From bricks and mortar to laptops and PCs — and now to smartphones and tablets — consumers increasingly want to manage all aspects of their lives on the go. This transition from physical to digital channels has been embraced by retailers, the travel and hospitality industries, and other verticals. For the banking industry — especially in the US — the transition has been more challenging.

Maybe it is due to the complex nature of financial services, or consumers’ concerns about identity and security. Or, maybe it’s because the banking industry is risk averse, reluctant to change, and supported by antiquated systems that has made the movement to a more mobile-friendly environment difficult.

As digital technology evolves and mobile banking transactions become more popular, banks and credit unions are facing an unprecedented opportunity… and competitive risk. Consumers are increasingly willing to make large and important life decisions with a tap of an app, click of a browser or recommendation from a social media acquaintance. Banking providers need to ensure they are seen as as a digital financial partner by providing a user experience that is intuitive, engaging and contextual.

Mobile Banking Is a Key Differentiator for Banking Brands

According to the Federal Reserve’s 2016 Consumers and Mobile Financial Services Report, 43% of adults with mobile phones and bank accounts reported using mobile banking. This was an increase from 39% a year earlier. Usage of mobile banking increases to 53% for smartphone owners with bank accounts, up from 52% in 2015.

Consistent with previous years, the three most common mobile banking activities among mobile banking users were checking account balances or recent transactions (94%), transferring money between an individual’s own accounts (58%), and receiving an alert (e.g., a text message, push notification, or e-mail) from their bank (56%).

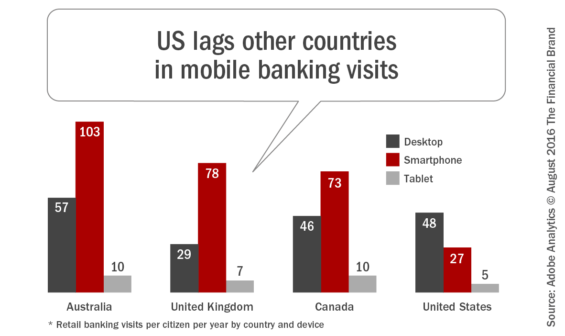

Despite this growth, smartphone mobile banking usage lags the use by other countries by a significant amount according to the Adobe Digital Index: State of Banking Report.

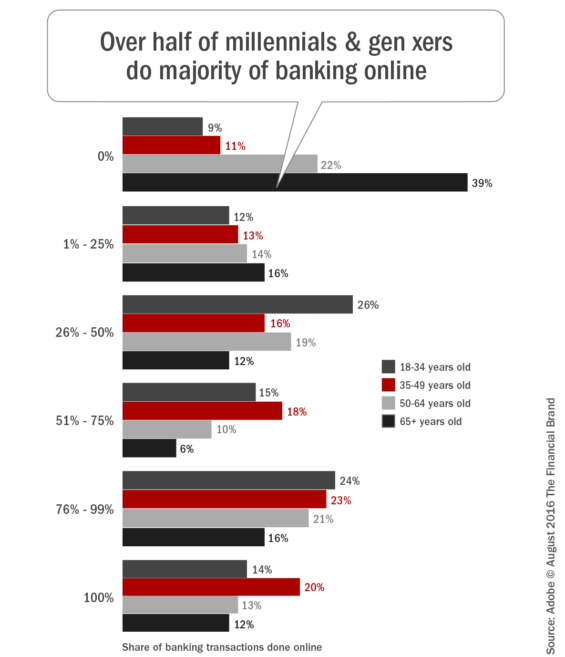

While the US lags other countries in mobile banking use compared to other channels, don’t tell that to Millennials or Gen X. According to Adobe, both of these segments do more than half of their transactions digitally.

As might be expected, older segments of the population are less likely to be digital natives. However, wealthy consumers in all segments tend to use mobile banking more frequently. In other words, to satisfy the most valuable consumers and the fastest growing segments, financial institutions need to provide best-of-breed mobile capabilities.

The need to differentiate using the mobile channel becomes more evident when we take into account the increasing use of smartphones, the willingness to consider a “bank without branches,” and the number of consumers who have already used their mobile device to obtain a financial product/service. In fact, one in five Millennials and one in seven Gen Xers would apply for a new account or loan using their phone, according to Adobe.

- 92% of Millennials consider their smartphone their primary device vs. 84% of Gen X who say they feel the same way.

- 61% of U.S. consumers would consider a mobile-only bank.

- 43% of U.S. consumers are applying for new bank accounts, credit cards, loans or brokerage accounts from their mobile device.

- 20% of Millennials and 14% of Gen X would apply for a new account or loan using a mobile device, while only 2% of Boomers would do the same.

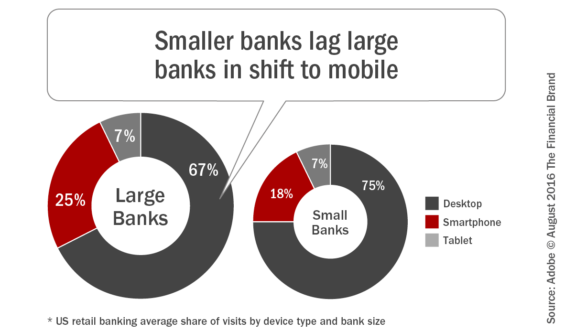

The ability to become a ‘digital bank’ is happening quicker at the larger U.S. financial institutions. Adobe found that an average of 25% of larger bank digital transactions are being done on a mobile device, while only 18% of transactions at smaller banks are mobile. This difference in distribution shift is even more apparent at the top five banks, something discussed in a previous article from The Financial Brand which showed Bank of America’s mobile app is 12 times more popular than its branches and 80% more popular than their online channel.

Mobile Banking Delivery

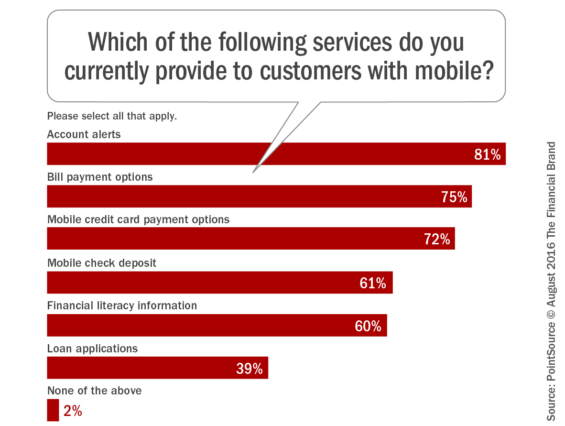

According to the PointSource report, “State of the Mobile Experience,” basic day-to-day banking activities are the most common mobile offerings by financial organizations. Of those companies already offering mobile banking to customers (92% of institutions offer some form of mobile banking), alerts are the most widely offered mobile service in banking, with four in five responding companies (81%) providing it to their customers. Mobile bill payments (75%), mobile credit card payments (72%) and mobile check deposits (61%) are also common.

Despite offering a relatively wide array of mobile offerings, banks and credit unions still believe their customers’ two biggest pain points are completing routine personal banking tasks (i.e. making deposits, paying bills, etc.) (56%) and accessing personal financial information in real time (52%).

Interestingly, 84% of financial institutions with an existing mobile presence ranked their current mobile experience at a seven or above on a 10 point scale, despite there being a clear need to improve and simplify the user experience when it comes to executing basic day-to-day tasks. As mentioned by PointSource, “With all banks offering a relatively similar scope of mobile capabilities, the user experience — its ease, responsiveness and speed — can distinguish companies from the rest.

Mobile Experience Matters

Starting a relationship with a financial services institution has never been easy. Traditionally, consumers were required to visit a branch, provide identification and supporting documentation, fund the account and sign the appropriate documents. With these paper-based processes as the starting point, no wonder it has been so difficult for banking organizations to become mobile-first.

Despite the increasing demands from the digital consumer for simple and intuitive applications that leverage the capabilities of the smartphone, most mobile application application processes currently offered by banks and credit unions are simply digital versions of existing web-based apps … difficult to navigate and not aesthetically pleasing to use.

In fact, according to research done by Episerver, one in five consumers claim that they are overwhelmed by the amount of information in financial service apps, 44% consider ease of use to be a significant factor when deciding whether to download such apps, and 63% of US consumers would abandon a site if it is too difficult to access. The same study found that while consumers are annoyed by the complexity of financial apps, 34% say they are frustrated by the limited functionality offered by mobile-specific applications and sites.

To address this paradox, and overcome the wide variety of financial products and services, some financial organizations have developed different mobile apps, each with their own specific function. Other organizations have focused on removing all unnecessary steps and used the capabilities of the smartphone to streamline processes (photo ID verification and use for pre-fill, address book use for P2P payments, etc.).

Finally, of those surveyed, one in five customers expect mobile applications to include additional content and advice. According to Episerver, “The demand for content and advice is especially high within the financial sector, where complex purchases often leave customers confused and seeking easy to understand how-to guides for financial advice.”

Four ways that Episerver recommends banks and credit unions should improve the customer experience include:

- Design with customer intent: Provide persuasive and informative content, without cluttering the overall buyer journey. Optimize for maximum usability — ultimately driving customers towards a sale.

- Simplify the approach: Balance user experience with device capabilities, providing a high level of continuity in terms of both usability and design.

- Balance security and ease of use: Make the most of new authentication technologies in a user-friendly way.

- Convert with content: Apps that embrace how-to guides, video content and in-app tools (finance trackers, loan calculators, etc.) will build customer trust, influence buying decisions and increase mobile sales.

The Importance of Getting Mobile Banking Right

Getting the bank’s mobile strategy right is critical, according to KPMG, “While the potential rewards are ‘exceptionally high’, failure could spell the ‘relatively fast decay’ of the business.”

This adds to the pressure for those who manage mobile development and digital customer experience at financial institutions. While mobile technology, use and expectations are part of a rapidly changing world, banking is slower, weighed down by legacy systems and cultures from decades ago. As a result, banking has struggled to respond to shifts in the market, and to deliver developments in an agile manner.

The banks that win at mobile will be those that understand their customers, adapt quickly, and deliver a high quality, comprehensive experience in a time frame considerably shorter than has traditionally been considered acceptable.

As probably surmised best in a white paper from Shinobi Controls, a good mobile experience delivers …

- An amplified brand experience

- Deeper, more personalized relationships

- Faster access to better information

- Improved decision-making

- Better money management

- Enhanced financial inclusion

According to Shinobi Controls, “Increasingly, getting mobile apps right will impact on a bank’s ability to acquire and retain not only customers, but employees and intermediaries as well. So, getting it right is critically important. It’s not enough to have an attractive app — it has to deliver real insight and has to provide intelligence which helps people make decisions which turn out right — for themselves or for the bank.”