With a world that is becoming more complex, today’s consumer is seeking organizations that can simplify their lives in a manner that is both personalized and seamless. The fewer steps it takes to achieve any objective, the better. The consumer also is growing increasingly aware of what is possible with modern technology, and they are moving established relationships to those organizations that can provide the best overall experiences.

Over the past several decades, traditional financial services providers have made very few changes to the products and services they offer or the manner in which they deliver them. Despite the introduction of credit cards, ATMs, telephone banking, online banking and mobile technologies, most banking innovation has been incremental in nature … usually focused on reducing the cost of delivery as opposed to improving the customer experience.

Most banks and credit unions have been unable to deliver a seamless consumer experience due to the continued presence of product and data silos, decades-old infrastructure, and a risk-averse culture that produces only incremental innovation. This has created an open door for startups and established non-financial competitors that can leverage data, modern technology and an agile mindset to deliver enhanced experiences.

“Improving the customer experience of an obsolete product line is like installing an escalator on a horse buggy,” states Ron Shevlin, Director of Research at Cornerstone Advisors and weekly contributor to Forbes. He continues, “Sure, it provides added convenience, but is it the best use of investment dollars? Today, consumers are accessorizing their traditional accounts with digital innovations from non-traditional players, including new savings tools, on-demand borrowing solutions, bill analysis tools, dispute resolution services and more.”

Beyond accessorizing existing accounts, an increasing number of consumers are ditching their legacy banking relationships altogether. As some of the larger fintech organizations expand their product offerings and build consumer trust, more disintermediation away from traditional financial organizations will occur.

Read More: 4 Myths Preventing More Fintech+Banking Partnerships

Experience Gap Widening Between Legacy Banks and Fintech Firms

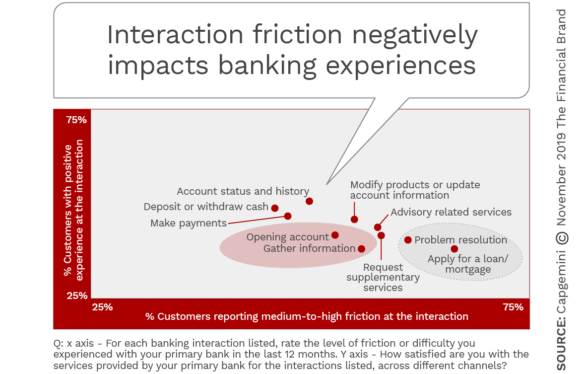

The way the majority of traditional financial institutions treat consumers and the experience they receive from fintech firms and big tech organizations underscores the differing approaches each side takes. The higher interaction friction, less intuitive design, lack of omnichannel solutions and poor integration with outside players negatively impacts user satisfaction metrics at legacy organizations, according to Capgemini’s Voice of the Customer 2019 survey of more than 8,000 consumers across 20 countries. The experience gap is the biggest with the more complex or high-involvement areas, such as applying for a loan/mortgage or problem resolution.

A bigger issue may be that fintech firms and challenger banks are providing lower friction as well as a more positive experience in the initial stages of the banking relationship, such as during account opening and when gathering initial information. This is why so many mid-sized and smaller organizations are generating fewer new accounts from digital consumers – there are fully digital options where no branch interaction is needed.

To effectively compete, banks and credit unions must provide seamless solutions with intuitive design that integrates into a consumer’s daily life. This is made more difficult because of product silos, decades old infrastructure and traditional mindsets. A viable option is to collaborate with the fintech and big tech organizations that have already built solutions that consumers are moving to.

“In an era of rising consumer expectations, banks are challenged to offer their customers a consistent engaging experience across all channels – branch, web and mobile – and evolve from the Open Banking approach towards an Open X mindset, where banks and new non-traditional players join forces to deliver banking services that integrate with digital experiences,” said Anirban Bose, CEO of Capgemini’s Financial Services Strategic Business Unit and Group Executive Board member. “Banks that identify their top capabilities and then seek partnerships with fintechs and other business sectors to enhance their offerings in other areas will be the most successful.”

Fintech: Threat or Collaboration Partner?

Banks, credit unions, non-traditional financial services providers, government agencies and big tech firms continue to debate what the banking ecosystem of the future will look like. Most believe that some sort of partnerships or collaborations will be needed to move forward successfully. The question is, which organizations will combine thought leadership and distribution capabilities to deliver next-generation solutions that will make the daily lives of consumers better?

More than ever, many traditional financial institutions believe fintech startups could be collaboration partners, short-cutting innovation efforts and providing enhanced digital solutions. But is the desire to partner coming too late? Evidence indicates that the strength of fintech firms and challenger banks may be greater than ever, providing some firms confidence that they can “go it alone.” For instance:

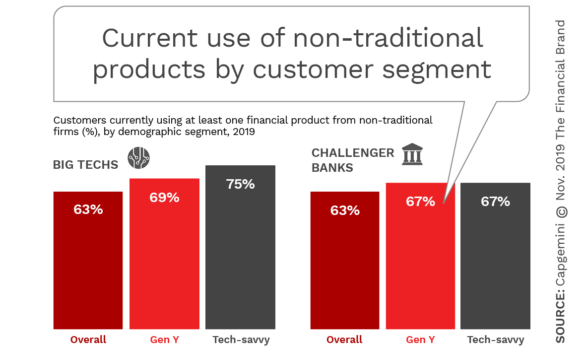

The World Retail Banking Report 2019 from Capgemini outlines the increasing acceptance of fintech and big tech offerings.

- 75% of tech-savvy consumers are currently using at least one financial product from a big tech provider.

- The top three reasons customers say they use non-traditional players are lower costs (70%), ease of use (68%), and faster service (54%).

- More than 80% of consumers likely to switch financial providers are currently using payments, cards, or banking account products from a big tech firm or challenger bank or are likely to do so in 3 years.

With regards to using partnerships or collaboration to build real-time contextual solutions, traditional banks have looked to startups for their speed, innovation focus and focus on the customer experience. Fintech firms look to traditional financial institutions for their large customer bases, access to capital, brand recognition in the marketplace and understanding of compliance and regulations.

Unfortunately, the movement to partner with fintech firms has been sluggish or non-existent at traditional banks and credit unions. According to Capgemini, only 33% of banking executives say they have effectively implemented Open Banking.

A question to be asked: Can banks and fintech firms even work well together? “Startups and big companies live in very different world: They hire people differently, they operate differently,” states Serguei Netessine, Wharton Professor of Operations, Information and Decisions. Netessine has been looking at the the startup revolution for years, having co-authored a report that examined how the world’s largest companies were dealing with newer, more agile firms.

Read More:

- Secret To Digital Banking Success is AI With “Human-Like” Feel

- Just Because Banking Customers Don’t ‘Switch’ Doesn’t Mean They Love You

The Open Banking Experience Opportunity

According to the Capgemini report, “To succeed, banks and credit unions need to strategically choose partners that complement product portfolios, enhance service delivery, boost sales – and work collaboratively. By leveraging effective collaboration while also maximizing traditional strongholds, banks can create a powerful advantage in the Open Banking era.”

More important than simply using Open Banking as a new product extension opportunity, Capgemini suggests that organizations need to focus on how potential partnerships can enhance overall customer experiences. This form of collaboration could provide opportunities to all ecosystem participants, provided that both traditional and non-traditional firms play to their strengths and are ready to collaborate.