In April of 2018 (two years after the introduction of Marcus by Goldman Sachs), I wrote the first of several articles about the Marcus brand, entitled, “Marcus by Goldman Sachs: The Future of CX + Fintech in Banking?”

The article stated: “Goldman expects its new consumer banking business to make $1 billion a year in revenue by 2020. That is a very small component of the overall revenues of Goldman Sachs, but the combination of services, and the fact that consumers are increasingly migrating toward digital channels for financial needs, means that Marcus could be a model for the digital bank of the future.”

Some of the major advantages I pointed to were that Goldman Sachs had significant corporate brand recognition and the deep pockets necessary to create partnerships and to support Marcus in the early stages of development. For example, in 2017, Goldman sent out 178 million pieces of direct mail for Marcus, bought television ads during the NFL playoffs, and did massive digital ad campaigns.

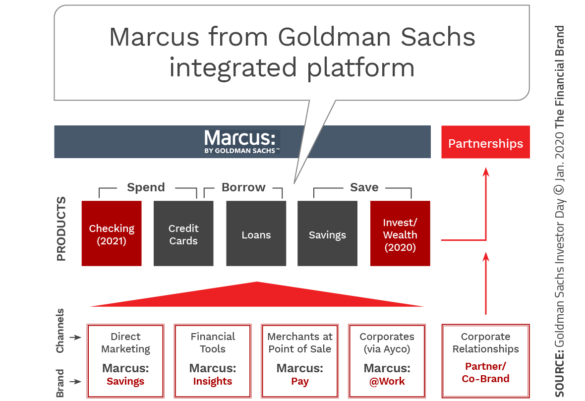

Marcus was built on API technology, leveraging the support of a massive engineer base at Goldman. The firm hired mobile developers to enable the creation of its digital bank, with the intention to offer native mobile apps and a consumer checking account in the future.

And yet, Marcus became the most recent example of a failed attempt to build a digital consumer bank with a scale that could disrupt traditional retail banking organizations.

Read more:

- Marcus by Goldman Sachs: Perfectly Positioned Post-Pandemic

- Marcus: A Digital Bank That Should Keep Rivals Up At Night

- Inside Goldman Sachs’ Plans for Marcus to Be the Dominant Digital Bank

What Went Wrong with Marcus?

Despite all of the investment in the Marcus brand, the partnerships developed to jump-start product lines and to create a significant customer base, why is Goldman Sachs retreating from the mission announced to great fanfare in 2016 in the U.S., 2018 in the U.K., and reinforced each year since?

There we a number of challenges faced over the past several years. First and foremost, outside observers, as well as Goldman Sachs executives, will point to the inability for Marcus to meet financial expectations. For instance, Goldman’s credit card loans had a loss rate of 2.93% in the second quarter of 2022. According to a September note from JPMorgan, that was the highest loss rate among big U.S. card issuers and “well above subprime lenders.”

These losses are expected to get worse in an uncertain economy since many of the credit card customers have lower FICO scores. Bloomberg reported that Marcus’ losses could climb to more than $1.2 billion in 2022, taking cumulative losses to more than $4 billion. This compares to a projection made by Goldman that revenues for Marcus would exceed $4 billion by the end of 2024.

Financial losses weren’t the only challenge faced by Marcus. There were continuous product delays (especially with the introduction of a digital checking account), leadership turnover and staff departures (three different executives heading the division since 2021), numerous rebranding efforts that created confusion in the marketplace, and a probe by the Consumer Financial Protection Bureau (CFPB) looking into Goldman’s credit card business.

Finally, as losses mounted, deadlines were missed, and key executives went to competing organizations, there were increasing disagreements over strategy and priorities that pitted chief executive David Solomon against the leadership team of Marcus. Central to the disagreements was Solomon’s insistence of introducing a cloud-based checking account product and the decision to create the majority of new products in-house as opposed to leveraging outside providers that could create solutions more efficiently and at scale.

Read more: Marcus Acquires Fintech Firms to Become Dominant Banking Power

What Goldman Sachs Got Right

Despite the challenges that resulted in the demise of the Marcus brand as envisioned, there were still several successes. The introduction of the Apple Card by Goldman in 2019 is considered by many as the company’s biggest success in terms of gaining consumer lending scale. It’s the largest component of the banking division’s 14 million customers and $16 billion in loan balances, with a potential to nearly double to $30 billion by 2024.

Marcus also has managed to attract more than $100 billion in deposits offering higher interest rates on accounts with no fees – providing Goldman with cheap funding. It also built strong partnerships with the top brands in the world including Apple, Amazon, Walmart, JetBlue, AARP and General Motors. Most recently, it bought BNPL provider GreenSky, giving Marcus not only a flexible payments option but also direct access to another customer base of 10,000 merchants in the home improvement space.

See all of The Financial Brand’s latest coverage of Apple.

What’s Next for the Marcus Brand?

As opposed to simply closing down the Marcus brand entirely, Goldman Sachs is folding Marcus into the firm’s asset and wealth management division as part of a recently announced reorganization.

David Solomon, told CNBC that placing Marcus within the wealth management business was a “better place for us to be focused than to be out massively looking for consumers.” Solomon added: “The concept of being broad with a consumer footprint is not really playing to our strengths. But when you look at our wealth platform … the ability to add banking services to that and align it with that actually plays to our strength.”

The new strategy will be to focus on expanding relationships with the Marcus customers it already has, while also marketing fintech products through the bank’s workplace and wealth management channels. Examples of expansions of fintech partnerships include a new buy now, pay later (BNPL) product in partnership with Apple and a recently announced high-rate savings product within the Apple Card wallet that will be administered by Goldman Sachs.