For a product that was introduced before any Millennials were born — much less members of Gen Z — the debit card continues to show it has as many lives as the proverbial cat, adapting surprisingly well to an increasingly digital world.

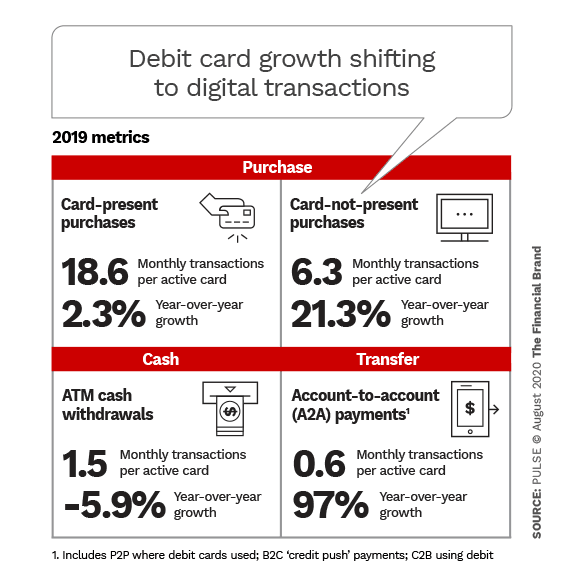

Debit card transactions grew 6.5% in 2019, a healthy number in itself. However, the vast majority of that growth came from card-not-present (CNP) use. That, in turn, was driven by e-commerce transactions but also, notably, by rapid growth in a variety of account-to-account (A2A) transactions. These include person-to-person transactions from Venmo and Square Cash and other P2P apps, as well as payments made to gig economy workers such as Uber drivers.

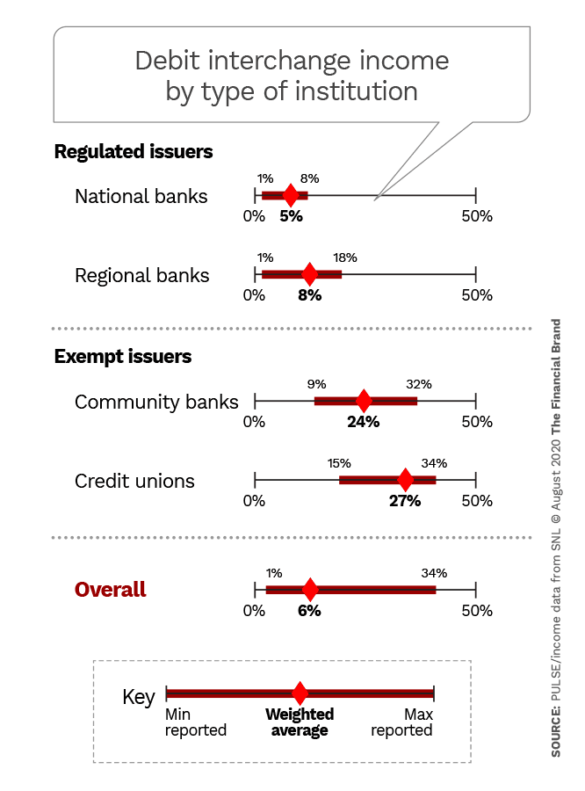

In many ways the debit card is not only surviving, but benefiting from the rising use of digital payments including mobile wallets. Debit cards are increasingly the payment utility “behind the curtain,” so to speak — the card-on-file quietly racking up interchange income for issuers. In fact, according to the 2020 PULSE Debit Issuer Study, debit interchange accounts for about 25% of noninterest income for community financial institutions below the $10 billion exemption cap of Federal Reserve’s Regulation II, which limits card swipe fees.

“For a mature product seeing 6.5% year-over-year growth — as well as all the different ways of utilizing the card — really does speak to the durability of debit as a payment type,” observes Steve Sievert, EVP of Marketing and Brand Management for PULSE. It also speaks to the ability of the banking industry to innovate to find different use cases, he adds.

The annual debit study surveyed 55 issuing institutions that manage 157 million debit cards, representing 42% of U.S. debit card transactions, according to the survey report. Sievert points out that the survey is not a PULSE member survey. Members of multiple networks participated. 31 of the issuers taking part were national or regional banks above the $10 billion asset threshold with the other 24 being exempt community banks and credit unions.

Payment Trends in Play Before COVID

The research was conducted during February and March and is based on yearend 2019 and full-year 2019 data, compared to 2018. Although some people may dismiss any pre-COVID study as irrelevant in vastly changed circumstances, the PULSE survey data could present a better picture of digital payment and banking trends than data gathered during the pandemic period when abnormal conditions obscure the underlying trends.

A demonstration of this comes from the study report itself. Oliver Wyman, which conducted the research for PULSE, included a page summarizing the early impact on debit card transaction volume from the coronavirus. The resulting line graph looks like a Six Flags roller coaster.

A major transaction surge in mid March was followed by a nearly 30% falloff in transactions into early April and then a sharp uptick in late April as a result of stimulus payments reaching consumers.

The 2020 debit survey shows what was happening before the roller coaster ride began.

Read More:

- Why Real-Time Payments Are Quickly Becoming Table Stakes

- Small Banks Must Fight Harder to Stay Relevant in Payments Space

Debit Growth Comes from Nontraditional Usage

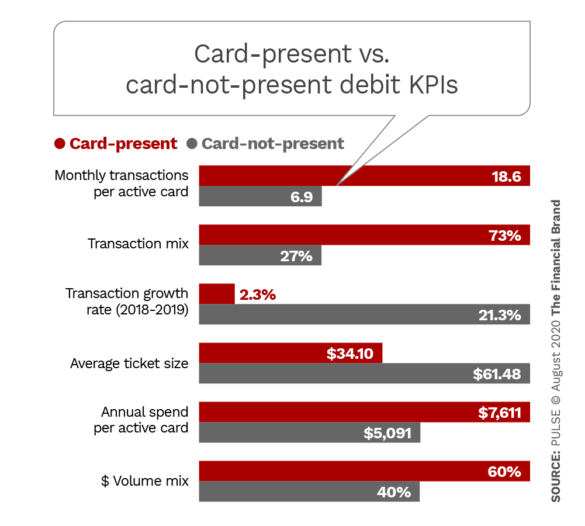

Almost three quarters (73%) of debit transactions in 2019 were still of the card-present variety — primarily in-store shopping using the physical debit card. That traditional payment usage grew, but at lower rate (2.3% year-over-year) than online card use and A2A payments, which grew 21.3% and 9% respectively. To be sure, A2A transactions grew from a much lower level. One in four debit card issuers that experienced overall transaction growth had negative or flat card-present growth, the data show. And that was before so many stores had to shutter during COVID.

Further, online card use had a higher ticket size and higher transaction growth, and now accounts for 40% of total debit card dollar volume.

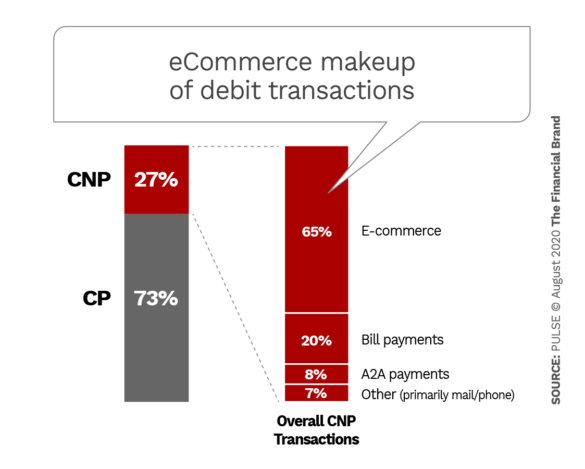

The PULSE survey broke down card-not-present transactions in detail. As the chart below shows, nearly two-thirds of CNP volume comes from e-commerce, a figure that most likely will jump in next year’s survey thanks to the ongoing concerns about the safety of in-person shopping. The rest of CNP was comprised of bill payments, A2A and mail and phone payments.

Read More: Four Trends That Will Finally Make Cashless a Reality

Wallets, P2P and the On-Demand Economy

While comprising only 8% of card-not-present debit transactions, A2A payments received a lot of attention in the study because these emerging transactions nearly doubled in 2019 (up 97%) and accounted for 40% of total debit card growth. That growth reflects the expanding range of ways in which funds are moved and disbursed between individuals and businesses.

The PULSE survey lists two main categories of these newer type of debit transactions:

- Account Funding Transactions — consumers increasingly fund non-bank payment wallets such as PayPal, Venmo and Zelle with debit cards.

- Original Credit Transactions — increased disbursements of money “pushed” to a consumer’s debit card, including commissions paid to gig-economy workers such as Uber, Lyft and DoorDash drivers, as well as for insurance payouts.

“One of the key factors driving debit growth is this notion of consumers uploading their debit card to pay for recurring transactions such as Netflix or Spotify.”

— Steve Sievert, PULSE

“One of the key factors driving CNP growth in debit is this notion of consumers uploading their debit card to pay for recurring transactions such as Netflix or Spotify, or a food delivery aggregator,” Steve Sievert tells The Financial Brand. He refers to this trend as the “sublimation of payments” where there isn’t the need to regularly utilize the card or access it in a traditional way. “The payment just becomes part of the overall experience.”

Consumers, of course, can choose to add a credit or debit card to a subscription service. In the past, credit may have had the edge given its more generous rewards programs, but Sievert believes that in the current more difficult economic circumstances consumers prefer to use debit transactions over credit so they don’t incur debt and can better manage their finances.

In addition, the PULSE executive states that even before the pandemic, consumers had been minimizing their use of cash and have likely embraced that practice even more since COVID arrived. “The ability to digitally exchange money in a way that makes it very seamless and convenient is likely to be a continued growth area,” Sievert states.

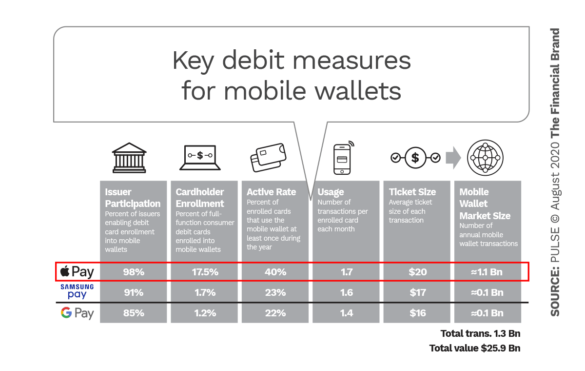

Dramatic Growth of Apple Pay Among Wallets

Mobile wallets haven’t had a lot of good news considering the fanfare with which they were initially greeted. Apple Pay, however, had a banner year in 2019, accounting for 85% of the 1.3 billion mobile wallet debit transactions, and doubling its previous year’s total.

“Apple Pay is really beginning to outperform the other mobile wallets in a major way,” Sievert declares. “Year-over-year growth with Apple Pay that we saw in the study far exceeds both Google and Samsung Pay.”

Overall, PULSE reports that mobile wallet payments using debit cards increased by 94% year over year. Wallets still remain a very small part of overall debit transactions, however — just 1.3 billion out of 77.4 billion. The average mobile wallet ticket size is 50% of the typical debit point-of-sale transaction, suggesting that paying by wallet is replacing small-dollar cash transactions. Although not entirely.

Sievert notes that one of the factors behind Apple Pay’s 2019 success was that it began routing iTunes purchases through Apple Pay. Another is that Apple Pay has benefited from additional merchant penetration of NFC-enabled (contactless) terminals, because of Apple’s higher cardholder enrollment rate.