As one of the financial industry’s biggest and most outspoken influencers, Brett King is well known for provocative predictions and prognostications.

In the final installment of his multi-book series on the future of banking, Bank 4.0: Banking Everywhere, Never at a Bank, King warns that the American banking system is facing a fork in the road that will ultimately determine its destiny.

His latest book foretells a not-too-distant future where many financial institutions will either evolve or consolidate — or become downright obsolete — and a world where banking will increasingly become an embedded function. Ultimately it’s a race between bank and non-bank providers vying to eliminate friction in people’s use of financial services.

King first burst onto the U.S. banking scene in 2010 with Bank 2.0: How Customer Behavior and Technology Will Change the Future of Financial Services. The book was a wake-up call to many financial executives. Back then King was among the first few who were questioning the future role and relevance of many sacred concepts central to traditional banking and branch-based delivery models. He foresaw the smartphone’s potential power to redraw what financial services would look like.

His next book, Bank 3.0: Why Banking Is No Longer Somewhere You Go But Something You Do (2012), warned that American financial services were falling behind the curve of the world.

Frustrated by the pace of change in banking, King finally became a fintech entrepreneur himself, launching the white-label banking platform Moven.

Even when industries have had lots of discussion about changes going on around them, companies push back, refusing to believe what’s going on, or at least not being willing to acknowledge it.

“I’m always trying to raise the industry’s awareness,” King explains, “because typically by the time competitors have eaten your lunch, it’s too late to do anything about it.”

“We’re seeing a material shift in the economics of banking,” King continues. “There are a ton of banks in the U.S., and there are probably 2,000 that are at risk.”

He characterizes the BB&T and SunTrust deal as a precursor of more to come. “They saw that the economics were failing them at the scale where they were,” he says. “They had to roll up to get to a scale that made sense.”

How far off that day of reckoning is, and its extent, can be debated, says King. But he’s certain a reckoning is on its way. The end game for this phase of financial transformation will come, he believes, within 20 years. How well the traditional industry in the U.S. transitions hangs on a mix of willingness to change, regulatory attitudes and synching with consumer preferences.

Take Those ‘Banking Goggles’ Off

King portrays a world where banking institutions sometimes view reality through their own “banker filter,” reacting to many events as if they are competitive inroads when they are actually much different strategies. One example is Uber’s introduction in early 2018 of a Visa debit card for its drivers in cooperation with Green Dot Bank’s GoBank brand.

“Uber doesn’t want to be in banking,” says King. “They just wanted to onboard drivers more quickly, and pay them multiple times a day. But Uber couldn’t recruit drivers because many candidates didn’t have bank accounts. They had to fix some banking problems in order to grow their business.

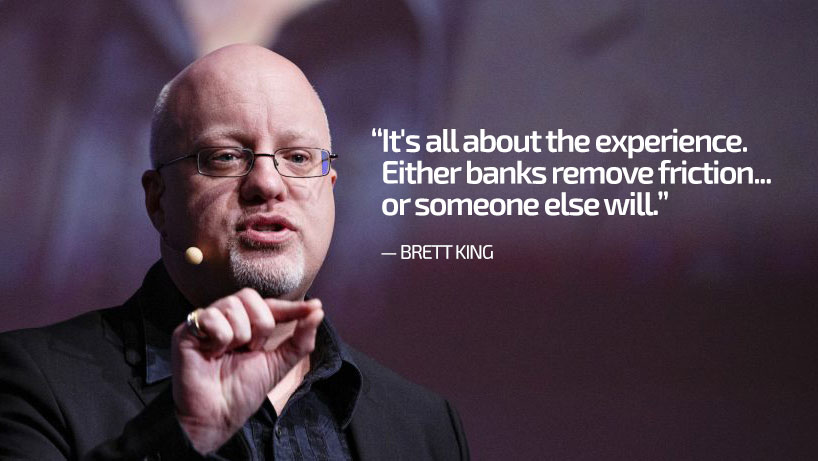

“Platforms like Uber, Amazon, and others will be proactively looking for solutions that will end up reforming banking, whether the banks see the need for that reform or not,” warns King. “Thinking that an Uber is competing with the bank is missing the point. It’s all about the experience. Any friction that isn’t absolutely necessary will be eliminated from the technology layer. Either banks remove friction… or someone else will.”

As King explains it, bankers need to make an essential mental shift. “They’ve always thought banking was different,” not subject to the same forces that other industries face. In his research, King has never seen a single industry that was immune to technology disruption.

“There are banks that are still fundamentally Bank 1.0 operationally and in customer engagement,” King maintains. The majority of banks still don’t offer account opening on a mobile, and thus would barely qualify for Bank 3.0 status — “sort of Bank 2.5,” he says.

King believes that true digital banks, working towards Bank 4.0 status, “number in the dozens globally, maybe. Most will never get there, including some of the challenger banks,” he predicts.

Read More:

- The Rise of Digital-First Banking and The Financial Institution of Tomorrow

- How Banks Can Begin to Catch Up with Amazon’s Personalization Genius

Ditch Friction, Embed Function, for Contextual Banking

“Friction will be the biggest killer of bank revenue in the next 10 years,” King writes in Bank 4.0. The lowest-friction experience, he says, will be most widely adopted, and if that is via a fintech’s app, consumers won’t look in the rear view mirror at the bank process they used to rely on. King gets exercised by any process that requires unnecessary steps, unnecessary travel or outdated methods such as “wet” signatures in an age when CFOs can run aspects of their company off a smartphone. The idea of using a branch as a place to submit a paper application annoys King, especially when the only reason may be outdated policies or regulations.

But that’s just the beginning. Making processes frictionless leads into making them “contextual.” The banking part of purchases and other events ceases to have a separate existence, and, ideally, get reimagined.

In the book King explains that reimagining banking is very different from merely digitizing the old way of doing things. A Bank 4.0 institution, he explains, engages in what he calls “first principles design thinking.” Essentially this means backing up from the task, tearing up the old blueprint, and confronting the job afresh with modern capabilities in mind. Here’s a specific example.

“First principles means backing up from the task, tearing up the old blueprint, and confronting the job afresh.”

“First principles mean new financial service networks wouldn’t build credit scores that punish you for missing a payment on your card,” King writes. Instead, “organizations would design systems that predict your behavior, only encourage credit use when you really need it, and help you manage that credit line reactively, including influencing new spending decisions so you don’t compromise your ability to pay back your credit line.” There would be no need for a plastic card or application process at all.

As King describes it, contextual banking combined with first principles thinking will put financial services in the moment, more and more. He predicts that “product” thinking will be eclipsed.

| Financial Product or Service | Replacement Embedded Experience |

|---|---|

| Credit Card | Predictive and contextual credit access |

| Overdraft | Emergency credit access |

| Checking, Current Account or Debit Card | Cloud-based personal value store linked to a mobile wallet |

| Savings Account | Behavioral savings tools and prompts |

| Personal Loan | Payment options advice in-store or contextually |

| Mortgage | Home purchase assistant |

| Car Loan (or Lease) | Subscription to autonomous vehicle access |

| Small Business Bank Account | Intelligent business value store with accounting, tax and payments AI |

| Business Line of Credit | Predictive cash flow analytics and smoothing |

| Life Insurance | Longevity and after-life management |

| Health Insurance | Health optimization and monitoring services |

| CDs, Term Deposits and High-Yield Savings | Wealth-builder robo-assistant |

| Mutual Funds | Robo-advisor with net worth manager |

| Foreign Exchange Service | Global wallet add-in |

“The utility of banking is what made it so essential to our lives in the past,” says King. “The utility is still there, but you can’t think about it in isolation anymore, particularly as you start thinking contextually. If you are not thinking about how banking fits into someone’s life, then you’re not thinking about banking in the value chain of experience.” For example, How do you give access to credit to someone who is paying for groceries without a plastic credit card? This is the type of problem that the fintech guys are continuing to look to solve, King states.

Bankers need to tap into the perspective of younger consumers to envision what will be relevant in coming years. “By 2030,” King writes, “the bank account itself is likely to be just a value store on the phone for the vast majority of consumers who have come into the banking system in the 21st century. The fact that … the money might be stored in a bank account somewhere, is almost incidental.”

Survivors from the existing banking industry, King insists, will be those who can dissociate themselves from legacy systems, but also legacy thinking. They will be ready to “strip and rebuild,” as he phrases it, and they will stop hiring bankers, hiring specialists like data scientists, machine learning specialists, and behavioral psychologists instead.

Why Many U.S. Players Remain Mired in the Status Quo

In many parts of the world, financial services players have double-jumped, like checkers, over most American banking institutions. In Kenya, for over a decade the phone-based banking system offered by M-Pesa brought financial inclusion and widespread mobile banking to many people who had never seen a bank branch. In China, home to tech giants like Alibaba, “they didn’t have legacy behavior to displace, whereas in the U.S. if you want to get people to use mobile wallets or to make mobile payments you have to stop them from using cash, cards, and checks,” says King, “whereas in China you only had to stop them from using cash.”

U.S. regulators are realizing there is a sea change, says King, who began working with Washington officials in 2012. They’re not quite sure what the answer is, how things should change, but at least now the posture is one of information gathering and figuring out what happens next,” says King. “The biggest problem in terms of moving regulation forward is getting over ingrained behavior among examiners and supervisors. On the other hand there is simply the problem that big regulatory changes require legal changes. That’s tougher to tackle and means change will be slower.” By contrast, in other countries change often outstripped regulators. In Kenya, for example, King says M-Pesa had developed so quickly that things were in place before the regulators understood what had happened.

While King worked with the Obama Administration extensively, he says the Trump Administration barely has anyone looking at fintech. “There tends to be a posture currently that is a lot more supportive of incumbents than disruptors.” The Administration issued an executive order on artificial intelligence that is considered somewhat vague and includes no funding plan.

“The really big question in the U.S. is if we truly get a fintech charter,” says King. The charter at the Comptroller’s Office is being resisted by state regulators and others. King’s Moven has wanted to acquire a bank charter for years, but so far this has been elusive. He sees this as of a piece with other resistance that holds the pace of digital change back in the U.S. compared to other countries.

“Is innovation just this little function you have over on the side? Or are you trying to actually change your organization’s culture?”

Much is happening in the private sector, but not all of it is moving the ball forward. Asked about financial institutions’ innovation labs, King draws a bold line between those that are ivory towers and those that work with and fund startups.

“The real challenge is, is innovation just this little function you have over on the side? Or are you trying to actually change your organization’s culture?” asks King. “Organizations like DBS in Singapore, Capital One and BBVA here have been committed to changing the culture from one that’s risk averse and traditional to one that has innovation at its heart. They understand that the future of the business lies in technology. There’s only a handful of banks that fit that description.”

Olive Branch: Brick-and-Mortar May Still Have a Future

King, who is widely portrayed as categorically anti-branch, sees some situations where some branches can still serve a purpose, but not for traditional functions — not in an “embedded banking” world.

“If there’s a place in the future for a branch to add some extraordinary value in engagement that’s viable, I’m all for that,” says King. “But using branches to open accounts and do traditional day-to-day banking is not it. If you can’t deliver that in real time, you won’t survive.”

Meanwhile, branching supporters point to developments like Chase’s building numerous new branches to prove that King is wrong about branches. King says branches will remain for many years, but that the population has been declining for a decade as digital has grown. And he points out that on a net basis Chase’s branch numbers are still declining.

The biggest problems for branch economics is customers just aren’t visiting them regularly. “For most major U.S. retail banks half of their customers don’t visit a branch annually, and most of those that do, do so less than once a year. That behavior no longer supports the economics of large branch networks. It’s forcing consolidation,” says King.

“There’s nothing I’ve seen anywhere globally to suggest this trajectory will change,” he adds.