The need to move to a more digital banking model has been talked about for almost a decade, but COVID-19 has made the need for reduced operational costs and improved digital experiences more important than ever. Financial institutions of all sizes must reassess their existing business models, core systems structure, distribution networks, commitment to innovation and product assortment for a marketplace with more demanding consumers, more agile competition and shareholders who are looking for greater efficiencies.

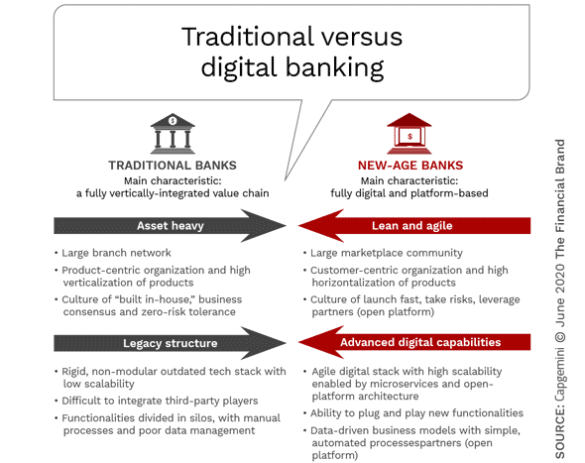

The “new normal” of banking is quickly moving from branch-heavy, product-centric organizations with legacy technologies and cultures to consumer-centric organizations with more personalized solutions that can be delivered seamlessly. According to the World Banking Report 2020, from Capgemini and Efma, those firms that can deliver fully digital, platform-based banking will realize significantly lower acquisition costs, an improved efficiency ratio and much lower costs of distribution.

Legacy banking organizations do not have a choice as the pressure on costs and demand for simple digital solutions have already become extreme. Capgemini recommends a shift to an open banking approach, leveraging third-party solutions, including the partnership with fintech providers. This will include enhancing current legacy systems, embracing an innovation mindset and using customer data and advanced analytics to drive the ability to deliver proactive real-time recommendations.

Read More: Most Financial Institutions Still Making Banking Too Difficult

Data is the Foundation for Banking of the Future

During the COVID-19 shut down, consumers became increasingly aware of the power of digital and the importance of using data to improve the customer experience. From being able to get products ordered in an instant from Amazon, to receiving groceries from Instacart or dinner from Grubhub, consumers saw the benefits of using stored insights to save time.

These types of engagements put a spotlight on those financial institutions that have rich data insights but had failed to leverage the knowledge of their customers to deliver a personalized digital experience. At a time when consumers were craving customized solutions for their individual crisis-related needs, many financial institutions delivered generalized communication with cumbersome solutions. In other words, those institutions that had been “faking digital” were at a significant disadvantage.

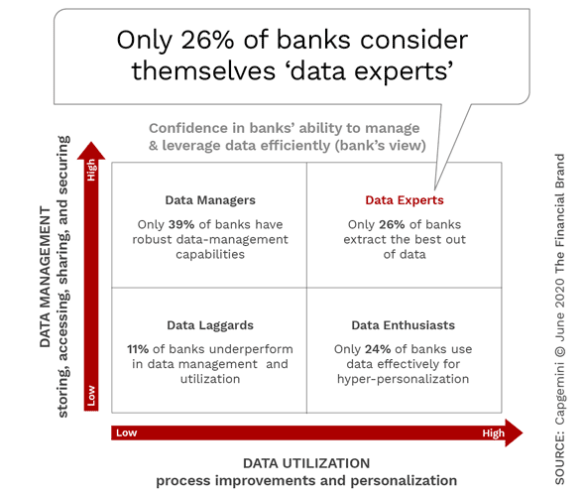

It became clear that just having data was not enough. Firms are being tested to determine if they have a high capability to 1) manage data, and 2) utilize the data for the consumer’s benefit. According to the Capgemini/Efma research, only 26% of financial institutions had the confidence to classify themselves as “data experts.”

Read More: When Opening Accounts in Branches Becomes Impossible

Digital Transformation Requires Innovation Focus

In Efma‘s 9th annual Innovation in Retail Banking report, published by the Digital Banking Report and sponsored by Infosys Finacle, it was found that a key component of successful digital transformation efforts was a strong commitment to innovation. While there are many reasons given for not moving forward with in-house innovation (insufficient budget, competing priorities, lack of project management agility), today’s tech-savvy consumers are demanding the types of digital solutions provided by fintech players.

The impact of the pandemic has forced most organizations to play catch-up. At the same time, advanced technologies have the potential to change the way organizations deliver banking services more than ever. These new technologies include artificial intelligence (AI), the Internet of things (IoT), blockchain, open banking platforms with application program interfaces (APIs) and robotic process automation (RPA).

To reimagine banking in a post-pandemic world, there needs to be a focus on both disruptive technologies and innovation, as opposed to simply moving forward in small steps. The winners in the future will be defined by those organizations that can leverage digital technologies to deliver a customer experience that goes beyond the ordinary. In most cases, this will require a collaboration with fintech and potentially bigtech partners.

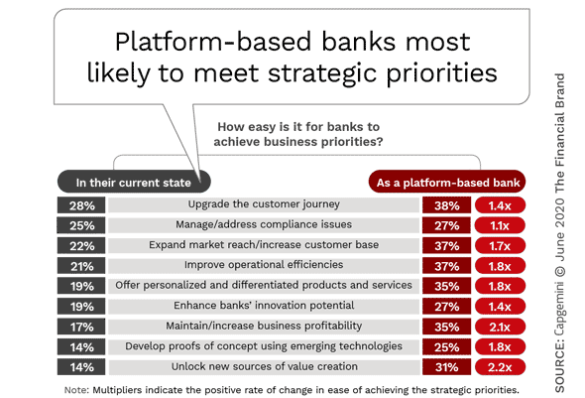

According to the World Retail Banking Report 2020, “Regardless of a bank’s intent or approach to innovation, a platform-based model can offer light at the end of the tunnel. Platforms enable fast and secure ‘plug-and-play’ integration to make collaboration with ecosystem partners possible.”

The Power of a Platform Model

There is no denying the power of platforms in business today. In fact, some of the most valuable companies in the world are platform-based, including Amazon, Airbnb, Uber, Apple, Microsoft and others. Some of the benefits of a platform-based structure include agility and the ability to create value with an ecosystem of interdependent producers, suppliers and distributors. In banking, the efficiency provided by a platform-based model is significant.

Legacy banking organizations must determine the correct platform approach that will align with business goals. Most will not go “all in,” but will adopt more of a hybrid approach that will combine third-party products and services with existing products. In any case, the choice will be whether to build, buy or share a platform going forward.

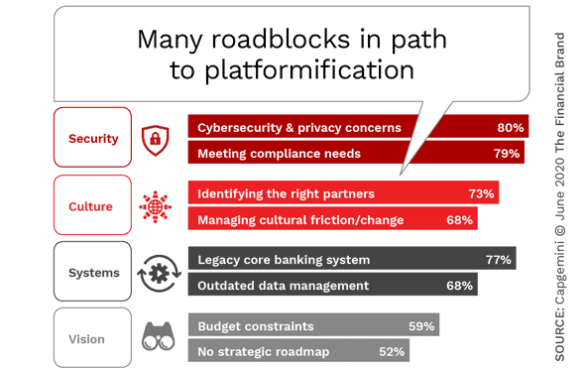

While there are many obstacles on the platformification journey, the rewards are significant and the need for these types of solutions is great. The most significant obstacles are related to security concerns, legacy systems, and finding the right partners, according to the Capgemini/Efma research.

COVID-19 Increases Need for Change

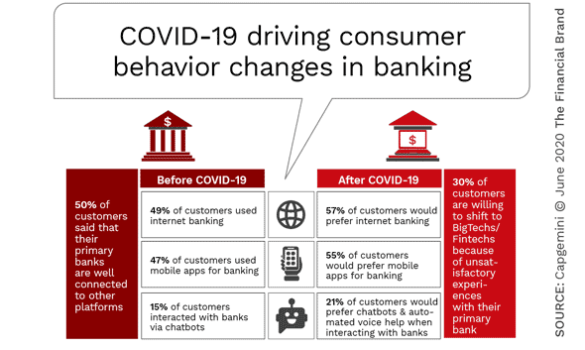

The COVID-19 pandemic moved more consumers to digital channels than any single event in our lifetimes. Consumers who never had deposited a check by taking a photo, transfer funds between accounts using their mobile device or communicated with friends and family using video channels were instantly made aware of the power of digital.

According to research from Simon-Kucher & Partners, a global strategy and marketing consulting firm, 42% of consumers in the U.S. (47% in Canada) said they will reduce branch visits after the COVID-19 lockdowns end. The survey also found that retail bank customer will be willing to travel greater distances to a branch, suggesting an opportunity to reduce branch density; and rising expectations for best-in-class digital capabilities will create new pressure for banks.

The research from Capgemini and Efma found similar results, with consumers increasingly preferring digital engagements with their financial institution post COVID-19. The research also found an increased need for preparation by financial institutions in the following areas:

- Customer centricity

- Operational resilience

- Business awareness