An independent Javelin Strategy & Research white paper sponsored by Deluxe Corp. entitled, Convert Silent Attrition into Banking Engagement and Profits reinforces previous studies that found that acquiring new customers and members is not as important as making sure these new relationships are effectively onboarded and that the status of being the consumer’s ‘primary financial institution’ is achieved.

The foundation of the problem is that 20% of new households say it is too difficult to completely switch their relationship from their previous financial institution resulting in dormant/inactive accounts – a status referred to as ‘silent attrition’ in the study. Helping the new household with their switching process can result in the following benefits:

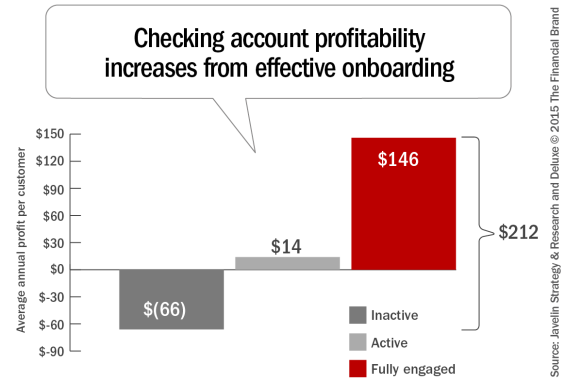

- Profitability can be increased by $212 by turning an inactive customer into a ‘fully engaged’ customer (with bill pay, direct deposit and debit purchases).

- Fully engaged households are 4 times more likely than inactive households to view the new bank or credit unions as their ‘primary financial institution.’

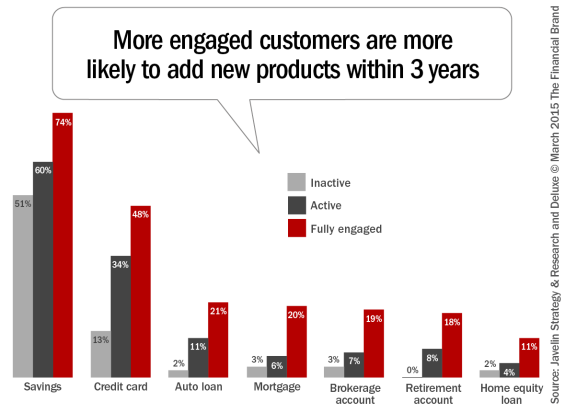

- Fully engaged households own 2.7 more accounts than inactive households and intend to open more new accounts in the next 12 months (3.0 vs. .5).

- Moving the 20% of the households who find ‘switching’ difficult to become fully engaged households will result in an 8% increase in overall profitability from these new households during the first three years. Alternatively, an inactive household will result in a net loss during this same period.

Building Relationships Must Begin Immediately

On average, checking accounts are unprofitable, especially among customers who are disengaged, carry low balances, and do not buy loans and other profitable products.

There is a very distinct difference between acquiring a new account and generating a new relationship. Without an immediate and proactive process of switching the key components of the household’s previous banking relationship, the new account could remain dormant (and costly) for years.

According to Javelin, about 11% of new checking accounts acquired remain inactive. Many of these inactive households may have initially had good intent, but eventually view the new institution as a place to park money, take advantage of a special offer, or to set aside funds for emergencies or specific savings goals.

Javelin states that financial institutions will reap a higher long-term payoff if they focus first on offering new households engagement services before cross-selling additional products. These engagement services include the use of online and mobile banking, direct deposit, bill payment, financial alerts, and personal finance management tools.

While inactive households are the biggest drain on profits, there are also 44% of new checking customers who are ‘active’ – making purchases, or had signed up for bill pay or direct deposit – but were not taking advantage of all three of these features like a fully engaged household. These ‘active’ households provide an easier path to enhanced profitability and a more likely prospect for achieving ‘primary financial institution’ status.

Read More: 21 Steps to Onboarding Success in Banking

The Payoff of Engaged Households

As mentioned earlier, the study by Javelin reinforces research done in the past which showed that fully engaged households are not only more loyal but also are considerably more profitable than households without the key ‘go with’ services (direct deposit, bill payments and debit purchases). Beyond the $212 improvement in profitability mentioned, there is also the payoff on the investment made to acquire the new checking account in the first place (estimated at between $50 – $250 per account).

Even if a financial institution can’t move an inactive household to become fully engaged, the payoff of improved engagement is still beneficial. According to Javelin, an organization can increase the annual profitability of a dormant account by $80 if the household can be moved to the ‘active’ status (2 engagement services), while moving an ‘active’ customer to the ‘fully engaged’ status adds $132 in annual profitability.

Read More: The Business Case for Onboarding

Newton’s Law In Banking

“An inactive account tends to stay inactive and a partially active account tends to stay only partially active unless assisted by additional encouragement.”

— ‘Newton’s Law of Banking’

To gain engagement success, it is imperative to alleviate the frustration of transferring relationships by simplifying the switch process and by providing ongoing onboarding communication that encourages increased account activity. In a variation on Newton’s First Law of Motion as applied to new banking relationships … “An inactive account tends to stay inactive and a partially active account tends to stay only partially active unless assisted by additional encouragement.”

The impact of a seamless switch and onboarding process has additional long-term benefits as well. “By having a simplified switch process in place and by providing incentives for households to move to the next level of engagement will increase a financial institution’s overall profit from all new checking accounts by 8%,” states Javelin. “In addition, more than 4 in 10 fully engaged customers consider the new organization to be their primary banking relationship, compared to fewer than 1 in 10 inactive customers.”

The payoff over time is that engaged households open more additional accounts over time as shown below. This longer-term benefit is why building early engagement is more important than cross-selling additional services in the first several months after the opening of a new account.

Key Engagement Strategies

The Javelin study stresses that becoming a consumer’s primary financial institution requires a simplified process for severing ties with the a household’s previous financial partner, and then encouraging the household to actively use the account for directly depositing checks, paying bills and doing daily transactions. This engagement will eventually lead to an even stronger relationship and increased profitability over time from the sale of new depository, loan, and investment products.

The key components of a successful onboarding process include:

- Promote engagement first, cross-selling later

- Place a priority on ‘go-with’ services (direct deposit, bill pay, debit card activity, online and mobile banking, custom financial alerts, etc.)

- Communicate early and often with personalized and customized communication

- Leverage consumer tutorials and other learning tools

- Simplify the switch process (online, mobile and branch channels)

- Integrate engagement as part of new account packages and processes

- Eliminate processes and policies that encourage ‘silent attrition’

Read More: Bank Onboarding Should Integrate Digital & Mobile Channels

Survey Methodology

Consumer data in the Javelin white paper entitled, Convert Silent Attrition into Banking Engagement and Profits is based primarily on information collected in a random-sample panel of 600 consumers in a December 2014 online survey commissioned by Deluxe, with a margin of sampling error of ± 4%. Supplemental data is based on information collected by Javelin in a random-sample panel of 8,552 consumers in a November 2014 online survey with a margin of sampling error of ± 1%. Profitability calculations are derived from a Javelin ROI calculator that was developed from Javelin consumer survey data, in-depth interviews, and secondary research.