It would be easy to conclude that bank branches’ days really are numbered, given that they have decreased in the U.S. by more than 13,000 over ten years, while digital transaction usage has surged

But the truth is that at current rates of shrinkage, branches will outlive anyone reading this.

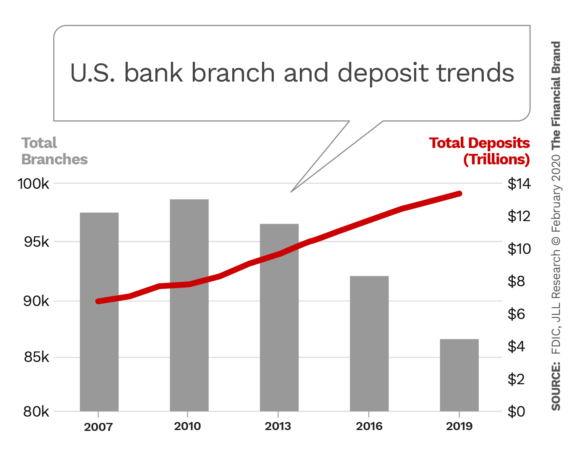

As of 2019 there were about 86,000 bank branches in the U.S., according to FDIC data analyzed by JLL Research. At the rate of decline over the most recent ten years — roughly 2% a year — mathematically it would take over a hundred years before there were zero bank branches in the U.S. And that does not include credit union branches, which numbered 21,337 as of June 2019, according to S&P Global.

Zero branches is not realistic, obviously, and the rate of closures may well accelerate if industry consolidation quickens due to a combination of economic, technological and demographic factors, which some observers expect. Still, nobody can predict with certainty what the number of financial institution branches will be in ten years, much less 25 or more. What can be said is that the recent past, combined with the current situation, paints a good picture of near-term branch trends.

Right now, the ongoing reduction in branches continues to be led by the largest institutions. At the same time, big banks are also selectively opening new branches to grow deposits and serve customers in a handful of targeted markets where they don’t have a physical presence. Small and midsize institutions are also opening new branches — far more of them, in fact than the large banks.

JLL Research, part of the national real estate firm JLL, predicts in its annual bank branch report that the 2% rate of net branch closures will continue. “We do not expect this pace to change materially over the next two years as the industry works to integrate physical branches with digital platforms and define how to best serve rapidly shifting customer expectations,” the report states.

The Long Tail of Big-Bank Mergers

Ongoing consolidation within the industry among large and mid-size financial institutions in particular is one reason for this prediction, according to Christian Beaudoin, Managing Director, Research and Strategy for JLL, and co-author of the report. For the top 25 U.S. banking institutions (from JPMorgan Chase down to Capital One) the rate of branch closures from 2018-19 was 3.7%, up from 3.1% in the previous 12-month period and well above the industry average of 1.9%. That amounts to a net decrease of 1,450 branches. A significant change in the economic or political environment that impacts bank mergers and acquisitions could alter the degree of branch shrinkage Beaudoin states.

Bank branch openings and closings 2018-2019

| New branches | Closed branches | Net change | Percent | |

|---|---|---|---|---|

| Top 10 banking institutions | 243 | -1,284 | -1,041 | -3.7% |

| Top 25 banking institutions | 327 | -1,777 | -1,450 | -3.7% |

| Total U.S. – remaining bank holding companies | 1,154 | -1,387 | -233 | -0.5% |

| Grand Total U.S. | 1,481 | -3,164 | -1,683 | -1.9% |

Source: FDIC, JLL Research

However, already completed mergers have long tails when it comes to branch optimization, notes Walter Bialas, Vice-President of Research at JLL, and the report’s other co-author. The 2019 merger of SunTrust and BB&T (rebranded as Truist), for example, will bring opportunity for those two large regional institutions to optimize their branch footprint, says Bialas. “The catch is, it takes a while to bring that about because of how long leases extend, along with owned facilities that have to be sold,” he explains. So the impact on branch numbers from such large mergers will be felt for some time.

As the table above shows, small and midsize banks added almost as many branches as they closed from 2018 to 2019. The situation for them is, in general, different from many of the largest institutions. Regional and community institutions are looking for ways to grow their balance sheets, Bialas states.

“Small and midsize institutions are much more nimble in being able to expand through branching.”

— Walter Bialas, JLL Research

“With smaller branch portfolios, it’s easier for them to see that they need a new branch in this market or another, which, for them, is a big change,” Bialas notes. “Small and midsize institutions are much more nimble as a rule in being able to take advantage of these opportunities to expansion through branching,” he explains.

That said, the largest banks are definitely seeking out new opportunities for a physical presence at the same time they continue optimizing their networks. Partly as a result of that, a handful of metropolitan areas have seen a net increase in the number of bank branches from 2018 to 2019, although overall most areas declined.

Read More:

- Without Branches, Banks and Credit Unions Say They Can’t Survive

- 4 Revealing Insights From Study of New Branches Opened By Big Banks

- 5 Reasons to Think Twice Before Closing Branches

The Financial Brand spoke with Beaudoin and Bialas to probe further into their report’s findings.

Could the ongoing branch decline slow or actually stop at some point?

Christian Beaudoin: In the current cycle — meaning over a five- or ten-year horizon — we’ll continue to see consolidation driving branch contraction. But beyond that, you never know. All cycles depend on how long your time frame is, right? So if you’re thinking far enough out, at some point we could see a need for additional branches depending on population growth and other factors.

There is also a steep decline in branch visits. Do you see any short-term change in that trend?

Beaudoin: I do not. If anything I see an acceleration of that trend as the huge Millennial and Gen Z generations now on the scene continue to impact banking.

Walter Bialas: Branch trends are a reflection of how the banking industry is struggling with rapidly changing customer expectations and behavior. It’s not as if institutions can say, “If we just do this one thing, we’ll solve this problem.” That’s why in the report we talk about how banking remains in the middle stages of this evolutionary process of digital transformation. It will be going on for a long while.

The report talks about ‘digitally focused’ branches. What do you mean by that?

Beaudoin: It’s a physical facility that allows consumers to complete their transactions or receive assistance or advisory services in the way that works best for them. Some consumers still prefer person-to-person interactions to get things done. Others prefer using interactive kiosks or other digital means that allow them to open an account or connect a new account with other accounts. Financial institutions are moving through an evolution right now of handling consumers’ needs along the entire range of full-service person-to-person at one end to fully automated at the other, with a whole spectrum of options in between.

Why would a consumer come to a physical location to do their banking digitally?

Beaudoin: They can perform some things digitally and may prefer that, but if they have a question — how to link a new checking account to their Ameritrade account, for example — it helps to have a person a few feet away to help you. At home on a mobile device, on the other hand, you may end up talking to someone at a call center on another continent.

“People like to do things digitally, but if they have a question, it helps to have a person a few feet away who can help.”

— Christian Beaudoin, JLL Research

Also, it’s a recognition that while digital solutions can perform many transactions and functions, they can’t perform them all. It’s like a self-checkout line at a store. About 80% of the time it works, but for the 20% when I change my mind on something I bought or my credit card doesn’t take, I still need a person to help.

Bialas: Also, for many bank branches small business customers are a significant groups of users. They frequently need checks cut or other things done that may not be easily handled digitally. So they still need a person to help.

What are the most important changes needed for branches to remain relevant?

Beaudoin: I see three things. First, obvious as it may seem, one of the most important success factors for any bank branch is still location. The facility has to be situated in the right location to attract the right talent and to serve the right customer base, based on demographic analysis, and other factors.

The best-designed branch won’t succeed if it’s in the wrong location.

Second, it’s vital for a branch in this era to have an efficient and flexible design to accommodate services across the human and technology spectrum.

Third is making sure that the employees working in your branches are trained to handle not only transactional services, but wealth management services, advisory services and sometimes even technology problem-solving.