Given all the words written about “the death of the branch,” the announcements in 2018 by JPMorgan Chase and Bank of America that they would each build 400 to 500 new branches over the next four-to-five years got a lot of attention. Many community banks and credit unions are still building branches, as well, even if it’s only one or two annually. What can they learn from the big bank’s efforts?

I analyzed the new branches opened by the top three banks in the last three years of official FDIC reporting (June 30, 2015-June 30, 2018). In a previous analysis, I found that about 60% fewer branches have been opened in the years since 2008, compared to pre-recession years, and that these newer branches are performing significantly better than those opened earlier in terms of deposit growth. The question is whether the new branches of the three U.S. megabanks are performing similarly.

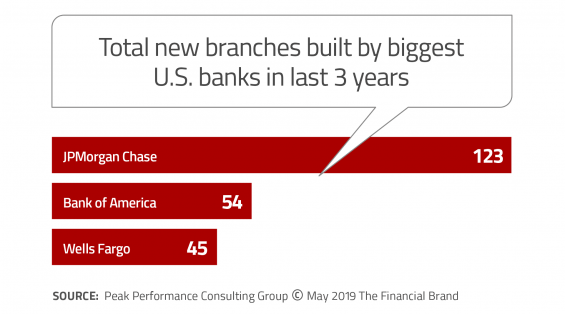

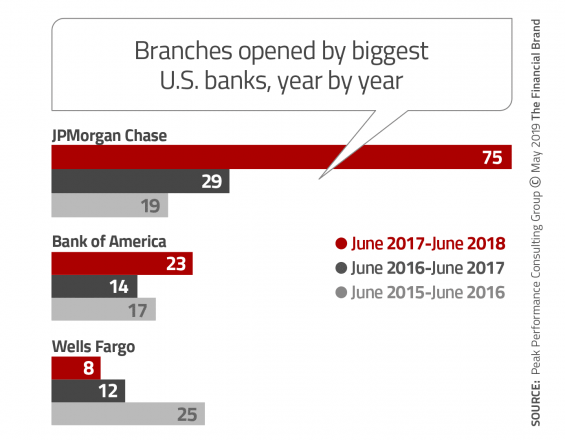

The recent announcements of building 80-100 new branches annually notwithstanding, the Big 3 have been building a more modest number of new branches in recent years. Chase leads the pack at an average of 40 annually, followed by BofA at 17, and Wells at about 15. These counts don’t include the fully automated and un-staffed locations such as BofA’s “Advanced Centers.” These new types of sites don’t meet the technical definitions of a branch and don’t require a branch charter.

Breaking down branch building into the last three reporting periods paints an interesting picture. Chase has seriously ramped up efforts, increasing from 19 to 75 new branches in the last reporting year, near the pace to meet their stated goal of 400 in five years (80 per year on average). BofA has been relatively steady, increasing from 17 to 23 new branches, but far below their stated target of 125 per year. Wells Fargo, perhaps not surprisingly due to their recent regulatory and reputational issues, is building fewer new branches, declining from 25 to only 8 in the last reporting period.

Where Are The Big 3 Building Branches?

Chase is building in the most markets (36) with half of its new builds in just six metropolitan areas (none in new markets). Surprisingly, Chase built 19 new branches in the New York City metro area alone, a place they already dominate. Two-thirds of their new branches are in top 20 markets (based on population).

Bank of America is more focused, building in only 19 markets with half concentrated in just four markets. Two of those four are new markets — Denver and Minneapolis. Fully 83% of BofA’s new builds are in top 20 markets.

Wells Fargo is building in 15 markets with half of its new branches in just three markets — two of them places where they already dominate: Los Angeles and San Francisco. Again, most (83%) are in top 20 markets.

The messages here are:

- Even if you want to expand into new markets, don’t ignore your core markets as you likely have opportunities to infill your network where your brand is already a known quantity.

- Bigger markets present greater opportunity, generally because the demand is more concentrated.

- The vast majority of these branches are traditional branches, with Wells opening a few supermarket branches.

How Well Are The Big-Bank Branches Gathering Deposits?

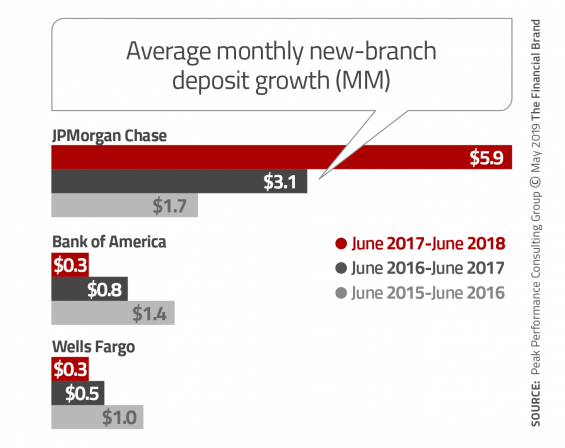

Most new traditional branches cost about $1 million to $3 million to build and $750,000 to $1 million annually to operate, with regional differences. Using $1 million in annual expense as an average, a new branch would need at least $29 million in deposits — assuming a fully loaded 3.5% spread (including fee income) — to generate positive cash flow in the third year of operation. That translates into a deposit growth rate of about $1 million per month. In my years of building new branches for Bank of America, that was the general goal we established as a minimum threshold.

Chase seems to have done a good job with each year’s portfolio of new branches exceeding that $1 million threshold. In fact, they have improved each year from $1.7 million to $5.9 million per month for recent branch openings, a truly outstanding figure.

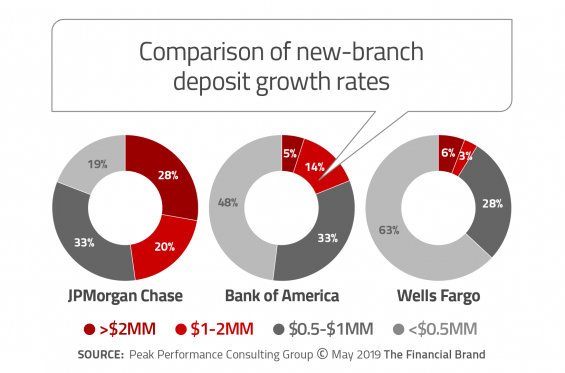

On the other hand, both Bank of America and Wells Fargo have seen their more recently opened branches struggling. (These figures exclude branches already exceeding $500 million in deposits, a standard approach in branch analysis meant to control for corporate deposits.) Even with this filter applied, Chase does have a high number of branches reaching $100 million or more in deposits in an unusually short time frame. Let’s look at those numbers through a different lens.

Nearly half of Chase’s new branches are averaging more than $1 million per month in deposit growth, in fact 30% are at twice that rate. Less than 20% of Bank of America’s new branches, by contrast, are averaging over $1 million per month, and Wells is not even 10%. I find these number surprising, but it shows how difficult it is to implement growth strategies through de novo branching even for the biggest banks in the country. We also need to keep in mind that a handful of these new branches are “corporate centers,” which benefited from transfers of large commercial deposits, so it is difficult to assess their true “retail” growth rates. Even so, Chase clearly is outperforming its two large rivals.

Read More: Top Branch Trends for Banks and Credit Unions

Which Big Bank Has Better Branch Locations?

I’ve had the opportunity to analyze more than 10,000 branches in my career, so I’ve seen lots of good and bad decisions about where to place branches. Beyond market characteristics, I’ve found that location setting and site placement have a huge impact on sales performance, and thus, deposit growth.

Location setting refers to the type of retail center where the branch is located, such as a grocer- or big-box anchored center (generally the best for retail branches), strip centers, and others. Downtown locations offer their own unique challenges and can range from great-to-poor, depending upon concentration of employment. I evaluated all the new branches from the three big banks and rated them from “A” to “D” based on the quality of the retail draw at each branch’s location. What I found is that the good performers are at much better locations.

Nearly 60% of good performers are at “A” locations, with Wells Fargo leading with just over two-thirds of its new branches at “A” locations. Chase, who has built the most new branches, has the lowest levels of top locations. In fact, Chase has built almost one in five of its new branches at “C” locations. That makes me wonder whether in their efforts to quickly ramp up branch building they are not being as patient as they should be.

Real estate is a long-term game. Often, banks and credit unions make 20-year commitments and then spend $2 million or more in capital to build the branch, so they need to be patient and make the right decision. Otherwise they could be saddled with an underperforming branch for many years.

Good Site Selection is Equally Important

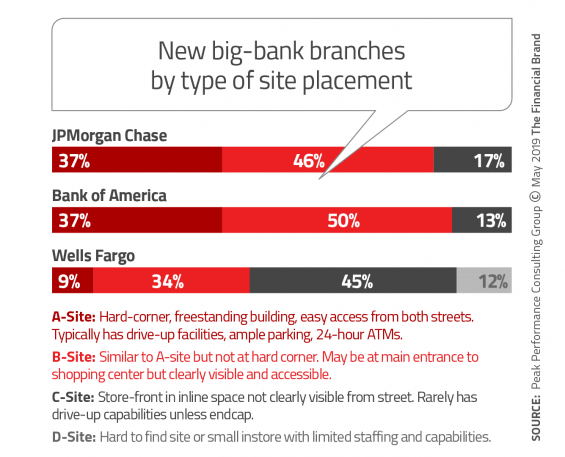

By “site,” I’m referring to the specific building a branch operates in. The main considerations are visibility and accessibility. However, services offered, building size, parking, and appearance all matter too. Again, I rated each of the new Chase, BofA and Wells Fargo branches on an “A” to “D” scale.

As with locations, the best branch performers in terms of deposits are also more likely to be good sites. Nearly one-third of Chase and BofA’s new branch sites are “A” sites — hard-corner, free-standing buildings with drive-up capabilities. And over 80% of these two banks’ new branch sites are either “A” or “B” sites, compared to only 40% for Wells. In my experience, the best performing branches are “A” or “B” sites at “A” locations.

Wells Fargo chose to open in-store or inline storefront branches in nearly 60% of its new branches, possibly sacrificing long-term financial success for lower initial costs. They chose mostly good locations but weak sites, which contributes to the weaker performance of their new branches.

4 Takeaways From Big-Bank Branch Analysis

As a result of this brief review, there are four things community banks and credit unions can learn about building new branches by studying the three biggest banks:

- As you expand, don’t forget to look for infill opportunities in your existing core markets.

- Larger, more densely populated markets generally present higher demand levels.

- Picking a good location requires patience. In many markets there are not a lot of new shopping centers being constructed.

- Picking a good, visible and accessible site is important as well. Remember, Wells Fargo chose good locations but weak sites. Both matter.

These four factors apply to your current branches, too, and might help to explain their performance. Perhaps you should ask yourself “How do my branches stack up against the biggest players?”