Credit cards are undergoing a transformation. The cards — whether actual plastic or an account residing in a digital wallet — increasingly offer a range of payment and credit possibilities, according to research by Keynova Group.

In tandem with this, the nature of cardholders’ digital user experience, from shopping around for new cards to managing the security and privacy of their card account, is changing.

Self-service channels have improved, thanks to the increasing utility of mobile devices and the growing sophistication of banking websites. Users are in direct control more than ever before and have options like video chat for when they get stuck.

Credit card issuers that don’t keep up with leaders on these trends could see interest in their offerings flag.

Trend #1: Major Card Issuers Cater to Comparison Shoppers

Competitive pressure often leads to innovations, which then trickle down to other issuers. One of these is the ability to comparison shop for credit cards.

It’s grown increasingly common for people looking for new credit cards online to visit an issuer’s website where there is not only substantial detail about individual card offers, but also an option to set up side-by-side comparisons of those offers.

Among the issuers that Keynova studies, this feature has become table stakes. And three issuers — Discover, PNC Financial Services and Wells Fargo — even enable comparisons with offerings from their competitors.

As variations on cash back and other rewards proliferate, more issuers are providing calculators and other aids to enable card shoppers to determine which option would earn them the most, given their typical spending patterns. Some issuers provide extra cash incentives or bonus cash-back multipliers for cardholders if they spend a required amount during an inaugural period, and those rewards also can be added into the calculators in a few cases.

While most cash-back deals offer multipliers in the single digits, a handful can go into double digits under the right circumstances, according to Beth Robertson, managing director at Keynova Group, who helped compile its fourth-quarter 2022 Credit Card Scorecard.

The study assessed the 10 leading U.S. card issuers, and in terms of overall value, JPMorgan Chase topped the field with its Marriott Bonvoy Boundless credit card. By combining several features under the card’s reward matrix, people charging room nights and related costs in participating Marriott properties can earn as much as 17 times every dollar spent in the hotels.

In an interview with The Financial Brand, Robertson reviewed the trends Keynova found.

Trend #2: New Ways to Use Up Credit Limit Beyond Point of Sale

Traditionally, a credit card from a bank enabled customers only to charge purchases and to obtain cash advances. Robertson says that as issuers seek to grow their card portfolios, they are coming up with new ways to use each cardholder’s credit limit. The idea is to provide credit in forms beyond card spending while within the parameters of the initial credit evaluation.

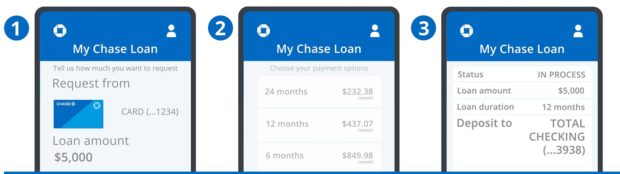

For example, My Chase Loan permits JPMorgan Chase customers to use their card’s associated mobile app to request that a portion of their credit line be issued as a personal loan. No new credit evaluation is involved.

The bank makes a rate offer through the app — it will be lower than the standard purchase interest rate — and the customer selects the term. Once the offer is finalized, the app tells the customer that the proceeds of the personal loan will be deposited into their checking account.

“It’s a smart way for the consumer to take advantage of their credit if they want to do a longer-term payoff,” says Robertson. “Maybe you want to put some money down on a kitchen renovation.”

Robertson notes that American Express and Citibank are among the credit card issuers that offer similar personal loan spinoffs to their cardholders.

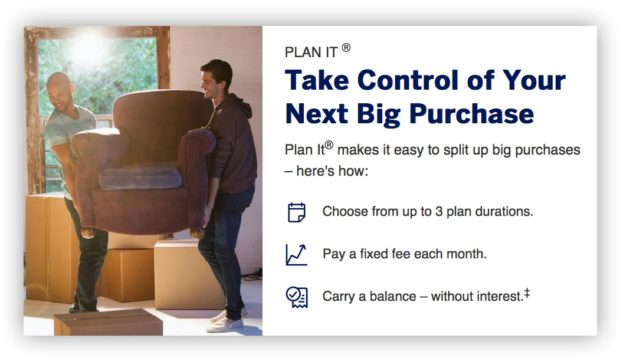

Another credit option that is becoming more common is a variation on the buy now, pay later theme. The customer can designate through the card app that a purchase be classified to be paid in set installments, similar to a purchase made with BNPL financing.

“This is done through the card account within the pre-approved credit limit, so it’s a little more controlled and not offered to the consumer endlessly,” says Robertson.

It provides the benefits of BNPL, albeit with a fee, without helping the borrower to get into debt beyond their credit card spending ceiling.

Robertson says American Express is especially adept in promoting this capability — which it refers to as the “Plan It” installment option — for its eligible card products.

Read More:

- 5 Payment Trends to Watch in 2023

- ‘Pay By Bank’ Trend Is Next Front In Merchants vs. Banks Payments War

- The Lines Between Credit Cards and BNPL Are Blurring

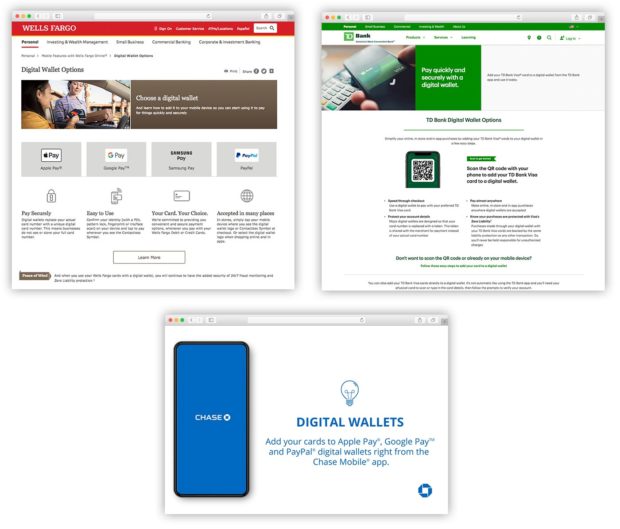

Trend #3: Instructions on Adding the Credit Card to Digital Wallets

At one time banks and other card brands seemed to want to forestall consumers loading their cards onto digital wallets. Robertson says that more issuers now make it easier to find instructions for loading cards into wallets and the advice is more explicit. There’s recognition that more consumers want contactless choices — and that means being in their digital wallet is essential to gaining traffic.

“It’s much more accessible than it was several years ago,” Robertson says, “when you had to hunt for anything about digital wallets on websites.”

Now four of the 10 brands studied — Bank of America, Capital One, Discover and Wells Fargo — provide direct access digital wallet management tools from their account summary pages.

The sites offer detailed written instructions. In addition, the use of instructional videos demonstrating what to do is growing, Robertson says.

“Many people are visual learners, so instead of just reading the steps to load the card, they can observe someone doing it and understand it more readily,” she says.

Read More: Digital Wallets Could Cost Banks Billions in Lost Payments Income

Trend #4: Self-Service Option for Disputing Card Charges

Videos showing cardholders how to dispute transactions online, sometimes on the same page as transaction records, also are becoming more common.

In such efforts Robertson cautions against overdoing the marketing glitz.

“Some of the videos I’ve seen look a little too much like advertisements, and they are less instructive,” she says. “I’m usually disappointed when I go through one where I think I’m going to get some knowledge and instead feel I’ve watched a feel-good ad.”

Useful videos can reduce expenses for a card issuer, she notes. “As long as consumers feel comfortable about doing something, then they’re more willing to continue self-servicing in the digital channel rather than calling customer service or going into a branch.”

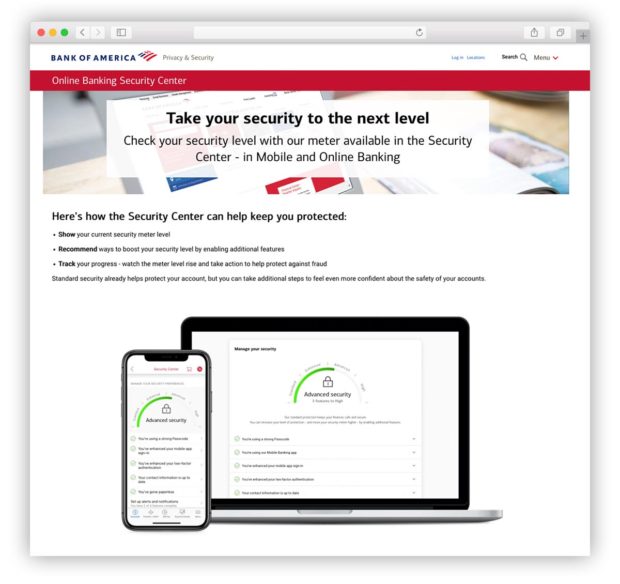

Trend #5: Help With Securing Card Accounts and Digital Identities

Card issuers are offering customers multiple types of assistance with safeguarding their finances, according to Keynova’s research. This takes different forms from one institution to the next.

At Bank of America, for example, customers can use a “security meter” on either the website or mobile app to see how well-secured their card accounts are. Besides showing the state of protection the meter also provides suggestions on how to bolster security.

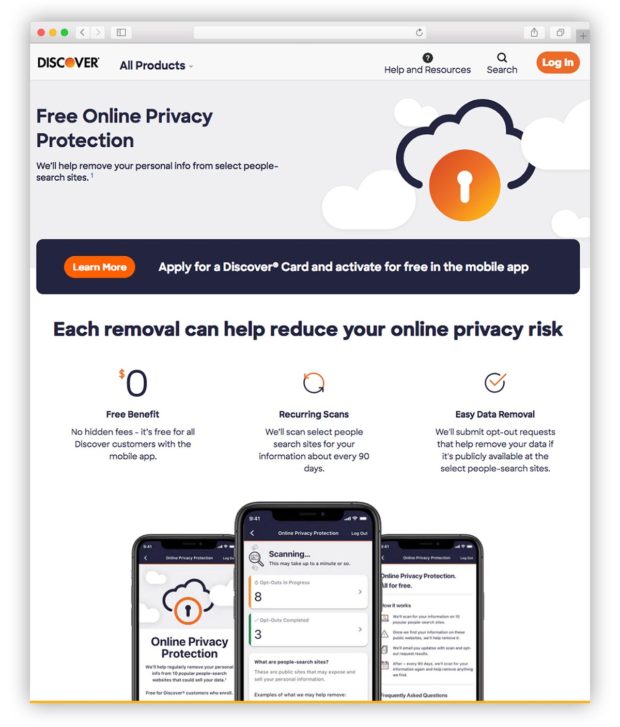

Discover provides its cardholders with online privacy protection services through its mobile app. This detects the appearance of a customer’s personal data on the dark web and other places they wouldn’t want it to be — such as nosy people search sites like Spokeo.com — and then works to remove it.

The free service is only available on the app, which provides an incentive for cardholders to download it. “We want to have our storefront on your phone,” Shannon Kors, vice president of marketing and product strategy at Discover, told American Banker.

Discover partnered with BrandYourself, an online reputation management company, to provide the service.

Robertson says that card issuers have also begun to offer features based on the recognition that consumers today have their account numbers liberally sprinkled all over the place. Food delivery services have them on file, as do subscription services for everything from shaving cream to goodie boxes, not to mention ecommerce merchants large and small.

New services from credit card issuers acknowledge both the convenience — and the risk — of such arrangements.

Some issuers provide access to lists of recurring merchants paid with their cards and provide contact information. That way, Robertson says, “If you have to have your card reissued because you lose it or your number becomes compromised, you can reach out to the merchants to readily update your information.”

One service offered by Chase goes beyond this to track any merchant that is storing the customer’s card number.

“This is interesting in terms of protecting yourself against fraud in situations where you may have your card numbers and card information stored with a merchant that you no longer use or may not feel as secure about anymore,” says Robertson. “Prior to having a service like that, you may have had no idea that certain websites and merchants were storing your card data.”

Robertson used this service from her card issuer recently. She bought a home and provided access to certain accounts as part of the transaction. So she decided to check afterward who still had access to her account information. When she saw that the mortgage lender was listed, she used a feature enabling her to revoke it.