Thinking that Apple Savings is simply a bid for Goldman Sachs to raise deposits is like thinking that iPhones are simply neat devices for making phone calls via a wireless carrier.

Apple launched its high-yield savings account on April 17, following through on its October 2022 announcement that its Apple Card program would be adding one. With many banking institutions focusing harder on deposit gathering and retention than they have in years, there might be an inclination to think of this move only in relation to funding. But there is more to consider.

How does Apple Savings measure up solely as a deposit-gathering move? And what is the bigger picture?

Apple Savings as Deposit Competition

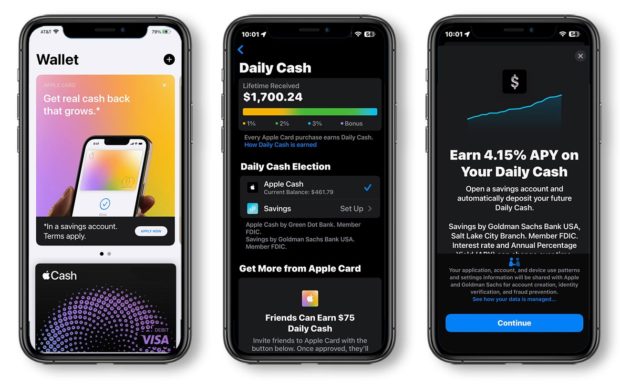

The initial annual percentage yield on Apple Savings is an attention-getting 4.15%, which the tech giant brags is more than 10 times the national average as computed by the Federal Deposit Insurance Corp.

As a savings account, this Apple product offers consumers greater liquidity than restrictive options like certificates of deposit, which have fixed terms and early withdrawal penalties. The tradeoff is that there is no assurance on how long that rate will be paid.

The deposits are held by Apple’s banking partner, Goldman Sachs, so are covered by the FDIC up to the usual amount.

The consumer response will vary widely based on age and other factors, predicts Ken Tumin, senior industry analyst at LendingTree and founder of its DepositAccounts.com site. Tumin says many of the people using his website are serious savers with a great deal of money that they need to squeeze the best return from. They deliberate over mere basis points before making a move, because the amount of money involved translates into a notable difference in their returns dollarwise.

Tumin says his read is that people are underwhelmed by Apple’s initial offer. He says many of them have accounts with Marcus, the online banking unit that Goldman Sachs operates as a way to gather retail deposits. Apple’s rate is higher than the 3.9% APY Marcus is offering on its high-yield savings account.

But that’s not the only rate available. For example, members of AARP could obtain a 4% rate from Goldman Sachs on that same account. Though that’s still lower than Apple’s rate, you don’t need an iPhone, the Apple Pay digital wallet or an Apple Card to get it.

All of those are required to access Apple Savings, and Tumin points out that many of his readers are senior citizens who don’t have smart phones.

Another drawback in his view is that the Apple Savings agreement, in its fine print, limits the account to a $250,000 balance. He says many of the rate shoppers using his site have more than that amount to place.

There are other providers of high-yield savings accounts that pay more than Apple too. Citizens Bank pays 4.25% for online high-yield savings, for example. Upgrade, a fintech that has Cross River Bank as its partner, pays 4.56%. Others offering even higher rates as of mid-April include BMO, Customers Bank, CIT Bank and Western Alliance Bank.

Read More:

- Understanding the Retail Bank that Apple Has Quietly Built

- Deposit Stability Matters More Than Low-Cost Money Now

- Deposit Competition Is On, But Should CDs Still Be the Go-To?

Card and Deposit Relationships Rarely Get Integrated Like Apple Is Doing

What surprises Tumin is that most online banks make little effort to link their online deposit offerings to their credit card programs. “You would think they would want to generate more savings through their credit card customers,” Tumin says.

Apple Saving's Role:

A key point about Apple Savings sets it apart from an ordinary savings account. It interlocks with the rest of Apple's banking and payment products.

One of the features of the Apple Card is Daily Cash, a variation on cash back rewards. This is paid daily, as the name implies, and can now be accumulated in two places. It can go into the Apple Cash account that the tech company offers through a partnership with Green Dot. The other, new destination is the Apple Savings account. Both options reside inside the Apple Wallet.

The savings account pays 4.15% interest on the Daily Cash that builds up there, as well as any additional funds deposited.

Just to keep our Apples in order: the Apple Pay digital wallet is the Apple way to make purchases with an iPhone in stores, in apps and online. Apple Wallet is another kind of digital wallet on the iPhone where consumers can store information about their cards, including Apple Card, access Apple Pay, and store other types of tickets and credentials. The cards stored in Apple Wallet can be used to buy things via Apple Pay.

Apple is open about its intention to continue adding even more banking products around the Apple Card and Apple Pay.

How big is the world of Apple financial products?

• Apple shares precious few details about the Apple Card, but Crone Consulting estimates the number of active Apple Card accounts at between 7 million and 12 million. (All of these are issued by Goldman Sachs.)• The consulting firm also estimates the Apple Pay mobile wallet has between 550 million and 610 million active users worldwide.

Read More:

- How the ‘Paze’ Digital Wallet Aims to Win Over Merchants and Consumers

- Digital Wallets Could Cost Banks Billions in Lost Payments Income

Sometimes It Quacks Like a Bank (Yet It Isn’t One)

As noted in The Financial Brand article “What the Apple Card High-Yield Savings Account is Really About,” you can’t assess the tech company’s offerings individually, the way you might with a traditional bank. They have to be seen as part of an ongoing effort to build a financial ecosystem for Apple users.

Still, debate continues over precisely what Apple is up to in the long term. After the Apple Savings launch, fintech consultant Bryan Claggett said in a LinkedIn post: “For the record, you can do better than 4.15% APY on cash. And providers like Betterment have better #UX and more financial product options. I’m not saying Apple and Goldman aren’t doing something cool (they are). But it’s not ‘transformational’ and won’t change banking.”

Ron Shevlin, the chief research officer at Cornerstone Advisors, responded: “I don’t think it’s supposed to be ‘transformational.’ I think it’s designed to drive more utilization of Apple Pay and Apple Card. And to make Apple more money. I don’t get the sense they care that much about ‘transformation’ anymore.”

Apple itself refrained from using words like “transformational” or “innovative,” instead describing the savings account as a practical add-on offering. “Our goal is to build tools that help users lead healthier financial lives, and building Savings into Apple Card in Wallet enables them to spend, send and save Daily Cash directly and seamlessly — all from one place,” Jennifer Bailey, vice president of Apple Pay and Apple Wallet, said in a company statement.

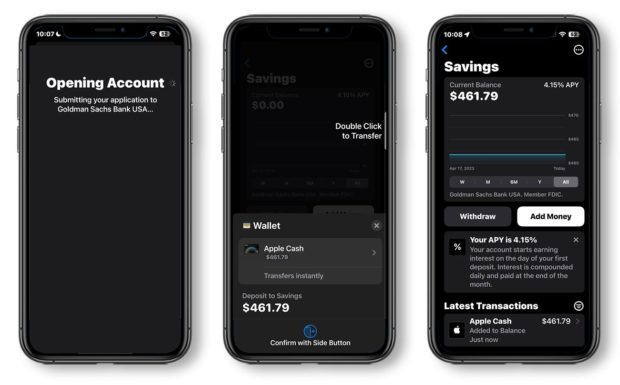

The banking options in Apple’s ecosystem are interconnected. To open an Apple Savings account, consumers need to have an iPhone and activate the Apple Card and the Apple Cash account in the Apple Wallet.

“That’s two hoops you have to go through, which tells me that they are purposefully doing this,” says payments consultant Richard Crone, who opened his own Apple Savings account the day it was announced, in part for what he considers an attractive rate. He points out that there are no fees on the savings account either.

But “this looks, acts and smells like a checking account,” given how accountholders can move funds through the Apple ecosystem on their phone, Crone says.

Apple Card holders can open an Apple Savings account right on their phones. Payments consultant Richard Crone says it took him under a minute. (Certain sections have been blocked for the sake of customer privacy.)

Apple Card holders encompass all generations, from Gen Zers to Baby Boomers, he says, but on the whole they are better educated, younger and more affluent.

The deposit growth they could generate is a plus for Apple and Goldman, in Crone’s view. And it helps that Apple “primes the pump” with the Daily Cash awards, he adds.

A Key Benefit for Apple: Consumer Data

The competitive threat to banks and credit unions lies not so much in the deposit account right now, but in a key operating aspect of the Apple Card relationship. Consumers with cards must provide their checking account number to Apple so it is pre-established where the money to pay the card bills will be coming from.

That information and the personal data entered to open the Apple Card account are powerful, because this fulfills know-your-customer requirements for any other product the consumer might use in the future within Apple’s growing financial ecosystem.

“That’s the strategy here, leveraging that data to open the account,” says Crone. He was able to open his Apple Savings account in “less than a minute.”

The pre-acquired data makes it simple and painless to expand what is becoming a cash management account relationship, according to Crone. (Another new offering, Apple Pay Later, will stay on the tech company’s own books, rather than get done through a bank partner. Apple Pay Later runs on technology from Mastercard Installments, the card company’s buy now, pay later operation.)

Read More:

- Digital Wallets Will Dominate Global Ecommerce Payments by 2025

- How One Community Bank Is Hanging On to Deposits as Rates Rise

What Would an Apple ‘Home Run’ Look Like?

Apple continues to show patience, slowly rolling out banking products and contentedly adopting what others have pioneered, Crone notes. The company does infuse high-tech touches designed to delight iPhone users. And this ties people into the Apple world more deeply and fosters an inertia that the banking industry, long a beneficiary of inertia, can appreciate.

Its strategy also generates some admiration. “Credit to debit to savings doesn’t exist anywhere else in this form,” Crone says.

Using a baseball analogy, he suggests that Apple has advanced to second base. He believes the ultimate “home run” would be a “pay by bank” network that would enable Apple to create payment rails independent of Mastercard, Visa, American Express and Discover.

When that happens, Apple will have become a superapp, he says. “You’re seeing a march towards being a superapp,” says Crone. “They are coming into the front door and going into every room in the house.”

What could the next move be? Crone suggests that, with all the consumer data it is compiling, Apple could become an agent for auto loans, moving into yet another key consumer credit activity for banks and credit unions.