In 2016, Goldman Sachs started a consumer lending business focusing on clients looking to refinance credit-card debt. under the brand Marcus, named after founder Marcus Goldman. Previously known as a firm that catered only to the ultra-rich (minimum investment of $10 million for wealth management relationships), customers today can open a Marcus savings account with as little as $1.

“Marcus is evolving from a single offering to a multi-product business that I believe will move the needle for the firm over the coming years,” stated chief executive officer, Lloyd Blankfein. Bottom line, Marcus wants to provide a consumer-friendly, digital financial destination for the masses.

The goal was to quickly become a major player for deposits and loans without ever hiring a teller or building a physical branch. The clarity of their offerings illustrate the differentiation they are trying to establish in the marketplace.

PERSONAL LOANS

- No fees. Ever.

- Fixed interest rates throughout the life of the loan

- .Ability to choose monthly payment dates and options.

- Dedicated loan specialists based in the US who deliver live, personalized support.

ONLINE SAVINGS ACCOUNTS

- Rates higher than the national average.

- No transaction fees.

- FDIC insured to the maximum allowed by law.

- Dedicated saving specialists based in the US who deliver live, personalized support.

Read More: 5 Ways to Make Sure Your Rebranding Project Doesn’t Fizzle

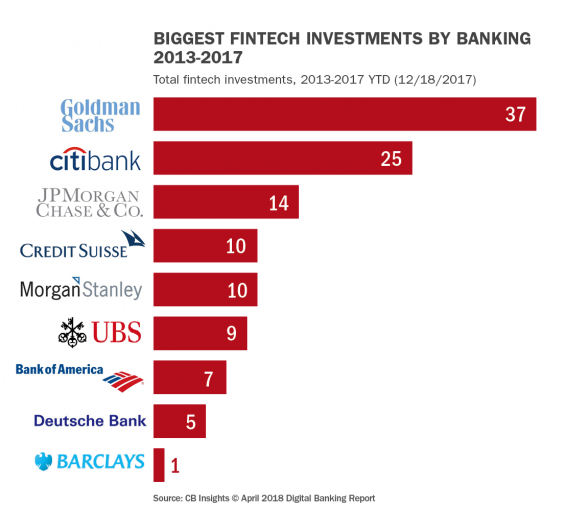

The Largest Fintech Acquirer in the U.S.

Since the establishment of the Marcus brand, Goldman has been one of the most active acquirers of fintech start-ups, acquiring 37 firms. Many of their investments in the most recent past have focused on lending and POS with their additions of Nav, Better Mortgage and Neyber. At the end of 2017, Marcus had more than $2.3 billion in loans and $17 billion in deposits.

As additional evidence of Marcus’ plans of becoming a mass market digital consumer bank, Goldman is in final talks to acquire Clarity Money, an app founded by Adam Dell, the brother of Michael Dell. It uses artificial intelligence to help consumers make better financial decisions by canceling or lowering bills, finding a better credit card or creating a savings account.

It had already acquired Oakland, California-based credit-card startup Final, which offered consumers a credit card with digital features designed to protect against fraud and theft. Final could generate unique virtual cards specific to each consumer-merchant relationship, sending digital receipts to allow consumers to monitor spending.

With Final, Goldman added engineers and product managers with experience building a consumer finance product from scratch. “We are eager to find experienced teams of talented people who have proven themselves to be consumer-centric in their approach to consumer financial services,” Omer Ismail, chief commercial officer of Marcus, said in a statement provided by the bank.

To fund loans at the time of immediate need, Marcus has partnered with Intuit Inc., the maker of financial and tax-management software, to offer loans to their customers. With its expansive data, and easy to use service, Intuit will be able to recommend Marcus products to its user based on their specific needs.

It has been speculated that the unit may also start providing POS financing for Apple’s iPhones, according to The Wall Street Journal. Customers purchasing a $1,000 iPhone X could take out a loan from Goldman instead of charging it to credit cards that often carry high interest rates.

With small POS loans seamlessly integrated into the checkout experience of merchant partners, it is far easier to convert shoppers into borrowers. This business has vast potential and is perfectly suited to a banking organization with a digital focus and lower operational costs.

One of the differentiators of the Marcus loan is that it is totally customizable. As opposed to traditional loan terms (12-months, 18-months, 2-years or 4-years), a borrower can set their terms based on how much they can afford to pay each month. This may result in an 8-month, 14-month or 40-month loan. A borrower can also set and change their monthly payment date to fit their payroll schedule. There are also no origination or prepayment fees.

It is believed that many other fintech acquisitions are in the works.

Read More: Fintech Adoption in North America Lags Global Acceptance

A Platform Approach to Banking

With a stated goal of being considered a technology company instead of a bank, Marcus/Goldman has taken a platform approach to building their digital bank. “Our competitors are generally structured in deep vertical silos and we have a different architecture: these shallower silos built on top of many layers of software, tech infrastructure, cyber security, enterprise platforms and increasingly, client platforms,” stated Marty Chavez, an engineer and Goldman Sachs CIO-turned-CFO.

Unlike a traditional bank, Marcus doesn’t want customers to have a fractured or siloed view. “As we broaden and add several products down the road, we want one user experience,” states Marcus executives.

Marcus is redesigning the entire company around APIs with a third of the employees at Goldman being engineers. The firm is hiring mobile developers to enable the creation of its all-digital retail bank, with the intention to offer native mobile apps in the future.

Designing around APIs and building a digital bank doesn’t mean the omission of human engagement. As an example, all the borrowing calls to Marcus are handled by loan specialists. After extensive research and surveying, Goldman found that customers preferred to speak with human advisers as opposed to robo advisers with their borrowing and savings questions. So all of Marcus calls are answered by loan or deposit specialists, improving the customer experience.

Speaking of robo advisors, Goldman is thought to be considering a digital wealth-management platform that it may roll out this year. Leveraging computer algorithms to buy and sell stocks and bonds for very low fees, Marcus is likely to supplement its robo advice with humans, similar to the deposit and loan business in place already.

Springboard for Future Growth

One of the major advantages Goldman Sachs has with the Marcus brand is corporate name recognition (not yet with the Marcus brand, but certainly with the Goldman brand). This is one of the primary reasons smaller start-ups need to find partnerships. When asked about the Marcus brand recognition, Goldman executives state, “It’s not just Marcus. It is Marcus by Goldman Sachs. There is a high familiarity with the brand and people want to engage with Goldman. … We are creating a user experience that is tethered to the mother brand.”

The other benefit Marcus has in the marketplace compared to traditional fintech firms is deep pockets. “There will certainly be some fintech firms that are able to go solo, but there are many who don’t think they could succeed without partnerships,” states Bill Sullivan, Capgemini’s global head of financial services market intelligence. “When we think about some of the challenges that fintech firms have, it’s things like scale and distribution, which they can only get through partnerships,” he added. Marcus has the corporate financial support to go it alone.

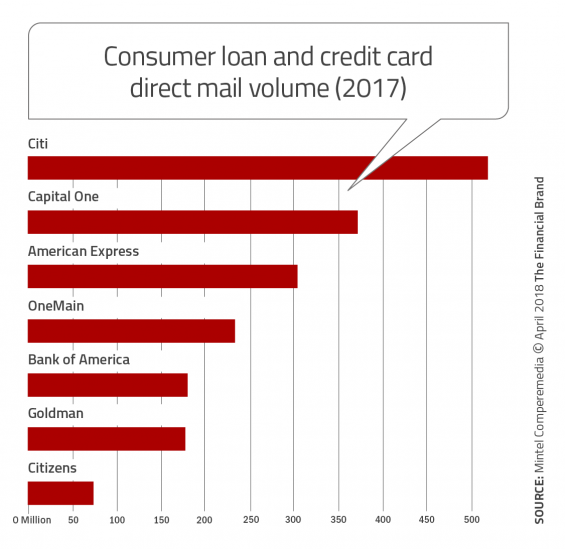

This allows for marketing most other fintech firms could only dream of. For instance, Goldman sent out 178 million pieces of direct mail last year for Marcus and bought television ads during the NFL playoffs. Online marketing for Marcus has, at times, been heavy on Facebook and includes retargeting as part of a digital strategy.

IWCO Direct suggested direct mail was used by Marcus for four reasons:

- Consumers trust direct mail.

- Direct mail has a personal touch that can’t be felt on a screen.

- Direct mail can be highly personalized.

- Direct mail has a shelf life.

Although the bank doesn’t offer the traditional checking and cash withdrawal services, this may not be a disadvantage given that a large segment of consumers are moving in a cashless direction, adopting P2P payment options like Venmo and Zelle. Many consumers have also embraced debit card driven relationships that have no checks, like Moven and Simple.

Goldman expects its new consumer-banking business to make $1 billion a year in revenue by 2020. That is a very small component of the overall revenues of Goldman Sachs, but the combination of services, and the fact that consumers are increasingly migrating toward digital channels for financial needs, means that Marcus could be a model for the digital bank of the future.