Building a digital payment solution using a bank membership model, Zelle is the newest in a series of simple, free and ubiquitous digital payment options that leverage a mobile app, replacing cash, checks, or cards, within a network of friends and acquaintances. Joining more established person-to-person (P2P) payment options such as Venmo, PayPal, Square and PopMoney, Zelle is built atop the infrastructure of clearXchange, with a goal of becoming the industry’s first unified consumer P2P brand.

Formally introduced in June, Zelle will eventually provide more than 86-million U.S. mobile banking consumers with the ability to send and receive money through their mobile banking application (no additional app will be required). Similar to other competitors, Zelle allows funds to be sent from one bank account to another in minutes, using only a recipient’s email address or mobile number.

“Send Money with Zelle” is conveniently available within the mobile banking apps of Zelle Network℠ participants. With no additional app to download, Zelle is intended to make digital payments a fast, safe and easy alternative to checks and cash.

At introduction, more than 30 financial institutions were announced as partners, including Bank of America, Citibank, JPMorgan Chase and Wells Fargo. In addition to working directly with financial institutions, Early Warning has established strategic partnerships with some of the leading payment processors, including CO-OP Financial Services, FIS, Fiserv, and Jack Henry and Associates. These relationships will expand the network and marketing power through community banks and credit unions, with the intention of having a single P2P platform for all traditional financial institutions.

A stand-alone Zelle app will be released this year for consumers of non-Zelle Network banks and credit unions. Until then, those outside the network can collect payments through Zelle by manually filling in their banking information and linking their accounts.

P2P Goes Mainstream While Mobile Payments Stall

There is no financial services activity that is growing as fast as P2P mobile payments, with awareness and use expected to skyrocket for the next several years. According to the latest mobile banking and payments forecast from eMarketer, 63.5 million US adults will use a P2P payment app at least once a month in 2017, equating to nearly one-third (32.6%) of smartphone users. In addition, the value of US mobile P2P payments will grow 55.0% this year to $120.38 billion, doubling by 2021.

“The consumer P2P market is experiencing rapid growth and financial institutions have a critical role to play,” said Michael Moeser, Director of Payments, Javelin Strategy & Research. “There is a market opportunity to offer a secure and trusted experience, as well as have greater P2P availability in financial institutions’ digital banking, mobile wallets and voice-driven P2P services.”

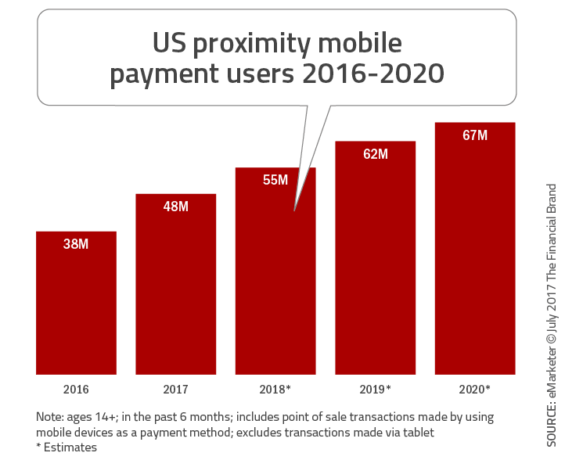

Meanwhile, mobile payment apps like Apple Pay and Google Wallet are being adopted in smaller numbers in the US, according to eMarketer. This year, the total US proximity mobile payment transaction value will grow 78.1% to $49.29 billion, with 48.1 million Americans ages 14 and older using a mobile payment app at the point of sale at least once in the past 6 months. While that’s nearly a quarter (23.0%) of smartphone users, the figure will grow only slightly to 30.8% by 2021.

![]()

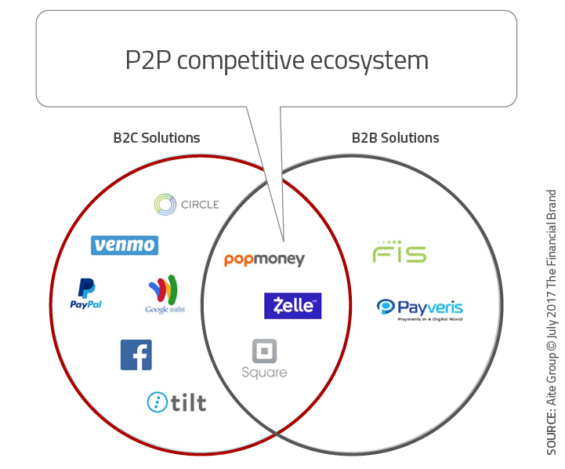

Zelle Entering a Crowded Market

The fact that P2P payments have become so popular, so quickly, is both Zelle’s biggest opportunity and its greatest threat. To become accepted as a mobile P2P payment option, Zelle organizations need to convince customers who already are fans of Venmo, Square Cash, Apple Pay and PopMoney to change established habits. This will require a significant awareness and branding advertising campaign, made more difficult since not all banks and credit unions will support the network initially.

There is still a lot of room for growth, however. One of the most prominent P2P competitors, Venmo (owned by PayPal), handled $17.6 billion payments in 2016, with close to $7 billion in payments in the first quarter of 2017. In comparison, the banks in Zelle’s network collectively processed $55 billion in P2P transactions last year, according to Early Warning.

![]()

While Zelle will not be a social media sharing solution with emojis like Venmo, it will provide a simple interface with immediate access to funds. According to Zelle, banks will be able to set their own user fees, but it is anticipated that no early participant will charge a fee. Finally, by being able to complete all P2P transactions within an institution’s mobile banking app, customers will avoid giving their banking info and passwords to a third party, helping to avoid concerns around privacy and security.

Can a Legacy Banking Product Succeed?

It is clear that Zelle has been introduced due to the pressure (and success) of fintech firms that have had massive success with P2P payments. While late to the game, the traditional banking industry does not want to be left behind in the competition for mobile banking, payments, digital lending, etc. But will the benefits of developing a strong P2P solution be short-lived?

The success of Zelle will be determined by the scope of the product penetration within the industry and the success of coordinated marketing and development efforts. If the majority of the organizations work independently on how the service gets promoted, the potential of Zelle will not be realized. The same is true with the development of Zelle 2.0, 3.0, etc. Future growth of the product depends on fintech-style innovation.

For instance, will Zelle allow the selection of payees using the address book already in a consumer’s mobile device? In addition, will the establishment of a new Zelle account for a consumer that is not yet supported by their primary financial institution be made simpler?

Finally, will Zelle support POS payments the way that PayPal, Square Cash, Google Wallet and others do? Venmo, Square and Apple have all added new P2P features that give consumers in-store payment capabilities, including a physical debit card. Will the banking industry be comfortable doing the same?

Why Should I Care?

The growing popularity of mobile P2P payments and increased spending power from digital-first consumers is causing the mobile P2P industry to skyrocket. While not a standalone money-maker as a product, not offering a strong P2P payment service could potentially result in attrition of an organization’s most profitable customers.

In addition, the coming 12-18 months may present an unprecedented opportunity for smaller and mid-market organizations to ‘ride the coattails’ of a much larger marketing initiative to promote Zelle. Learning from the introduction of Apple Pay, it is believed that there will significant industry support for Zelle.

Finally, organizations need to ask themselves if they can afford to sit on the sideline? The importance of becoming a bank that supports the digital consumer can’t be overestimated. Not just from a customer service perspective, but from a cost perspective. The investment required to provide P2P mobile payment solutions now is much less than the cost of playing catch up later.