minority including Caucasian customers.