As the banking industry continues to deal with the disruptions resulting from COVID-19, most financial services executives say that innovation is now a prerequisite for them to respond quickly to market challenges and opportunities. In fact, in new research from the Digital Banking Report, innovation leaders in both the legacy banking and the fintech space agree that innovation must have a cultural and leadership underpinning for digital transformation efforts to succeed.

With an innovation culture, financial institutions of all sizes were in a better position as consumer behavior changed in an instant and where employees were forced to work remotely. In all cases, those organizations that considered themselves to have the highest level of innovation maturity thought they were in the best position to recover from the impact of the pandemic financially, structurally and competitively. This is critical at a time when the banking industry may be under new financial pressures.

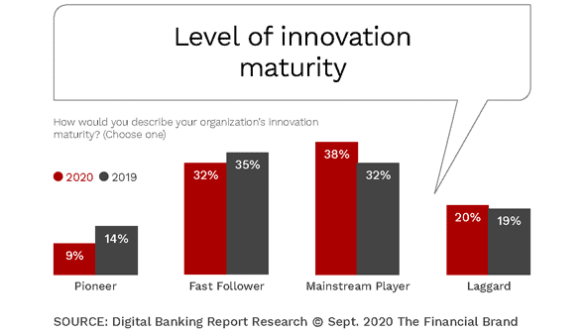

In assessing the culture of innovation maturity framework, we asked financial institutions globally how they viewed their innovation maturity in the areas of data, technology, talent, processes and measurement. As in 2019, the four stages of innovation maturity included 1) pioneer, 2) fast follower, 3) mainstream player and 4) laggard. Our research found that over the past year, despite investing and focusing more on innovation, organizations perceived themselves to have become less mature in the culture of innovation, with a drop of more than a third in the pioneer stage and even a drop in the fast follower stage. This reflects that innovation may be more difficult for some organizations during a crisis or that there was an inability to keep pace with consumer expectations.

As was discussed in the article, “Digital Transformation Success Elusive For Financial Institutions,” while the majority of institutions understand the importance of being positioned to launch new products, change internal processes, adapt to changing consumer needs and leverage data and advanced analytics, most are lagging the fast pace of digitization and innovation of fintech and big tech organizations.

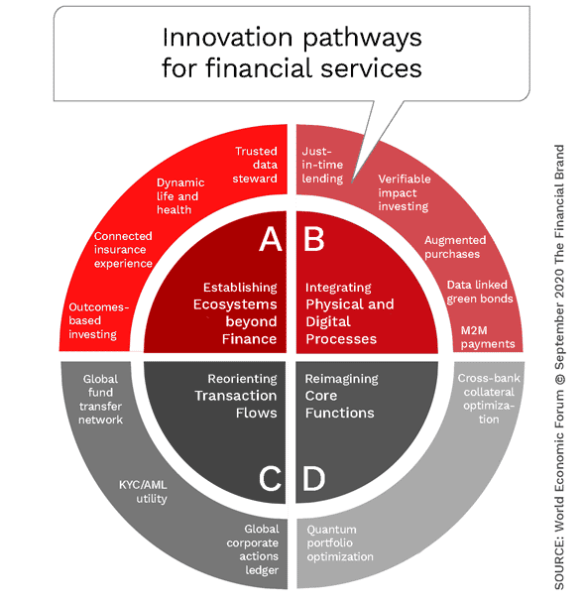

The Digital Banking Report research found that organizations with the highest innovation maturity are completely rethinking their business models, leveraging advanced technologies, understanding their customers and members more fully, investing in upskilling and reskilling and achieving higher rates of growth. As stated in a report by the World Economic Forum, illustrated below, organizations are focusing on four major paths to success.

Read More:

- How to Avoid Digital Transformation Failures in Banking

- Banking Must Bridge the Growing Digital Transformation Skills Gap

Innovation Culture Begins at the Top

All financial institution executives want their companies to be more innovative. They watch comparatively young fintech firms and huge tech giants create and market financial products and services that steal market share and revenues by leveraging data, analytics and new technology. Research done over the past five years by the Digital Banking Report finds that corporate culture is much more important than the size of the company, level of investment, geographic location or even regulatory environment.

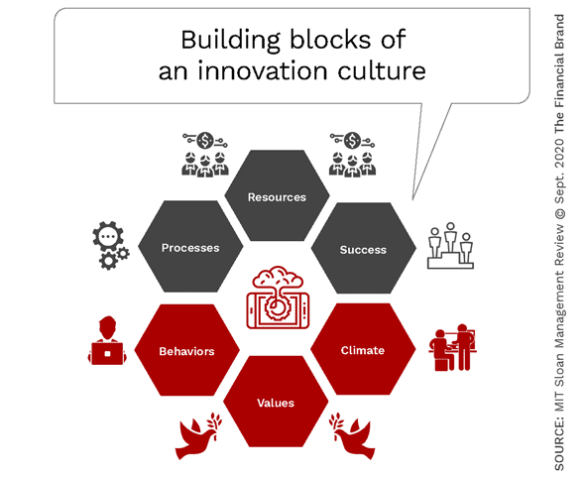

The question becomes: How can leaders build and reinforce an innovation culture within their organization? According to research by Jay Rao and Joseph Weintraub, professors at Babson College and published in the MIT Sloan Management Review, an innovative culture rests on a foundation of six building blocks. These include resources, processes, values, behavior, climate and success. Each of these building blocks are dynamically linked.

The research by the professors is aligned with insights found recently by the Digital Banking Report which shows that increasing investment, changing processes and measuring success is imperative … but not enough. Organizations must also focus on the overarching company values, the actions of people within the organization (behaviors), and the internal environment (climate). These are much less tangible and harder to measure and manage, but just as important to the success of innovation and the ability to create a sustained competitive advantage.

Even the best organizations don’t excel in every area, but innovative companies always have at least one or two of the building blocks solidly in place.

- Processes. This represents the flow that innovations take to move from concept to reality. To succeed, organizations need a process to evaluate, prioritize and fund ideas. Obviously, the more defined and agile, the better.

- Resources. Beyond funding, resources include the technology and people needed to bring ideas to fruition. Not surprisingly, having innovation champions is the most important.

- Success. Measurable on many levels (externally and internally), success is a building block because success funds future innovations. Success also reinforces values, behaviors and processes.

- Behaviors. For both leaders and employees, behavior becomes important when needing to decide between competing innovations and when needing to overcome challenges. During times of crisis, the behavior of leaders and employees differentiate organizations.

- Values. The values of a company are leaders do and invest in more than what they say to investors. Innovative firms invest more on entrepreneurship, promote creativity and encourage ongoing learning.

- Climate. Referencing the internal work atmosphere, where there is enthusiasm around innovation and challenges people to take risks and encourages collaboration as well as independent thinking.

When evaluating how an organization is doing with their innovation maturity, it is important to ask people at all levels of the organization since more senior executives tend to rate their organization more positively than people ‘in the trenches’. There is also evidence that larger organizations are more resistant to change. While the very largest banks and credit unions have shown the ability to spend their way beyond this resistance, mid-sized organizations are tremendously hampered with the combination of legacy thinking and lack of funding to support other building blocks.

Read More:

- Do Bank Management Training Programs Create ‘Leaders of Yesterday’?

- What The Most Innovative Leaders in Banking Have in Common

- Financial Institutions Must Become Digital Innovators

COVID-19 Impact on Innovation Strategies

The banking industry was already under pressure to transform their organizations with data, analytics and new technologies in order to better compete with nimble fintech players and well-funded big tech firms. When the pandemic hit, digital banking use escalated, requiring many firms to build solutions that were not previously prioritized. “Banks had planned for years for disaster recovery if their technology failed, but never planned for disaster recovery if their buildings closed,” stated Chris Skinner, author, speaker and CEO of The Finanser Ltd.

According to the seventh annual global banking survey conducted by The Economist Intelligence Unit in March, 45% of respondents said their strategic response to the COVID crisis was to build a “true digital ecosystem.” This objective of digital transformation was the top response, increasing from 41% of respondents in 2019. This percentage surely went up as the COVID crisis continued into autumn.

For the second year in a row, the key driver for change is considered to be new technologies (66%, up from 42% in 2019), such as artificial intelligence, machine learning, blockchain, the Internet of Things (IoT) and other technologies underpinned by data and advanced analytics. This highlights the importance of these new tools in addressing the competitive threat posed by fintech firms and big tech corporations. It also is in response to what consumers are increasingly expecting from their financial institution. The increased importance of regulations is in response to the rise in security issues as more banks and credit unions increase digital offerings.

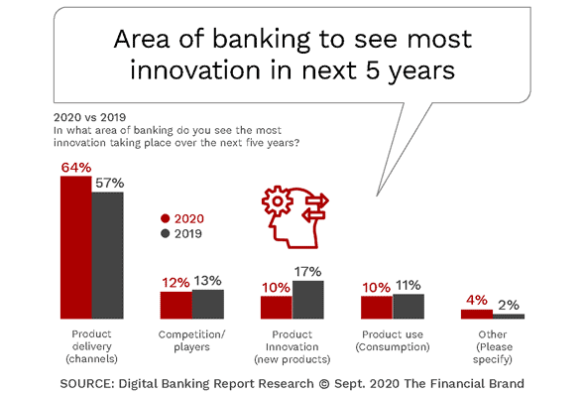

When the Digital Banking Report asked financial services executives globally in August the areas where the most innovation would occur over the next five years, the delivery of products (channels) was by far the most popular answer (64%) with product innovation, product use and competition having much lower responses.

Awareness of Innovation Need No Guarantee of Success

While most organizations believe they are open to respond to identified consumer needs or explore new opportunities, many don’t provide their teams with the guidance or resources to adequately pursue these opportunities. This challenge became even more acute when teams had to work remotely … building new solutions in crisis mode.

The reality is that many leaders want innovation, but they don’t want to alter underlying processes or policies. The result: teams that are handcuffed by legacy processes with a fear of taking risks or disrupting status quo. This is why many solutions simply replicate what was done previously, simply on a different channel. This is akin to putting lipstick on a digital banking pig.

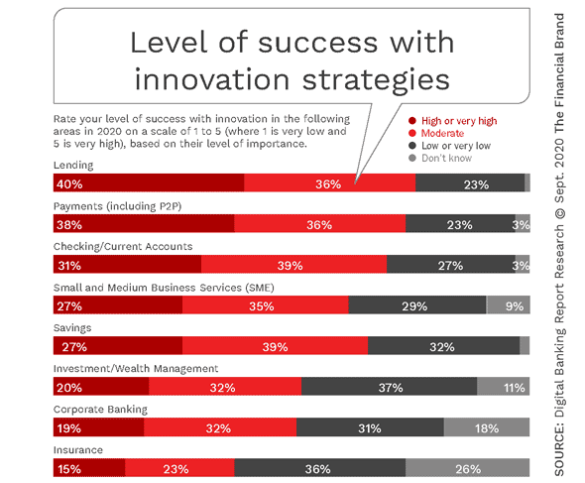

As shown below, the level of success event with traditional products is relatively low. Potentially impacted positively by competitive pressures, the highest levels of innovation success were seen in the lending, payments and check (current) account product lines. Still, most organizations did not give themselves high marks in any product area.

Becoming an Innovative Organization

First of all, becoming an “innovative organization” does not require the development of a large number of “made from scratch” products that don’t already exist. In the vast majority of cases, supporting an innovation culture is more about improving current solutions (digitize, simplify, support across channels) and adopting ideas that are already in the marketplace. In other words, a strong iteration may be better than disruption of what exists.

Secondly, instead of focusing on areas that are not strong, it is usually best to build on your organization’s strengths. For instance, your organization may already have a number of people who have an innovative spirit and can lead the innovation process. By providing them the needed resources to support the organization’s digital transformation vision, innovation can occur.

Finally, it is usually better to focus on a few things and leverage their successes into a broader transformation over time. Cultures change very slowly. If innovation has not been supported adequately in the past, people may show resistance to this new focus. For best results, leaders should aim for small victories — at least at first. According to Jay Rao and Joseph Weintraub, “Small successes will usually trigger a widening circle of improvement. Measurable results are more powerful than arguments, campaigns and mandates: People change when they see their peers becoming more productive, engaged and successful.”