Was this the first line of an obituary?

“Ally Bank, the largest digital bank in the U.S…., eliminated overdraft fees on all accounts today. Every Ally Bank customer is eligible, and there are no requirements or restrictions.”

Some think that overdraft fees — and traditional overdraft policies — are dying, and good riddance. Ally’s announcement came in the wake of Senate Banking Committee hearings in which Sen. Elizabeth Warren roasted major banks over their pandemic period overdraft charges.

Warren, whose longstanding opposition to overdraft fees is no secret, asked JPMorgan Chase’s Jamie Dimon if he would refund $1.463 billion in pandemic-era overdraft charges. Dimon said “No.”

Split Opinion:

The truth about the banking industry is, while some bankers have loved the idea of overdraft fees, it’s never quite sat right with others.

Many bankers recoiled from the idea of reordering debit items by amount versus date of arrival so large checks like mortgage payments would be paid first — but potentially triggering multiple overdraft charges when smaller items hit the account. Others, with straight faces, spoke of the importance of covering such important payments. That the practice happened to produce lots of fees was only “incidental.”

On the other hand, the argument has often been made that you shouldn’t spend more than you have in your checking account. But widespread talk these days about many people being paid too little to make it on their salaries over the course of a month have pushed that kind of talk to the side.

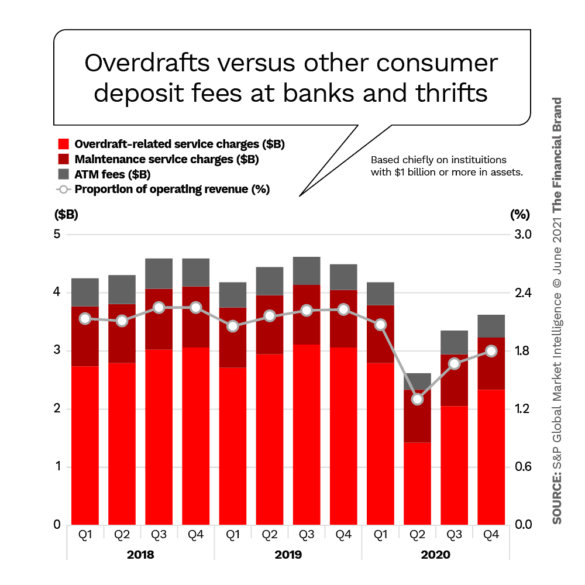

Ironically, fees collected during 2020 were down, due both to waivers and less spending, triggering fewer overdrafts.

What seems to be changing now is that attitudes about overdrafts are becoming more strident at the same time that technology makes it possible to change the way overdrafts are handled. PNC’s new Low Cash Mode, for example — covered later — puts nearly every decision regarding a potential overdraft literally in customers’ hands, through the bank’s Virtual Wallet app.

Beyond this, one of the selling points of certain fintechs and neobanks is that they don’t charge overdraft fees. Chime, for example, promotes its SpotMe service, which permits overdrafts of $200 or more, the amount subject to the fintech’s experience with the consumer and other requirements.

Thus, market forces and politics are both pushing for a fresh look at overdrafts.

What’s Bringing the Industry to a Decision Point

In the old days, people just bounced their checks and got red-faced and charged fees by merchants. Credit lines attached to checking accounts were available to those with good scores, in some institutions. Fee-based overdraft service has been around for a couple of decades. It began as simple courtesy by institutions honoring checks with insufficient funds and calling the accountholder to come in and tot up the account asap. This saved people embarrassment from having checks bounce all over town. Then the thought of making money off the service came about, at a time when community bank margins were eroding.

The popularity among bankers of free checking — which came about in part with the thought of more accounts generating more fee income from overdrafts — spread quickly. Then a small but persuasive group of consultants began showing banks how to generate more overdraft income in ways that bankers often justified on a customer service basis but which never really passed the smell test.

Laws and regulations came, but people kept overdrafting and expecting to be covered by their banks or credit unions.

Regionals Are Moving on Overdrafts:

The point has been made that in spite of Elizabeth Warren’s big bank barbecue, regional banks actually rely more strongly on overdraft fees. That’s beginning to change.

Regions Bank, during an analyst briefing, revealed that it was going to change the order items are posted in. All credits will post first, with debits to post second. The bank believes this will impact positively on many customers because of this and related changes. CEO John Turner stated that “we’ve been anticipating revenue declining as a result.”

How would Regions make up for that? Turner said one advantage was that consumer accounts were growing and that this would boost debit card income. Interestingly, that’s one of the income sources for many neobanks.

Read More:

- What’s the Future for Overdrafts?

- Why Do Consumers Love Fintechs Like Chime and SoFi?

- Walmart’s Fintech Deal Threatens a Much Deeper Banking Incursion

The Ally Bank Impact

In a blog on LinkedIn, Andrei Cherny, CEO at neobank Aspiration, wrote that, “We may well look back at the announcement that Ally will stop charging overdraft fees as the close of the last decade or so of Fintech innovation: Fintech 1.0. … We are now seeing the victory of the first neobanks as banks are dropping egregious fees on overdrafts and ATMs and adopting popular features such as round ups for savings and early pay days.”

Ron Shevlin, in his Fintech Snark Tank blog, had his doubts that Cherny had called it right.

“Banks and credit unions will wait and see who else eliminates overdraft fees. If nobody blinks, the issue goes away. But if a few make the move, there will be a rush, because no one will want to be the last financial institution with overdraft fees.”

— Ron Shevlin, Cornerstone Advisors

On one hand, Shevlin notes that megabanks took in $4 billion in overdrafts in 2020 and that is a lot of money to give up. On the other, he points out that minorities pay a large portion of overdraft charges and killing the fees would provide favorable publicity. In addition, it would look better to “volunteer” than to wait for a Consumer Financial Protection Bureau run by President Biden’s appointee to impose an end to fees.

Shevlin suggests that Chase bite the bullet and kill overdraft fees and force the industry’s hand. As of mid-June 2020, that hadn’t happened.

Steps Institutions are Taking to Address Overdraft Controversy

Since 2021 began, and sometimes earlier, banking institutions have been introducing various approaches to the overdraft issue, ranging from elimination of overdraft penalties entirely to establishment of substitute lines of credit. Here are some of the most significant moves.

Ally Bank began its no overdraft fee policy in late May 2021, deciding to continue a no-fee policy from the pandemic. The Financial Brand asked if overdrafting would still be possible or if checks would be returned and debit card transactions declined. The answer: “No, we don’t reject everything once you’ve hit zero. We’ve always given customers a fee-free $10 buffer and try to offer ways to help customers on items that may take them negative. While we won’t charge an overdraft fee, there’s a good chance that the person or company who received the check may still charge a fee since it wasn’t paid.” Consumers have six days to bring their account back to a positive balance.

Alliant Credit Union announced in August 2021 that it was doing away with overdraft fees as well as non-sufficient funds charges. Initially overdraft and NSF fees were going to be refunded, until the credit union could make system switchovers to avoid charging the fees in the first place. Overdrafts will still be permitted, but won’t be charged for.

Fifth Third introduced Momentum Banking. This account includes Extra Time, which provides more time to make a deposit, in order to avoid overdraft fees. The funds must be deposited before midnight of the business day the account is overdrawn. They must cover the overdraft plus any other charges to the account that come through the same day.

Frost Bank added a new feature to its overdraft offerings: $100 overdraft grace. People holding Frost Personal and Frost Plus accounts won’t be charged any overdraft fee if they overdraw by $100 or less. One proviso is that they have monthly direct deposits of at least $500.

Huntington Bank offers several features to reduce overdrafts. Safety Zone eliminates fees for overdrafts that cause negative balances of under $50, for example. The bank also offers a 24-hour grace period to bring the account current. In addition, Huntington has been rolling out Standby Cash, a digital-only line of credit based not on credit score but on checking, monthly deposits and overdraft history. Advances must be paid back within three months. If automatic repayments are agreed to, there is no interest nor fees for the advances. Otherwise payments at 1% monthly interest (12% APR) are due. (For comparison’s sake, if a $35 overdraft fee had to be paid back for an advance of $1,000 in three months, that would be the equivalent of 14% APR.)

KeyBank introduced Key Smart Checking, an all-digital account, in August 2020. Among its features is the ability to add a “$0 Overdraft Protection Option” by linking a savings account to Smart Checking.

PNC added a new feature called Low Cash Mode to its Virtual Wallet line. Accountholders can see what charges are going to hit their account and if a shortfall is indicated, they can change the order in which checks and ACH transactions are processed, in order to avoid overdrafts “rather than the common industry practice of the bank making the decision.” Customers can actually choose to return an item for later presentment. (Any penalty for that is between the merchant and the consumer.)

Real-time alerts enable the customer to know when their balance is low, based on a threshold preset by the customer. If the balance is already negative, the service provides at least 24 hours of “extra time” to prevent or address overdrafts before fees are charged. The bank’s mobile app shows a countdown clock for bringing the account balance current.

The customer can set up “protecting accounts,” permitting automatic transfers, or can opt for other ways to restore the balance to at least $0. This includes options to make a mobile deposit, to transfer from another account besides the protecting accounts, to find a branch to make a physical deposit, or to reach out to friends or family for a transfer via Zelle.

PNC Will See Revenue Impact:

A PNC pilot among almost 20,000 customers reduced overdraft fees by more than 60%, according to the bank. The service permits at most a $36 overdraft fee per day.

“PNC expects to help its customers avoid approximately $125 million to $150 million in overdraft fees annually,” the bank said in a statement. “PNC’s full year 2021 revenue outlook anticipated this fee reduction, and as a result is not impacted by this change.” In a statement the bank said it hoped this would help drive growth as PNC expands its branch network nationally.

TD Bank announced plans to introduce TD Essential Banking, a low-cost checkless deposit account. The account will have no minimum daily balance requirement. There will be no overdraft fees because consumers will not be able to overdraw their accounts. In addition, TD Bank announced, when these accounts go live the bank will also implement changes in its overdraft policies. Prior to this the bank introduced new secured card products, including one with a reduced minimum requirement.