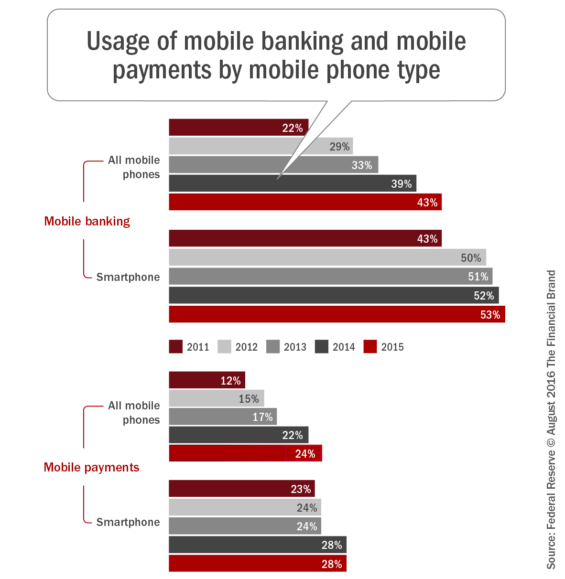

For the fifth consecutive year, the Federal Reserve has conducted a survey examining trends in the adoption and use of mobile banking, payments, and how mobile financial services impact how consumers engage with their financial institution. According to the Federal Reserve Board report, 43% of adults with mobile phones and bank accounts reported using mobile banking — an increase of 4% from last year’s survey and 10% from the 2013 study.

As would be expected, mobile banking use is significantly higher for those consumers with smartphones (53%). Among smartphone owners with a bank account, the increase in users increased only 1% during the past year, the same amount as in the previous 3 years. This almost stagnant growth continues to raise the question as to whether the growth in mobile banking use is caused by the increase in consumers upgrading their mobile devices as opposed to being the result of marketing efforts by banks and credit unions.

Use of mobile payments continues to run at about 50% of the overall mobile banking user base, with 28% of the smartphone users with bank accounts having made a mobile payment in the past 12 months and 24% of all mobile users indicating the same. Despite significant hype of mobile payments by the banking industry, there was no growth in use by the key target of smartphone owners.

Of particular concern to banks and credit unions should be that there is still a significant proportion of consumers who have no desire to use mobile banking or make mobile payments in the near future. The reasons for non-use vary from being satisfied with current ways of conducting banking to not feeling that mobile channels are secure. It remains to be seen whether continued improvement in functionality and security features will result in new mobile banking users or simply a shift in market share of current users from one organization to another.

Mobile Banking Demographics

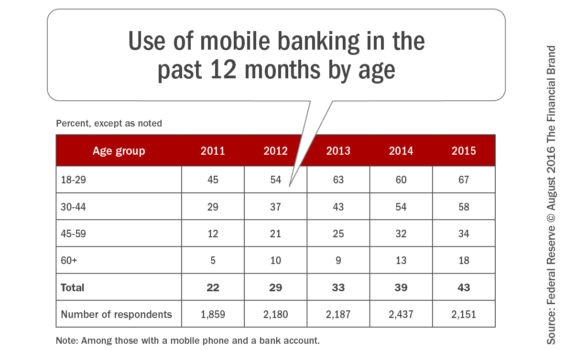

Reflecting the rates of mobile and smartphone usage among different demographic segments, younger consumers are more likely to use mobile banking than older consumers. For those with a mobile phone and a bank account, 67% of those in the 18 – 29 age range used mobile banking in 2015 compared to only 34% for those in the 45 – 59 age group. Usage has generally increased from year to year for all age groups, and is greater for smartphone owners. The rate of growth has been higher for the older segments, who were slower to adopt mobile banking initially.

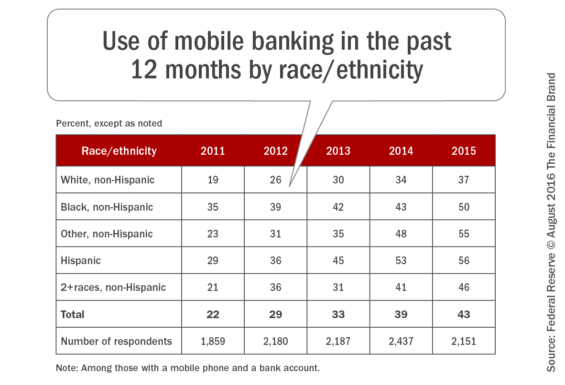

Also consistent with the data from previous surveys, minorities continue to be more likely to use mobile banking than non-Hispanic whites. In particular,

Hispanic mobile phone users with bank accounts showed a higher rate of use of mobile banking (56%) compared to mobile phone users with bank accounts overall (43%). As with most segment delineation, the difference in use by minorities correlates with mobile and smartphone usage variances.

Finally, the Federal Reserve study found that mobile banking usage continues to be more common for those with higher levels of education and those with higher incomes. Usage for those with a college degree or some college (47%) is greater than for those with a high school degree or less (35%), while mobile banking usage by households with incomes of $40,000 or more exceeded use by those with incomes below $40,000 (45% vs. 38% respectively).

Mobile Banking Activity

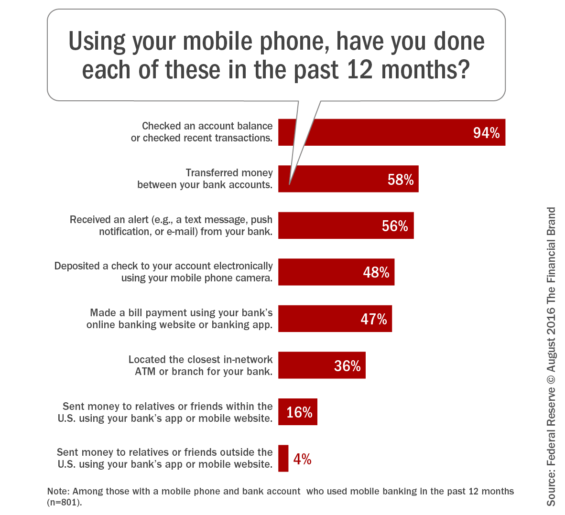

Consistent with previous studies, the most common mobile banking activity was checking financial account balances or transaction inquiries, with 94% of mobile banking users having performed this function in the 12 months prior to the survey. This was the exact percentage as in the previous year’s survey. The next most common activities were transferring money between accounts (58%) and receiving an alert from their financial institution through a text message, push notification, or e-mail (56%), with both activities being done less than last year.

Depositing a check to an account using remote deposit capture and making an online bill payment from a bank account using a mobile phone were the next two most common activities, done by 48% and 47% of mobile banking users, respectively. These activities were also done a bit less than indicated in last year’s study.

Interestingly, while some activities were less used, significantly more consumers indicated that they had installed their bank’s application on their phones in 2015 (82%) than in 2014 (71%).

Among all mobile banking users, the frequency of mobile banking use has been relatively consistent over the past several years. Among those who used mobile banking in the month prior to the survey, the median reported usage was five times per month in both 2015 and 2014, and four times per month in 2013.

High intensity users (those who conduct mobile banking tasks more than 10 times per month) tend to conduct all activities at the same or higher rates than the average mobile banker, especially transferring money between their own accounts, making bill payments and receiving alerts. Not surprisingly, high intensity users tended to include higher shares of younger, Hispanic, more educated and wealthier mobile users.

Channel Use Among Smartphone Users

According to the Federal Reserve study, “Most consumers with bank accounts reported using a mix of online and offline channels to interact with their financial institution. For those who have adopted mobile banking, use of the mobile channel appears to complement their use of other banking channels.”

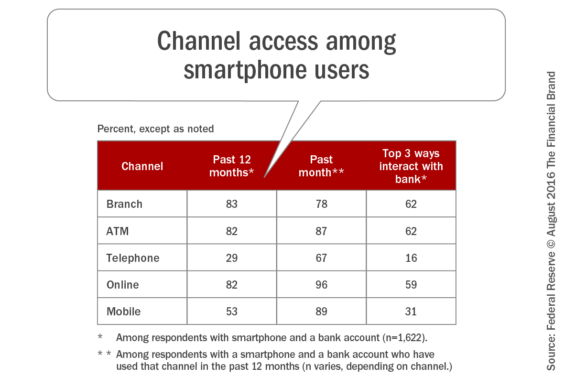

Among mobile banking users with smartphones, 31% stated that the mobile channel was one of the three most important ways that they interact with their bank. This was a lower percentage than for online (59%), ATM (62%), and even a teller at a branch (62%). This lower share mentioning mobile banking as important is partially due to the overall adoption rate of mobile banking relative to other channels.

For smartphone owners who use mobile banking, 54% cited mobile as a top three channel, below online (65%) and ATM (62%) but above branch use (51%).

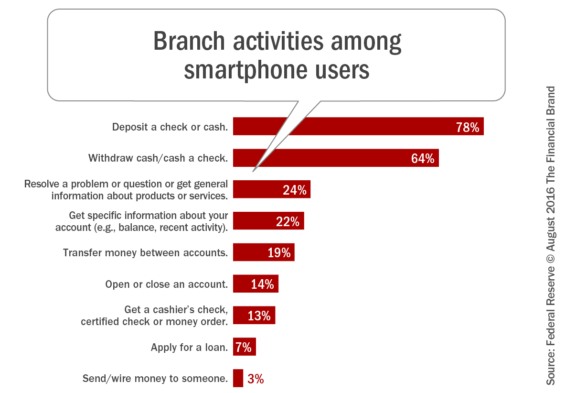

Among smartphone owners with bank accounts who reported using a branch in the past 12 months, the primary reasons for visiting a branch were to deposit or cash a check (78%) or withdraw cash/cash a check (64%). This indicates that, even among smartphone owners, there is still a reliance on traditional channels for activities that can be performed on a mobile device.

Reasons for Using and Not Using Mobile Banking

Consistent with findings from prior years, a majority of consumers using mobile banking and mobile payments cite convenience (39%) or getting a smartphone (26%) as their main reason for starting to use mobile banking. An additional 19% of consumers indicated that their use of mobile banking was driven by their bank or credit union starting to offer the capability.

Among consumers who have mobile phones and bank accounts but do not use mobile banking, the main impediment to adoption of mobile financial services continues to be that their needs are being met without mobile banking (88%). Other significant hurdles included, “I do not see any reason to use mobile banking” (78%), and “I am concerned about security” (73%).

Less important issues mentioned were the small size of the mobile screen (43%), a lack of trust in technology (40%) and not having a smartphone (27%). Each of these reason are relatively consistent over the past three years, except for not having a smartphone, which has decreased in mention over time.

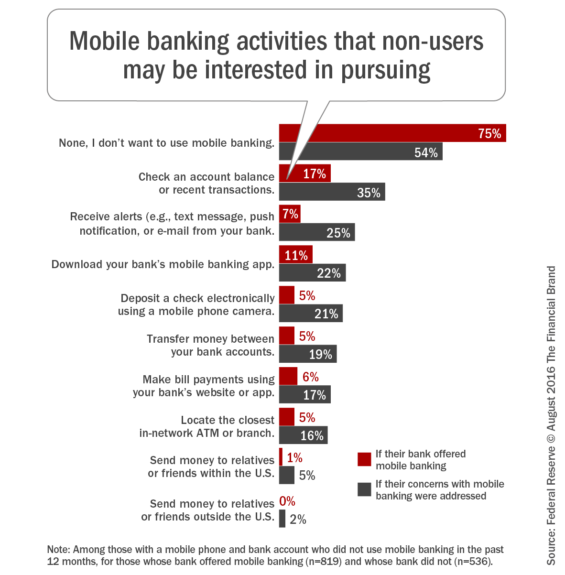

Of those who have a mobile phone and checking account but do not currently use mobile banking were asked what activities they may be interested in pursuing. While 17% stated the ability to check balances or transactions, 75% stated that there were no activities that would interest them. In fact, 54% stated they would not be interested in mobile banking even if their concerns about mobile banking were addressed.

Mobile Payments Activity

For the Fed study, mobile payments are defined as “purchases, bill payments, charitable donations, payments to another person, or any other payments made using a mobile phone. This includes using your phone to pay for something in a store as well as payments made through an app, a mobile web browser or a text message.”

Use of mobile payments continues to be less common than use of mobile banking. Twenty-four percent of all mobile phone users, and 28% of smartphone users, made a mobile payment in the 12 months prior to the survey. While younger consumers are more likely to make mobile payments, the percentage of consumers in 18-29 year old segment making mobile payments actually went down for the first time in 2015. As with the use of mobile banking overall, use of mobile payments is higher for minorities, higher income consumers and those with higher educational levels.

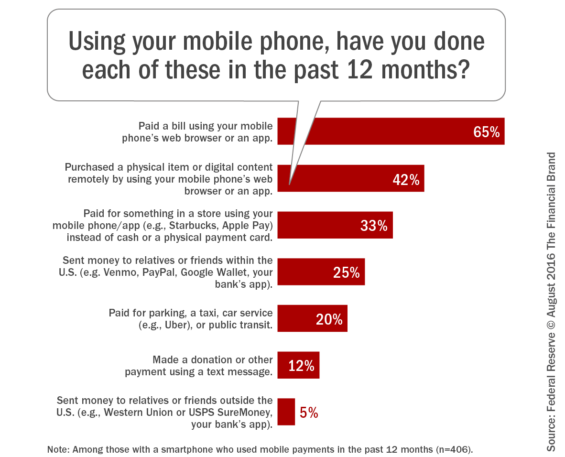

For smartphone owners who reported making payments with their phones, the most common types of mobile payments were paying bills (65%), purchasing a physical item or digital content remotely (42%), paying for something in a store (33%) and sending money to relatives or friends within the US (25%).

When asked why consumers use mobile payments currently, convenience was the most mentioned reason (45%) with “getting a smartphone” being the second most mentioned reason (20%). For those who have not tried mobile payments, a whopping 80% stated it was easier to use other methods of payment, with 67% being concerned about security of making a mobile payment and 65% not seeing a benefit of making a payment with a mobile device. These reasons for not trying mobile payments are consistent with the most recent previous studies in 2013 and 2014.

Similar to the non-users of mobile banking, a significant percentage of non-users of mobile payments (74%) indicated they would have no interest in mobile payments even if their concerns were addressed.

The Future: Market Shift or Market Growth?

Over the past several years, the rate of growth for both mobile banking and mobile payments is best categorized as slow and steady. The reason for beginning to use both mobile banking and mobile payments has shifted from being driven by ownership of new technology to a desire for digital convenience.

That said, the reasons for not using mobile banking or mobile payments has not changed significantly over the past several years, with consumer concerns not adequately addressed by the banking industry. So, despite other industries like retail, hospitality and travel converting large numbers of consumers to digital solution, the banking industry has seen more shifting of market share to larger banking organizations with better applications than a growth in penetration overall.

To benefit from the cost savings and revenue potential of mobile banking and payments, the banking industry must do a better job of educating the digital consumer of the benefits of the mobile channel. It is also important for smaller organizations to build better mobile applications to avoid additional shift in digital consumer market share.

About the Study

The Federal Reserve Board report, “Consumers and Mobile Financial Services 2016,” was conducted on behalf of the Federal Reserve by GfK, an online consumer research firm. The 2015 survey was conducted from November 4-23, 2015. More than 2,500 respondents completed the survey.