Financial institutions globally are at a significant juncture in their history, where they need to make a strategic decision – whether to become a banking ‘utility’ supporting other providers’ customer-facing solutions, or become a central resource in a consumers’ daily life. More than simply being the provider of traditional banking products, the future may see progressive banking organizations become a resource for entertainment, travel, hospitality, retail and a host of other services.

Although the use of APIs is not new, growth in their usage has expanded in unison with the growth in digital solutions. Today, APIs are now being adopted across various industries enabling new digital solutions. The opening of account APIs in financial services is an important step towards ‘Open Banking’ – providing tremendous potential for banks and other financial institutions to innovate, create new solutions, and potentially ‘disrupt the disruptors’.

The move to open APIs will definitely increase the rate of disruption within the financial services industry. The keys to success will be to gain a full understanding of the potential disruptive threats, and to adapt to this changing landscape by evolving ‘Banking as a Service’ (BaaS) business models to leverage APIs as an enabler of new products and services.

According to a PwC research paper, “When consumers can manage a variety of financial products and services from different institutions with one application, it will facilitate the cross-institution movement of money and accounts and will dramatically improve the flexibility of consumers to pick and choose products seamlessly from competing providers. More importantly, consumers will be able to see and act on their full financial profile at a glance, thereby allowing them to make better-informed decisions.”

Rethinking Banking as We Know It

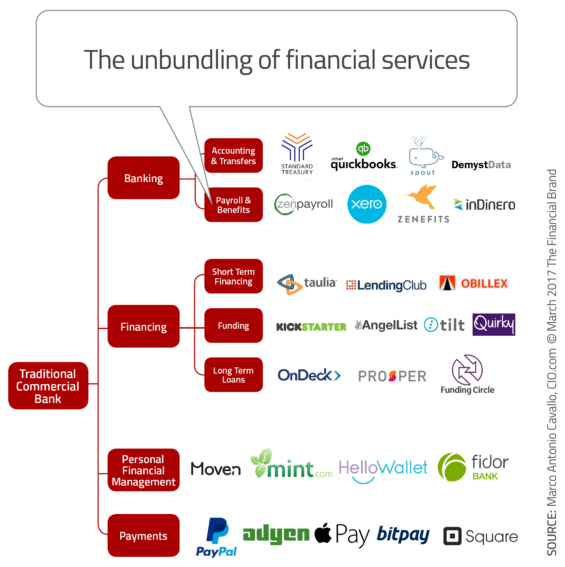

Over the past several years, fintech firms have been disrupting traditional banking organizations across virtually all product lines, making innovative plug-and-play, multi-channel and easy-to-use banking solutions available to the masses. These offerings include digital wallets, P2P payment products, wealth management solutions and lending services.

While initially seen as a direct threat, these innovative insurgents are now seen as potential partners in the delivery of personalized services to an established customer base of legacy banking organizations. Banks must rethink product development and delivery across multiple channels, providing personalized solutions that support the customer requirements of “know me, look out for me and reward me.”

To take advantage of this new Banking as a Service model, financial services organizations will need to build partnerships with outside providers, rework distribution models, significantly enhance digital experiences and leverage internal data to find the right match between the consumer and product/service offerings.

Potential Loss of Customer Relationship

The banking industry has traditionally enjoyed a central role in their customers’ financial lives. With the entrance of both fintech and large technology providers as financial players, this relationship has changed. The relationship between banks and customers has evolved from face-to-face engagement to less personal digital engagement through the years.

While this evolution, by itself, has not threatened the relationship between bank and customers, or the sense of customer ‘ownership’ that banks enjoyed due to ‘loyalty inertia’, the path towards open APIs could eventually change this dynamic. As access is granted to alternative providers, via APIs, banks are at risk of losing a direct relationship with the customer and being relegated to more of a ‘dumb pipe’ commodity status.

Access to customer account data by a third party creates a scenario where customers could fulfill their daily banking needs (viewing account balances, transaction histories and payments) all from a third party portal with no meaningful engagement with, or even visibility of, the traditional bank’s brand. This scenario could present a threat to incumbent banks by providing a single platform of financial services not ‘owned’ by a traditional banking organization, but by a fintech firm or major tech player.

Product aggregation services such as NerdWallet offer information about a wide range of financial products and services, allowing the customer to select the ones that fit their needs. Money Dashboard or Digit and others provide tools to assist a customer in managing their finances. Companies such as Varo Money and Bud allow consumers to cross-shop products within the application and offer one-stop, multi-account management through an API.

According to a report from Accenture, customers in any of these scenarios could access multiple stand-alone financial services products, all integrated with their existing account and transactional data. If this occurred, it would remove the opportunity for banks to cross-sell and engage their customers, with less customer insight and data being available to the legacy banking organizations. “With less customer data, the legacy banks would enter a negative feedback loop in which their ability to compete would steadily decline, eroding a key competitive advantage that banks currently enjoy through their wealth of customer data and insight,” stated Accenture.

Opportunity for Enhanced Relationships and Revenues

Until now, legacy financial organizations have benefited from hurdles associated with switching financial service providers. In the U.S., less than half of the consumers who indicated a desire to switch providers actually followed through with their intentions. In the U.K., where the process of switching accounts was made easier due to account number portability, less than 2% of households switched providers.

Eventually, consumers will realize the experiential and pricing benefits provided by the new fintech players. When that time comes, those legacy organizations that leveraged the benefits of API integration, combined with their existing customer relationships, to develop their own banking portals will be the winners.

Progressive banking organizations are already beginning to build partnerships with fintech providers which will expand product and service options and provide the platform for product and revenue growth. “Financial services industry statistics suggest that households with 6.6 banking products on average generate twice the revenue of customers with the standard average of 2.7 products,” the PwC report noted. “The most prolific customers – those with an average of 16.6 products, which usually include both personal and small business accounts – generate nearly 17 times the revenue of a standard two-product customer.”

Where to Start

Moving from being a traditional banking organization to a digital-first provider of customer-centric financial (and non-financial) solutions involves a series of steps from exploration through implementation. In an excellent article written by Marco Antonio Cavallo for CIO.com, the following steps were suggested:

- Preparing, adapting or building a solid API-led ecosystem;

- Choose and formulate the most suitable API strategy;

- Selecting partners that are in line with your company’s market and customer strategy;

- Building strong partnerships with fintech firms and independent software developers to support and monetize APIs;

- Have a change management strategy in place to implement and keep moving the Banking as a Service (BaaS) strategy forward within your company;

- Ensure the strategic alignment between business objectives and your BaaS project.

According to Cavallo, “If banks are able to successfully implement an open banking BaaS strategy, they can evolve from being just a mere peripheral institution in the digital age and become an important broker that enables many different benefits for consumers and partners across the digital value chain, expanding their partners’ customer base, enhancing innovation and creating new revenue sources.