COVID-19, having accelerated the evolution of the branch system and digital banking, appears to be hastening acceptance and use of contactless payments, especially contactless cards. While a shift has clearly been occurring, at least one payments expert cautions that its magnitude must be considered carefully.

Early in the coronavirus crisis there was much fear that simply touching a surface like a card reader or POS terminal PIN pad that had been touched by an infected person could cause someone to catch the coronavirus. Much stock was put in an erroneous quote attributed to the World Health Organization, which quickly denied that it had stated that surfaces were a major risk.

Now it’s less certain how communicable the disease is from surface contact. But since those early days, out of an abundance of caution many consumers in the U.S. and elsewhere have been choosing to use contactless means of making payments.

This change has taken two forms. One is use of contactless cards or mobile wallets at the point of sale — neither require touching the payment terminal. The other is payment via online or mobile prepayment or even spoken over the phone, with the consumer picking up their purchase at the retailer’s store. (Contactless point of sale payments cost merchants the same fee as swipe or chip insertion payments, as they are all “card present” transactions. On the other hand, online, mobile and spoken transactions are considered “card not present” transactions and command a higher fee.)

Like much to do with COVID-19 and its economic ripple effects, the contactless trend has been something of a moving target. During the strictest phases of the widespread shutdowns of all but essential retail businesses, many purchases, when even possible, were by definition going to have to be through online means. Card-not-present transactions soared for card networks during this period, while card-present transactions plummeted, according to research by S&P Global Market Intelligence.

However, there is widespread consensus that, just as many Americans tried digital banking for the first time during the pandemic and liked it, many also tried contactless payments for the first time and will have strong interest in continuing the practice.

What Retailers Have Been Seeing and What They Expect Next

One of the strongest sets of numbers demonstrating the shift comes from a joint study of both retailers and consumers by the National Retail Federation and Forrester. Released in August 2020, the research found that use of contactless methods has increased significantly.

“While mobile payments and contactless cards have accounted for a minority of payments in the past, the pandemic has clearly driven consumers to change their behavior.”

— Leon Buck, National Retail Federation

“While mobile payments and contactless cards have accounted for a minority of payments in the past, the pandemic has clearly driven consumers to change their behavior and retailers to accelerate their adoption of the technology,” states Leon Buck, NRF’s Vice President for Government Relations, Banking and Financial Services.

Concerning retailers, the survey found:

- 67% accept some form of no-touch payment at point of sale.

- 58% accept contactless cards, up from 40% in 2019.

- 56% accept digital wallet payments, up from 44%.

- 69% have seen contactless payments rise since January 2020.

- Of those retailers that have activated contactless payments capability, 94% expect increases to continue.

One in five offering contactless payments say more that half of their in-store transactions use the technology.

Concerning consumers, the survey found:

- One in five have made a contactless payment for the first time during the pandemic.

- Of those consumers, 62% used mobile wallets and 56% used contactless cards.

- 57% said they would continue using contactless payments post-pandemic.

A study on contactless methods by Entrust Datacard found that 40% of consumers use some contactless method of payment at least three times a week and 34% at least once or twice a week. The same research found that sanitary concerns ranked highest among consumers choosing contactless means — 70% cited this, edging the 67% who cited transaction speed.

Visa’s “Back to Business Study” found some serious points for reflection for financial institutions that discount the contactless trend.

First, the research found that 78% of global consumers have adjusted the way they pay because of COVID-19 risks. “The shift to digital-first commerce and technologies like contactless payments has ushered in a new generation of consumer tendencies that will have a ripple effect on the global economy for years to come,” the report states.

Statistics in the report flesh this out:

- Nearly two thirds — 63% — of consumers globally would switch to a provider that installed contactless payment capability over an existing relationship. (This assumes that factors like price, selection and location are equal, the report suggests.)

- Over half of Americans — 54% — would switch. And almost three quarters of Millennials would do so.

- 48% of consumers say they won’t shop at stores that offer only payment methods that require contact with a cashier or a shared surface like a POS terminal.

- 62% of consumers have been using cash less during the pandemic out of concern that they could catch the virus from money.

- 12% have ditched cash completely.

Key Finding: Beyond preferring contactless payments, many consumers are cleaning their payment cards. 33% disinfect them and 22% wipe their cards on a shirt or cloth. In addition, 23% wear gloves while making payments.

Finally one out of three small businesses globally have either banned cash purchases outright or have accepted cash less in the wake of coronavirus.

Read More:

- Debit Cards Dominating Retail Payments, Fueled by P2P and eCommerce

- Banks and Credit Unions Must Take Digital IDs Seriously Now

- Financial Marketers Moving Mobile Ads to the Front Burner

Digital Boom Sets Up Favorable Environment for Contactless

All this takes place at the same time that Zelle, the banking industry’s P2P platform, reported a 63% increase in payment transaction volume year-over-year during the first six months of 2020. Zelle also saw a 43% increase in active usage in the same period (people who have sent a payment in the previous 90 days). Zelle’s operator, Early Warning Services, LLC, notes that many consumers used the service to reimburse neighbors for groceries picked up or to send money to friends and family during the pandemic.

“As economies open up, people will rely more on contactless pay tools, and I think it will create a lasting behavioral change.”

— Denise Leonhard, Venmo

During a roundtable discussion on Synchrony’s website, Denise Leonhard, Commercial Officer of Venmo, PayPal’s P2P service and Zelle’s rival, said that growth in usage had been dramatic, “even more than on Black Friday or Cyber Monday on certain days, which is traditionally the most active time of the year.”

Added Leonhard: “As economies open up, people will rely more on contactless pay tools, and I think it will create a lasting behavioral change.”

“Contactless debit will increase as the big banks put more contactless cards in the market and smaller financial institutions prioritize the investment,” predicts Mercator Advisory Group. The firm reports that Visa, which is the brand on nearly three-quarters of U.S. cards, already has 93 million contactless debit cards in the field in the U.S.

“Much of the customer behavior and loyalties formed in this period may persist well beyond the pandemic and may even become the new standard for customer behavior in the post-COVID period,” suggests S&P Global Market Intelligence.

A white paper from Harland Clarke notes that many consumers carrying first-generation chip cards are coming up for replacement cards. This is a good opportunity for them to be given “dual-interface” cards that accommodate both chip insertion and contactless transactions, the paper states.

According to Visa figures quoted by Mercator 80 of the top 100 U.S. merchants accept contactless cards. As a result, this means that more than three out of five card transactions take place where ability to accept contactless cards already exists.

Consultancy Offers a Contactless Reality Check

A balance to the enthusiasm over the surge of interest in contactless comes from Sarah Grotta, Director, Debit and Alternative Products Advisory Service at Mercator. In a blog, she notes that “one could come away with the impression that consumers in the U.S. are madly tapping and waving their cards to the exclusion of all other payment types, with the exception of the disenfranchised, of course, who are still using cash.”

Grotta, a payments veteran, suggests there’s a flaw in this reasoning.

“Much of the data shared comes from consumer survey data, which is very helpful in understanding trends and directions, but doesn’t pinpoint the number of transactions that have been completed contactless,” Grotta writes. She points out that while U.S. consumers had hung back, in other countries contactless was a preferred payment method pre-COVID.

Grotta also suggests that transaction data might not tell a “newsworthy type of story,” in that the increases seen are on small pre-COVID usage levels.

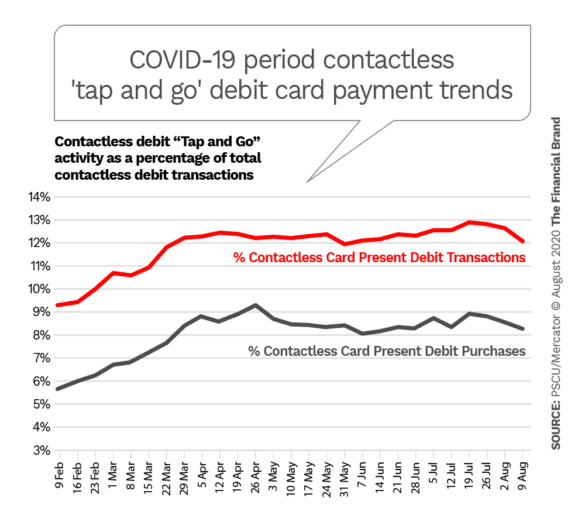

That said, in a detailed analysis Grotta evaluated openly reported transaction figures from PSCU, a CUSO serving credit unions across the country. In the charts below, she tracked consumer behavior over the COVID period among PSCU’s universe.

First, she tracked contactless card use in terms of transactions, the top line, and actual spending, the bottom line.

She points out that contactless was on a steeper growth curve prior to March 1. She says this likely reflects the fact that later transactions were occurring at nonessential retailers who have not always set up their terminals to take contactless payments. She believes as reopening continues they will get on board.

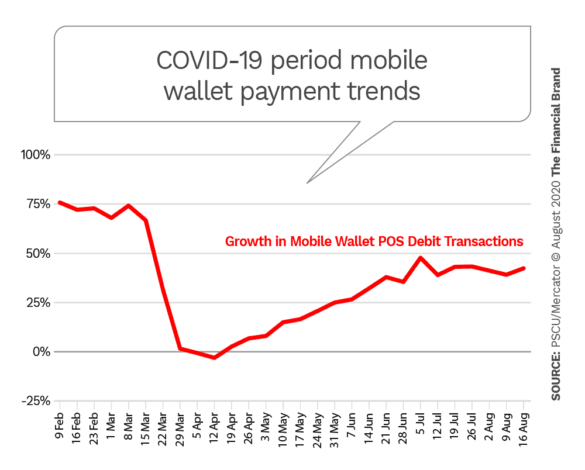

Second, Grotta tracked trends in the growth rate of mobile wallet transactions.

She points out that the growth in number of transactions, rather than purchases (actual dollar spending), is the more important number to follow.

“More transactions build a lasting payment habit, meaning that the user is more likely to use contactless at that location again and may try it at other stores,” she says. Consider this in light of the consumer preferences reported in the survey reviewed earlier.

Grotta’s verdict: “While these growth numbers do not necessarily provide a sizzling headline, this is good growth as it represents a change in consumer behavior, which often takes years to accomplish. … As financial institutions continue to replace expired cards with contactless capable plastic, as they promote mobile wallet use, and as more financial institutions initiate projects to launch contactless cards, the growth will be further fueled.”