To many, the idea of prepaid financial services still conjures up images of single-use gift cards given as birthday presents or perhaps a financial tool used by the unbanked.

Banks and credit unions, however, should start tapping into the potential to use prepaid technology in order to innovate digitally and quickly bring new products to market.

“Prepaid today is more versatile and prevalent than ever before,” says Francisco Alvarez-Evangelista, an advisor in the retail banking and payments practice at Aite-Novarica group in an interview with The Financial Brand. “Yet it is often this unassuming player that gets little attention for its role in today’s top trends.”

Prepaid is still largely looked at as a high risk, low reward market by many traditional financial institutions, says Alvarez-Evangelista, yet it plays a large role in how many fintechs and digital challenger banks have rolled out new products.

Hidden in Plain Sight:

The rapid innovation in payments in general has obscured the fact that prepaid card technology has seen significant changes.

“Prepaid cards are an important payment mechanism that have seen renewed interest in recent years, as well as several developments in terms of capabilities,” observes Juniper Research.

Fintechs Use Prepaid to Jumpstart BNPL Products

Fintechs have been leveraging prepaid technologies and existing prepaid payment rails for several years now in order to innovate and speed new products to market quickly, says Alvarez-Evangelista.

One example is buy now, pay later. Many people don’t realize that today most BNPL transactions are handled on the back end by prepaid program managers and utilize existing prepaid payment rails to facilitate the settlement between the BNPL company and the merchant, Alvarez-Evangelista notes. Major firms such as Klarna, Affirm and others rely on prepaid infrastructure to power their platforms.

“This enables the merchant to get paid immediately and the BNPL company to get some level of interchange fee from the processor,” he adds.

Overall, it is a “far more efficient way” to conduct such transactions, as opposed to using other settlement processes on the back end, such as sending an ACH, he states. Everything is settled immediately.

Innovation Tool:

Fintechs realized that existing prepaid infrastructure was a more efficient approach to settling BNPL transactions.

Another way fintechs are using prepaid technology and infrastructure to innovate is in the creation of new banking products. When digital challenger banks such as Chime and Varo first offered “checking accounts” these were in fact not true checking accounts, but used prepaid payments rails, and the associated cards issued to customer were prepaid cards, Alvarez-Evangelista points out.

“It was the quickest way to go to market,” he says. (Chime and Varo, he adds, now both offer true checking accounts with associated debit cards.)

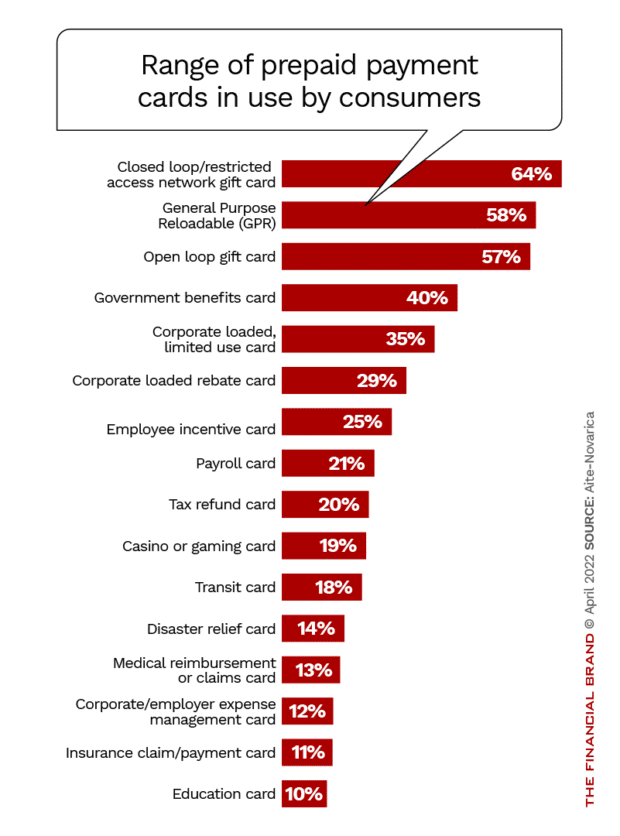

Use of prepaid products is also becoming increasingly popular among consumers. Aite-Novarica research from Q2 2021 catalogued many different types of prepaid products used by consumers, and the frequency with which they are used.

“We are seeing a transition of the prepaid card from something that would be on a J-hook at a local retailer, to something that is being reimagined, especially by digital challenger banks,” says Alvarez-Evangelista.

Read More:

- 8 Fintech Trends Changing Banking Forever

- Financial Institutions Must Address ‘Buy Now, Pay Later’ Problem Now

- Six Retail Banking Technology Trends for 2022

How Banks Can Jump on the Prepaid Train

Many financial institutions for the decade after the Great Recession looked at the prepaid space as a hassle, with limited revenue streams combined with new regulations designed to protect consumers. In recent years, however, those financial institutions and their partners who are issuing prepaid today are far more mature in their understanding of the regulatory environment that exists, with more industry and staffing resources to manage those expectations as well, Alvarez-Evangelista observes. Thus, they have no excuse not to tap the expanded prepaid potential.

Banks and credit unions can look to how fintechs have utilize prepaid technology to innovate and do the same themselves.

Opportunity knocks:

Three big use cases in banking facilitated by prepaid cards: virtual cards, digital wallets and early wage access.

One area for prepaid expansion is in business banking. Banks can use prepaid payment rails to help a treasury client to conduct payments and facilitate accounts payable processes using virtual prepaid cards, Alvarez-Evangelista states. This eliminates paperwork and manual processes greatly for both the business and the bank.

Juniper’s research also touts the benefit of using prepaid technology to issue virtual cards.

“Virtual cards have vast potential within the prepaid cards space,” the firm states. “To start with, they can lower costs. By offering a virtual [card] with no physical option, issuance costs can be lower. This will be useful across prepaid card use cases where scale is important, such as bulk disbursement of government benefits for example, or in a corporate setting.”

Prepaid cards can also be implemented in digital wallets, Juniper noted.

“By offering digital issuance via a digital wallet and top-ups in this way too, potential theft is no longer an issue,” Juniper maintains. “Indeed, this reduces the barriers to entry and significantly decreases the costs of prepaid issuance and management.”

Prepaid technology can also be used by banks to enable early wage access services to customers, Alvarez-Evangelista states. Such services, offered by fintechs like Chime and others, have proven to be popular with a growing segment of consumers.

“Prepaid is not just general-purpose reloadable card or gift cards anymore,” says Alvarez-Evangelista. “It can be used for literally almost anything else.”