Home prices are up 6% from a year earlier, and home equity continues to grow. According to CoreLogic, home equity had risen in the second quarter of 2018 by 12.1% year over year. In dollars, that means a gain of over $1 trillion in the quarter, coming to about $16,200 per home.

TransUnion projects that 10 million Americans will originate home equity lines of credit (HELOCs) between 2018 and 2022. That’s more than twice the level originated in the previous five-year period — a rich vein of demand waiting to be tapped.

But a multitude of factors determine the success of home equity promotions. You have to understand how consumers learn about home equity loans and lines. You need to figure out which prospects are best-suited for these products and what they look like. You have to look at the the role of technology in marketing and where the strongest cross-selling points exist. And none of this matters if you don’t understand where and how people prefer to apply for home equity credit.

Major banking providers — notably Chase, BofA, Wells Fargo, and U.S. Bank — dominate home equity lending with around half the market. Credit unions have 14% of the market, while mortgage brokers hover around 9%, according to a report from Phoenix Synergistics.

According to the firm, home equity borrowers are oriented to use credit and tend to need it. Three quarters have used other forms of credit in the previous year, and 84% expect to need more. Borrowers’ average annual household income is $85,600; their average level of liquid assets is $197,500; and their average estimated home equity to draw on is $181,300.

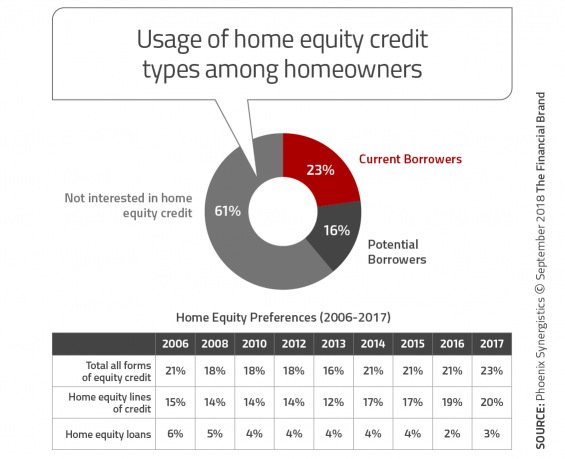

Less than one in four homeowners currently have home equity credit of some kind, according to Phoenix Synergistics. The firm’s research found that 7 out of 10 who currently have HELOCs obtained them from the lender where they obtained their first mortgage, suggesting that many prospects may be consumers that your institution knows already.

Genie Driskill, COO and Director of Research at Phoenix Synergistics, says banks and credit unions that have not yet moved back into the home equity market should strongly consider it.

“It’s a very attractive market, in terms of the current borrowers,” says Driskill.

Gen X in Home Equity Credit Crosshairs

Home equity borrowers have an average age of 45. That places them smack in the middle of Generation X. According to the Pew Research Center, Gen Xers were hit especially hard by the Great Recession in part because they bought at the top of the market and most of their net worth lay in their homes. However, Pew’s analysis of Federal Reserve data indicates that today’s markets have made Gen X the only generation to recover the wealth they lost — their home equity has doubled since 2010. And they can access it now via home equity credit while they are in their prime working years.

“With most consumers still paying down a primary mortgage, they may be reluctant to take on more debt, even with the potential benefits of debt consolidation,” states a report by Mintel Group. “Lenders have an opportunity to highlight the benefits of this type of loan, while ensuring that any additional debt taken on by the consumer can be effectively managed and paid down.”

When Phoenix Synergistics asked homeowners where they first heard about HELOCs, the top source reported was local bankers:

- Local bank branch representative — 38%

- Personal research — 32%

- A loan officer — 23%

- Information from main mortgage lender — 22%

- Friends or relatives — 20%

- Financial advisor or planner — 16%

- Mortgage broker — 16%

- Accountant or tax advisor — 13%

- Real estate agent — 12%

Read More: Home Equity Borrowers Admit They Don’t Know Squat

Reasons Why Consumers Tap Their Equity Have Shifted

Years ago, marketing of home equity credit products often promoted “the good life,” with pictures of glamorous vacation destinations and other such symbols. The idea of treating one’s house as a piggy bank seemed to catch on culturally. But Driskill says much of this attitude has gone away.

“Consumers have become serious about this product,” says Driskill. “They now want home equity credit for serious purposes.”

The firm’s research indicates that 40% of homeowners surveyed use proceeds for home improvements or repairs. About a quarter of borrowers (23%) use the funds for emergency expenses; while a similar number (22%) use them to consolidate debt or to pay off debts, since rates are typically less than those charged on other forms of consumer credit.

Getting on Homeowners’ Borrowing Radar

Having a relationship with prospective home equity borrowers gives the would-be lender an advantage. Being the prospect’s original mortgage lender is a strong factor. Being their primary financial institution — the provider of their checking account — also helps. Driskill emphasizes the need to market home equity credit to consumers the institution already knows.

Driskill points out that more and more go for a “piggyback” approach, obtaining both their primary mortgage and a HELOC simultaneously with the same lender. She adds that institutions need to market home equity services heavily to both mortgage borrowers and checking account holders, because they both represent strong opportunities.

While large banks dominate home equity lending, an advantage all lenders with branches have is their physical presence. This suggests that smaller institutions can play up their local connection and knowledge.

Driskill says that some consumers may perceive that a lender with local knowledge will provide a larger amount of credit than an out-of-town lender. Her firm’s research found the following factors rated “extremely important” by home equity borrowers:

- Have local offices — 36%

- Confidence they’ll be approved — 35%

- Main or primary financial/depository institution — 33%

- Large, well-known institution — 30%

- Get a better deal or discount because have other relationships at that institution — 29%

Read More: Do the Majority of Americans Really ‘Want’ to Use a Branch?

Reaching Out to Prospective Equity Consumers

Phoenix Synergistic’s research finds that home equity borrowers as a group don’t shop around, even in these days of easy web searches. Research by J.D. Power indicates that 88% of HELOC borrowers begin looking before they are solicited. And more than half of both those shopping for credit lines and those seeking closed-end equity loans look at only one lender, according to the research.

Looking at the direct mail and email marketing of home equity lenders by Mintel reflects active marketing efforts by both smaller and larger companies. Looking closer at these campaigns reveals that:

- Direct mail goes into more detail than email solicitations, and the more depth, the greater the compliance-oriented copy that’s needed to back up the promotional language.

- “Inclusion” appears to be on financial marketers’ minds. Where photos of people are included, often non-white are portrayed.

- Serious uses for equity credit proceeds tend to be emphasized. Kitchen remodeling often gets pictured or mentioned prominently.

- Where the idea of borrowing for travel is even mentioned, it’s couched with phrases like “a much-needed vacation.” Among other “fun” uses of home equity, home pools still show up frequently, in spite of more “serious” thinking about home equity borrowing.

- Financial incentives frequently show up, such as lower initial rates and fee waivers.

Some pointers from a Harland Clarke webinar on HELOC and home equity loan marketing:

- Emphasize that equity credit lines can be a smart and flexible financial tool.

- Call out a competitive rate offer — “Rate is king.”

- Use an offer end date to add urgency.

- Adapt the message seasonally: bring up tuition expenses in summer promos, paying off high-interest holiday debt in January.

- Keep the offer straightforward — don’t try to cross-sell in the same message.

Equity Credit’s Digital Frontier

Beyond factors already cited, home equity lenders must realize that the digital trends already rocking many other elements of bank and credit union business aren’t ignoring this product line.

In releasing its 2018 U.S. Home Equity Line of Credit Satisfaction Study, J.D. Power emphasized the encroachment of digital channels into this space.

“Lenders need to recognize that the HELOC customer experience is a journey that begins with initial consideration and evaluation and extends through to usage, with each part of the journey affecting overall perceptions,” said Craig Martin, Senior Director of Financial Services at J.D. Power. “Increasingly, many steps in that process are occurring in digital and mobile channels, which are areas that the industry has been slow to leverage and refine.”

Within the time frame that TransUnion identified for home equity credit growth, the oldest Millennials — 38 now — will be four years closer to the sweet spot Phoenix Synergistics identified of 45 years.

“As Millennial homeownership rates increase and home values continue to rise, lenders need to be able to meet these customers where they want to be, not try to force them into the lender’s entrenched methods,” said J.D. Powers’ Martin.

Key factors from the firm’s study to consider:

Comparison shopping is stronger among Millennials. Remember that Millennials’ level of trust was forged in the Great Recession and that internet searching for everything is a natural for them. While Power found that 55% of its respondents overall compared at least two lenders in shopping for a HELOC, among Millennials, 80% shopped among at least two lenders.

Not borrowing blithely. Power found that 64% of all HELOC borrowers surveyed have some concerns about borrowing more against their homes. Among Millennials, 87% have such concerns.

Digital channels grow critical for younger borrowers. In this study, 66% of consumers gathered HELOC information in person overall. However, among Millennials, 59% relied on desktop computers to get information online, and 50% obtained some information via smartphones and tablets.

Even here, there’s a balancing point from Mintel: “Only 20% of the consumer population is currently ready for a mobile application process and 27% are ready to apply online. The in-person experience cannot be fully abandoned in search of a more technologically-savvy process.”

Read More:

- Secret To Digital Banking Success is AI With ‘Human-Like’ Feel

- 5 Actions To Accelerate Your Digital Transformation Journey