Inflation is causing consumer debt to accelerate, especially on credit cards issued by banks. This dynamic is also driving up use of unsecured personal loans, which many consumers use to consolidate their card debt and bring down their overall interest burden.

However, for many consumers, the relief from these personal loans only lasts so long. Many don’t change their spending habits and run up their debt all over again, according to TransUnion research.

An especially significant finding in the research is that, as consumers from Generation Z age, their use of credit cards goes up. This is notable because research on this generation has long suggested that they resisted the use of credit cards, just as Millennials once did when they were younger.

The growth and popularity of the buy now, pay later concept has been credited in substantial part to Gen Z’s adoption of BNPL instead of credit cards. Various studies of Gen Z, which TransUnion defines as consumers born between 1995 and 2005, have also indicated a preference for using debit cards for spending instead of credit cards.

Read on for details on five key findings about these loan categories from TransUnion, including which type of personal loan borrower tends to perform better in terms of credit quality.

Bank Credit Card Debt Hits a Record (Again)

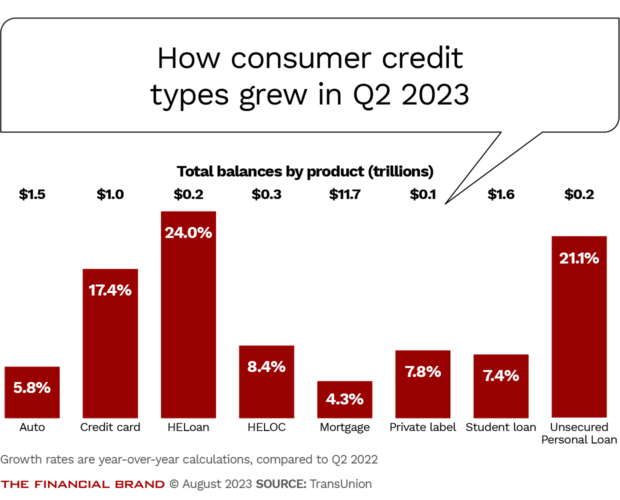

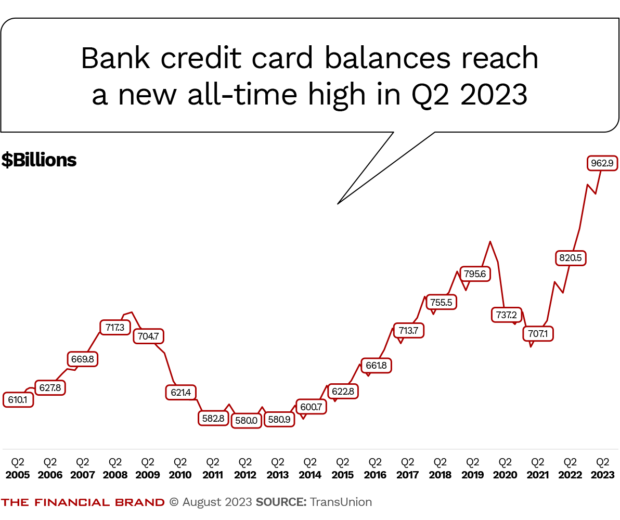

Bank credit card balances rose to $963 billion in the second quarter of 2023, setting a new record, according to TransUnion. This total was 17.4% higher than the year-earlier level.

Average bank credit card debt per borrower rose in the second quarter to $5,947, an increase of almost 13% over the year-ago average. The average is the highest level seen in a decade, the credit bureau says.

In addition, the total credit available on bank credit card accounts rose for the fifth consecutive quarter to $4.5 trillion, a year-over-year increase of 9.6%.

But, while the available credit continues to grow, cardholders’ level of use has been steady, TransUnion says. The average level of use stayed below 22% of the total credit available in the second quarter. This reflects, in part, that the average number of credit cards per person has been rising. This helps keep the balances in each account within normal levels of use.

Balances overall are going up, though, because of the impact of inflation on prices in key categories.

Credit Card Delinquencies Are Rising:

With average bank credit card balances rising, TransUnion advises lenders to monitor deterioration closely. The percentage of card borrowers who are 90+ days past due hit 2.06% in the second quarter, versus 1.57% a year earlier.

Another way of looking at balance growth is by credit tier. Across all tiers, growth in the second quarter hit double digit percentages compared with a year earlier. However, quite a range was seen.

Among subprime borrowers, balances increased 48.6%, and among near-prime borrowers, 27.4%. The increases were much smaller for other credit tiers, with prime cardholders at 13.85%; prime plus, 10.1%%; and super prime, 14%.

See all of our latest coverage of credit card trends.

Banks Still Actively Pursuing New Cardholders, But Getting Pickier

Originations in credit cards — new accounts opened — remain high, but a significant change TransUnion flagged is that banks have been reducing their exposure. Specifically, these card issuers have been opening new accounts mostly for consumers rated prime and above, while reducing card originations for near prime and subprime applicants.

That’s a notable change. Origination growth in the first quarter of 2022 was driven by subprime and near prime. By comparison, prime and above accounted for the origination growth in the first quarter of 2023. (TransUnion reports card originations one quarter in arrears to account for reporting lags.)

Lenders are not generally reducing the credit lines of near-prime and subprime borrowers, according to Michele Raneri, vice president of U.S. research and consulting at TransUnion. “It means we are starting to see signs of people with subprime credit having a little bit harder time getting credit when they are applying for it,” she says.

The megabanks talked up credit card loan growth in their second-quarter earnings calls and played down a deterioration in credit quality.

Bank of America, for example, opened 1.2 million new card accounts in the second quarter. Chief Financial Officer Alastair Borthwick, speaking during the bank’s earnings briefing, described the growth in this loan sector as strong. “Credit card growth reflects increased marketing, enhanced offers and higher levels of account opening over time,” he said.

BofA’s credit card chargeoffs were 2.6% in the second quarter. Despite the fact that this is an increase from the previous quarter, the level “remains well below the 3.03% pre-pandemic rate in the fourth quarter of 2019,” Borthwick said.

The bank increased its loan reserves by $448 million in the second quarter, chiefly due to credit card growth.

In discussing a similar erosion in credit quality at JPMorgan Chase, its CFO, Jeremy Barnum, said, “We still see this as a ‘normalization,’ not a deterioration story when we talk about consumer credit.”

Read more:

- Reality Check: Overall Debt Declines for Average American

- Will FedNow and BNPL Dent Credit Card Use?

Generation Z Grows into Spending with ‘Plastic’

TransUnion found that Gen Z consumers are turning to bank credit cards and unsecured personal loans even though some lenders are tightening their credit underwriting.

A TransUnion pulse report for July 2023 found that 50% of Gen Z borrowers plan to apply for new credit or to refinance existing credit within the next year. In the year-earlier pulse report, only 41% of Gen Zers had such plans.

Uptick in Gen Z Credit Appetite:

Percentage of Gen Z borrowers who said in July that they plan to apply for new credit or to refinance existing credit within the next year:50%

By contrast, among the population as a whole, 32% were planning to apply for new credit or to refinance. (This includes all types of credit — student loans, credit cards, personal loans, auto loans and leases, and mortgages.)

Raneri says the Gen Z shift was expected. “We have been watching Gen Z for several quarters, recognizing that they were coming of age and increasing their credit usage.”

What’s newsworthy, she says, is that the growth in use for this segment is outpacing other generations.

Gen Z’s total bank credit card balances increased 51.9% year over year in the second quarter. To put that into perspective, their balances represent 5.7% of overall balances, so this isn’t a tsunami. (The percentages for other generations are: Silent Generation, 4.1% of overall balances; Baby Boomers, 27.5%; Generation X, 33.8%; and Millennials, 28.8%.)

Asked how lenders should react to the significant change for Gen Z, Raneri says it’s important that lenders understand the need to communicate differently with Gen Z. She suggests emphasizing social media promotion, for example.

“The other thing is to recognize that most of these people will have thinner credit files,” Raneri says, “and a thin file doesn’t necessarily mean that they are a bad risk. Evaluating consumers and seeing that they don’t have as much credit experience means the lenders will need to have policies to accommodate that, to be able to extend them credit.”

Read more:

- Zillennials: The Millennial & Gen Z Mash-Up with Unique Financial Needs

- TD Bank’s No-Interest Credit Card: Niche Product or Trendsetter?

Unsecured Personal Loans Hit New Record

The total for unsecured personal loan balances grew to $232 billion in the second quarter, which is the highest level that TransUnion has on record. While growth has been continuing, the second quarter’s year-over-year growth rate of 21.1% reflects the third consecutive quarter of slower growth. TransUnion attributes this to lenders’ shift towards higher credit tiers in recent months.

The average balance hit a record level too — $8,558 — although this is somewhat skewed because the super prime category saw the highest level of growth and those consumers typically obtain larger personal loans.

Over the last 12 months, the mix of lenders that account for unsecured personal loan volume has changed dramatically. Overall, the share of originations in the first quarter of 2023 ranked this way: finance companies, 33.6%; fintechs, 26.5%; credit unions, 22.1%; and banks, 17%. (Originations are reported one quarter in arrears to account for reporting lags.)

The share for finance companies has been relatively steady in recent years, but not so for other providers. Many fintechs have been backing away from personal loans, so their share of originations in terms of number of loans fell by more than 10 percentage points. They had accounted for 37.9% of originations in the first quarter of 2022. During a second quarter earnings briefing LendingClub, a fintech personal loan specialist that became a bank via acquisition, noted that it had reduced originations in part because some bank buyers of its stream “are currently moving to the sidelines as they address their capital and liquidity concerns. And their pullback will have an impact on our near-term origination volume.”

Banks, on the other hand, bulked up on these loans, as did credit unions. Banks’ share of this lending had been at 11.4% a year earlier, and credit unions, 16.8%.

Read more:

- Inflation Is Changing People’s Money Habits: 7 Studies Show the Trends

- NCUA Chief’s Top Worries: Deposit Pressure, Loan Pricing and Fintechs

One Type of Personal Loan Borrower Tends to Be a Better Credit Risk

TransUnion analysts looked at personal loan usage and found some key differences in behavior.

Overall, consumers who used personal loans to refinance credit card balances generally showed better credit performance than people who used personal loans to refinance their previous personal loans. Credit card refinancers also perform better than personal loan borrowers who use the loans for vacations and other spending, says Liz Pagel, senior vice president of consumer lending at TransUnion.

Pagel theorizes that people who use personal loans to make credit card debt more manageable are generally “a little bit more financially savvy” than the other borrowers.

“They understand the interest rate arbitrage of taking something from a higher-rate balance on their card to a lower-rate personal loan,” says Pagel, “and they’re interested in paying off the debt, because as soon as you get a personal loan, you have to make a substantial payment every month.”

That’s as opposed to making only minimum payments on card balances, while higher card interest rates continue to accrue. Taking that big chunk off of a credit card typically results in an immediate uptick in the consumer’s credit score.

“As I talk to lenders, I tell them this is a pretty decent population to go after, because they do perform better” than other personal loan borrowers, Pagel says. “There’s a real opportunity to send a message to consumers to say, ‘Interest rates have gone up and the rate on your credit card is likely among the highest you pay. You can save money refinancing with a personal loan.'”

Pagel had expected even more growth but says a rebound in home equity lending has siphoned off some of that. On the other hand, unsecured personal loans can be obtained in a fraction of the time needed to obtain home equity loans and home equity lines of credit. A few years ago, she adds, 0% balance transfer offers by card issuers also took away some of the demand for personal loans, but those offers have mostly disappeared as rates rose.

Not all of the debt consolidators retain the benefit of using personal loans for this purpose, however. A TransUnion study found that, among personal loan borrowers in 2021 and 2022, the debt consolidators slashed their card balances by an average of 57%. However, their card balances returned to close to their previous levels within 18 months of the consolidation.

Read more: Upgrade Expands Credit Card, Loan Lineup for Wider ‘Mainstream’ Appeal