New Competitors Forcing Banks to Reevaluate Innovation Strategies

Innovation continues to be a strategic priority in the banking industry, with new business models emerging including partnerships with fintech startups.

By Jim Marous, Co-Publisher of The Financial Brand, CEO of the Digital Banking Report, and host of the Banking Transformed podcast

Simple Subscribe

Subscribe Now!

As competition expands and consumer expectations for enhanced digital banking services increases, new business models in banking are emerging and being deployed in real applications. Investment in innovation and in technologies like artificial intelligence are transforming the way rich data is analyzed and applied, creating the potential for real-time contextual banking engagement.

The innovation agenda has become intertwined with the digitalization agenda, with both requiring changes in culture and back office operating systems. Investment in delivery channel innovation continues to be the most important focus for the banking industry, responding to expectations set by other industries. The focus in most instances is to reduce costs, improve engagement and make banking easier.

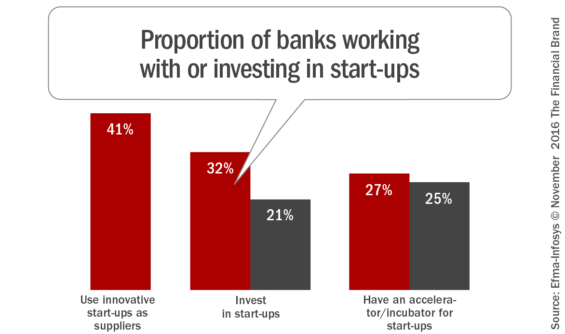

In the 8th Annual Innovation in Retail Banking Report from Efma and Infosys Finacle, banking organizations indicate a shift from viewing fintech as strictly competition, to being potential strategic partners. The study found that over 40% of banks say they work with startups as suppliers, and around 30% of banks are investing in start-ups or working with start-ups in accelerators/incubators.

The Disruptors

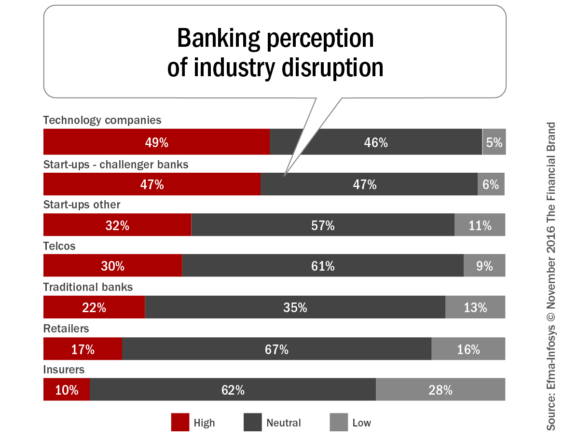

“77% of Banks Believe the Threat From Disruptors to be High or Very High”

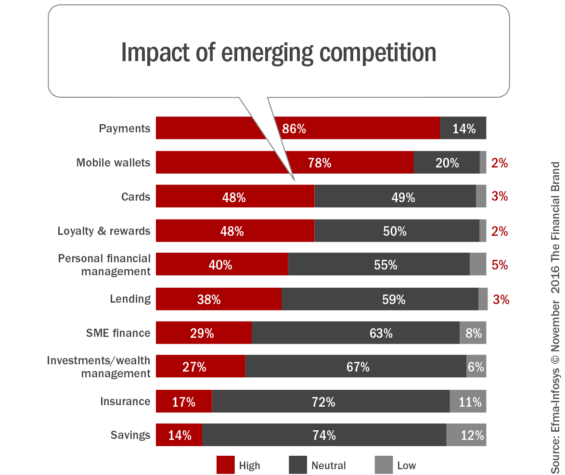

Despite the potential for ‘coopetition’, technology companies, fintech start-ups and challenger banks continue to be be viewed as a triple threat, with 77% of banks believing that the overall threat is high or very high from these players. Payments (86%) and mobile wallets (78%) are the areas where disruptors are expected to have the greatest impact, with products like areas like savings, insurance and investments viewed as having the lowest risk.

Read More: Fintech Use Reaching Mass Adoption Among Digital Consumers

Technology Companies: Technology company disruptors include companies ranging from search, to social media, to retail (e.g. Google, Facebook, Apple, etc.). While not yet being a overall banking threat in most developed countries, each have made advances in the payments space. In contrast, in countries like China and India, technology companies are starting to have a big impact on traditional financial services (Alibaba/Ant Financial in China and Paytm in India being the best examples)

Challenger Banks: The terminology “challenger bank” covers a different types of competitor, some of which are not particularly new (Moven and Simple in the US). Starting a digital-only challenger bank was made easier recently in the UK thanks to changes in banking charter regulations and is less costly than starting a multichannel bank. Some of the more recently introduced challenger banks in the UK include:

- Large challenger (e.g. Virgin Money)

- Small challenger (e.g. Metro Bank)

- Digitally-focused challenger (e.g. Atom Bank)

- Retailer (e.g. Tesco Bank)

Telcos: The threat from telcos has been most prominent in developing countries (M-Pesa in Kenya). While important for the distribution of banking services to underserved markets, the growth rate in the number of services has actually been falling in recent years. Telco competition has been limited in the US and UK, yet telcos and banking partnerships in Poland (T-Mobile/Alior Bank and Orange/mBank) have had modest success.

Emergence of New Digital Banking Models

As expectations for improved digital banking experiences increase, new business models are emerging impacting all areas of the financial services industry. From the initial selling process to new account opening, credit scoring, onboarding of customers, security and customer service, the focus is on simplification and digitalization.

Rather than building all of the capabilities internally, many financial services firms are working with third party fintech start-ups to deliver a more cost effective, digital and contextual customer experience. Beyond digitizing current processes, some firms are embracing the concept of platformification™, leveraging customer insight and established loyalty to become the central provider of both traditional and non-traditional banking services.

Innovation Trends

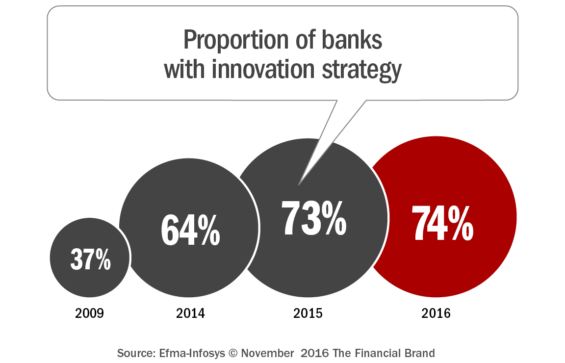

According to the Efma/Infosys Finacle study, the proportion of banks with an innovation strategy has increased marginally in 2016 to 74%. This is only a one percentage point rise from last year, yet significantly than the level in 2009. The slowdown in innovation spending is also reflected in the proportion of banking organizations that have increased spending YOY, where we see a drop from 84% increasing their innovation investment in 2015 to 78% in 2016.

The areas where most banks are increasing innovation investment are customer service/experience (84%) and channels (82%), followed by processes (67%), products (63%) and sales and marketing (56%). Interestingly, 50% of the banks surveyed regarded their innovation performance in channels as high (scoring 6 or 7 on a scale of 1 to 7), with less than one third of banks feeling that their innovation performance is high in any of the other areas.

To help jump-start innovation efforts, many banking organizations are working with start-ups. For instance, the research found:

- 41% of banks are working with start-ups as suppliers

- 32% of banks are making investments in start-ups (vs. 21% in 2015)

- 27% of banks are running accelerators or incubators, internally or externally (vs. 25% in 2015)

Digital Transformation

”50% of Banks Believe Legacy Technology is a Barrier to Digital Transformation”

Organizations are taking vastly different paths to digital transformation. According to the research, approximately 20% of banks are launching or considering launching a digital-only bank. Examples of banks launching digital-only banks discussed in the research are UniCredit (Italy) with buddybank, Caixabank (Spain) with imaginBank and DBS Bank (which launched a digital-only bank in India).

Alternatively, banks like BBVA are acquiring or investing in start-up digital banks. In addition to Simple in 2014, BBVA has acquired a 30% stake in Atom Bank (UK), and 100% of Holvi (Sweden). Similarly, BPCE of France announced it was acquiring Fidor Bank in July 2016. Fidor Bank operates in Germany and the UK. Banks launching digital-only banks will have different products and services, channel applications and back office technology and processes from the core bank.

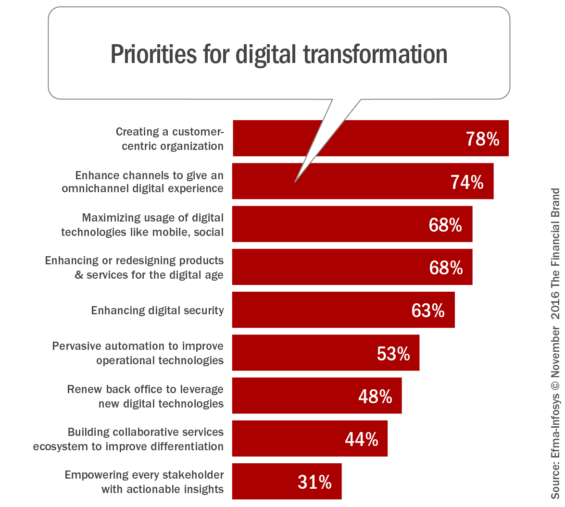

The top digital transformation priorities for banks are creating a customer-centric organization (78%), enhancing channels to give an omnichannel digital experience (74%), maximizing usage of mobile and social technologies (68%) and enhancing or re-designing products and services for the digital age (68%). According to the report, “Part of the reason for launching digital-only banks is to provide this exceptional customer experience without having to link in physical channels to create a seamless omnichannel experience, something which is proving to be a particular challenge with legacy systems.”

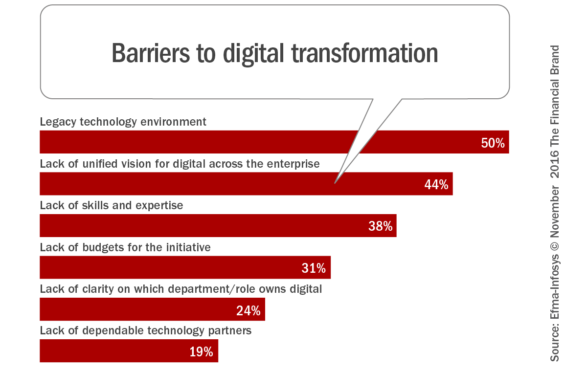

The most important barriers to digital transformation is the legacy technology environment (50%), the lack of a unified vision for digital (44%), and the lack of required skills and experience (38%).

Impact of New Technologies

”73% of Banks Consider Working With Fintech Firms the Best Approach to Deliver New Technologies”

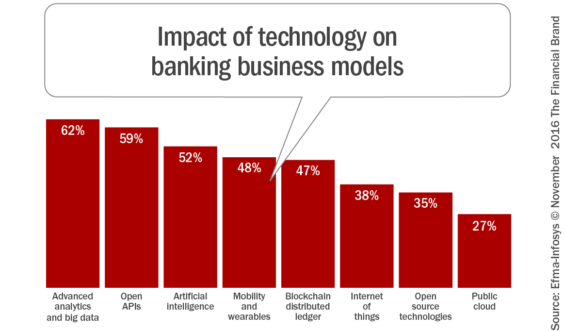

The study asked what impact disruptive technologies would have on business models. The most significant were believed to be advanced analytics (62%), open API’s (59%) and artificial intelligence (52%). Mobility/wearables (48%), and blockchain/distributed ledger (47%) were also expected to have a significant impact.

When asked about the timing of each impact, advanced analytics and big data was expected to impact the industry much sooner (79% believed the impact will be within the next two years), with mobility/wearables (75%) and open APIs (67%) also expected to impact banking in the next two years. Alternatively, artificial intelligence and blockchain/distributed ledger technologies were thought to have a much less likely impact over the next two years (37% and 21% respectively). To some extent, these results correlate with where banks are investing.

In order to deliver these technologies, 73% of banks said that working with innovative start-ups as either suppliers or partners would be important. Also considered important were internal research and development (46%), and working with firms from other industries (42%). Only 20% of the banks surveyed thought that working with traditional suppliers would be beneficial and only 14% would work with other legacy banking organizations.

Open source technologies were not expected to a significant disruptive impact on banking business models by most banks in the near term. Most likely application of open source technology was with analytics, operating systems, and databases.

Advanced Analytics Paradox

”62% of Banks Consider Advanced Analytics and Big Data to Have a Big Impact on Business Models”

As mentioned, 62% of banks believed advanced analytics and big data would have a high impact on the industry. In addition, 79% of the banks surveyed believed the impact would occur in the next two years. That said, only 46% of banks surveyed are investing at a relatively high level in this area. This “advanced analytics paradox” is consistent with what the Digital Banking Report found in research done for the “State of Financial Marketing” issue.

The strategy supporting the use of big data and analytics is machine learning which enables complex models and algorithms to “produce reliable, repeatable decisions and results” and

uncover “hidden insights” through learning from historical relationships and trends in the data. This is the foundation of many of the emerging fintech firms that are appealing to consumers used to firms like Amazon and Facebook that apply learnings to determine what is presented to consumers each moment.

The Future

Banks continue to invest in innovation to keep pace with consumer expectations and in response to the threat of industry disruption. But the race to keep pace is far from over.

Digitalization of banking is moving quickly with many options available. Digitalization of the entire consumer journey is required to cut costs, achieve efficiency gains, and to deliver a better customer experience.

While the benefits of applying big data and advanced analytics across many solution sets has been proven, the investment in these solutions is far from what is needed. Many believe that the application of data for the benefit of the consumer will be the key differentiator in the future. But decisions around innovation prioritization will be required.

According to the research from Efma/Infosys Finacle, small and medium sized banks might be at a disadvantage compared to larger banks when it comes to the ability to invest in innovation. The research recommended the following steps to assist in keeping pace:

- Monitor developments: Make sure your bank is aware of all the critical innovations taking place around the world and understand how these are impacting the business model of banking.

- Focus on culture: Smaller banks will have an advantage over larger banks when it comes to developing an innovation culture so this is an area on which to focus attention.

- Be selective: With limited resources, be very selective and disciplined in choosing areas in which to invest.

- Leverage relationships: Make use of relationships to access innovation at lower cost, for example by partnering with suppliers, start-ups or even other banks.