With more than $25 billion invested in an estimated 4,000 fintech firms in the past five years, it is surprising to many that this investment represents just a small fraction of the overall banking industry. And while there is a great deal of hype surrounding the potential for digital disruption, fintech firms face significant challenges to growth, and the banking industry is trying to determine whether they should ignore, acquire, partner or compete with their new technology-driven competitors.

As transformation of the banking industry continues, fintech firms and legacy banks are beginning to realize the benefits of working together to deliver innovative solutions and superior customer experiences to an increasingly digital consumer. Fintech firms see the advantages of leveraging banking’s large and loyal customer bases, experience with risk and regulations, a broad product set, established trust and the deep financial pockets of incumbent banking organizations.

”The holy grail for banks is to become the best at ‘fintegration’.”

— Andres Wolberg-Stok, Global Head of Emerging Platforms and Services at Citibank

Alternatively, most incumbent banking organizations need the fintech advantages of not having to work with old, legacy operating systems, an innovation agility unheard of in traditional banks, a better understanding of today’s technologies and a laser focus on narrow solutions. The question is whether these new partnerships can preserve the culture of the fintech firms, while allowing legacy banks to be the hub of the consumer’s financial relationship?

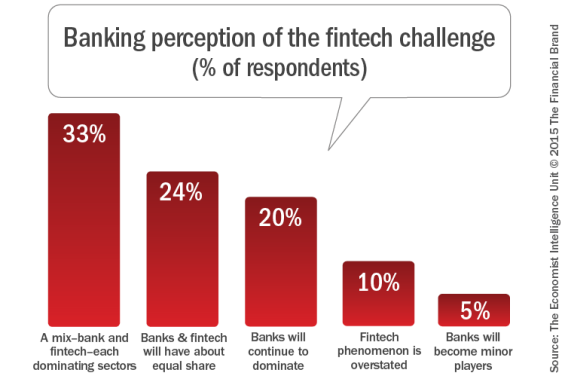

Banking’s View of the Fintech Challenge

In a report published by the Economist Intelligence Unit, over 100 senior bankers and 100 fintech executives were interviewed to ascertain the likely landscape for the retail banking industry over the next five years. When bankers were asked how fintech may disrupt the banking industry, more than 90% of bankers believed that fintech firms will have a significant impact on the future landscape of banking, with more than a third believing that fintech will win an equal share (24%) or even dominate the market (20%).

When asked about banking’s response to the fintech challenge, a majority of bankers (54%) believe that banks are either ignoring the challenge or that they “talk about disruption, but are not making changes”. Interestingly, an even larger percentage of fintech executives (59%) agree with them.

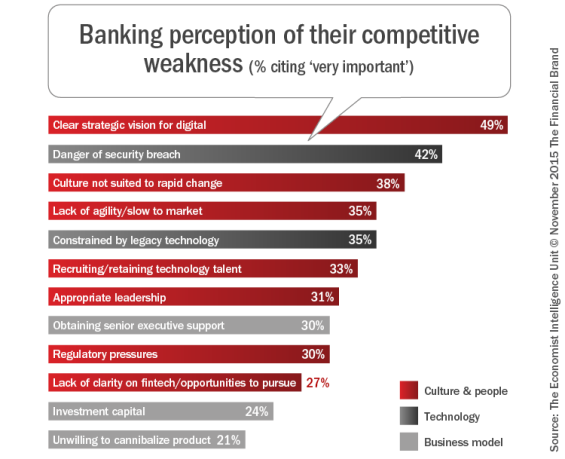

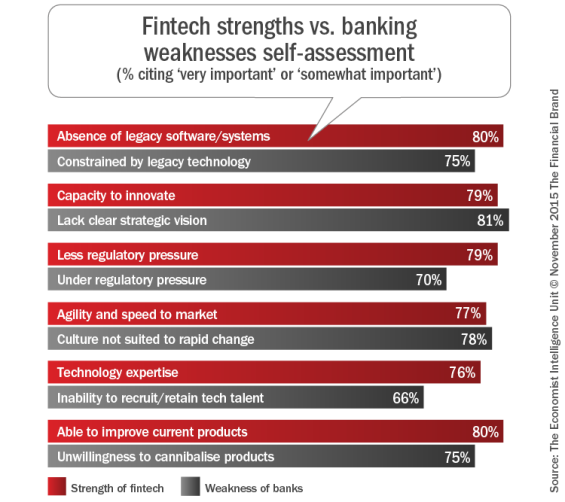

Bankers see the primary barriers to developing an adequate response to the fintech challenge as the combination of a lack of a clear digital strategy, an underlying culture unsuited to rapid change, and the inability to attract top technological talent. An ongoing challenge to the banking industry is the legacy technology systems which in many cases date back to the 1970s or 1980s.

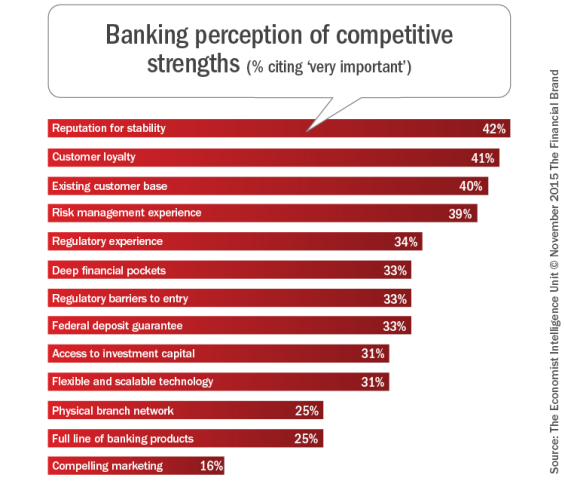

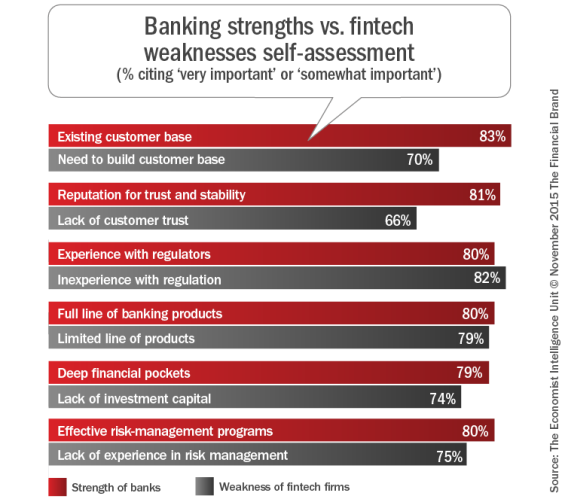

When bankers were asked about the strengths of the industry, the reputation for trust and stability topped the list, with the advantage of current customer relationships and loyalty also being important. The EIU report notes that regulation presents a double-edged sword to banks, with a majority of bankers (56%) believing that regulation protects banks, while 62% believe that regulation also restricts banks in the response to fintech.

Not to be underestimated, not only does the banking industry have scale, it also has capital. According to EIU, “The banking industry has the capacity to invest and build new ventures and the staying power to weather intense competition. No wonder, then, that 95% of bankers and fintech executives believe that banks will remain in a strong position even as fintech gains ground.”

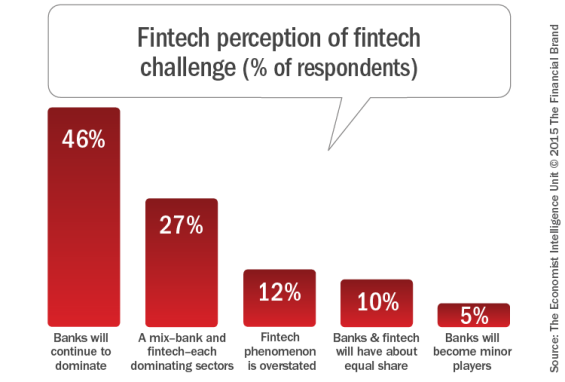

Fintech’s View of the Fintech Challenge

When fintech executives were asked about the balance between banking and fintech, it was found that fintech executives were more than twice as likely to predict that banks would continue to dominate the market (46% vs. 20%). As was the case with the banker’s self assessment, only 5% of the fintech executives believed fintech firms would dominate the market in the future.

In alignment with a survey by Silicon Valley Bank, fintech firms expect regulatory issues to be the biggest impediment to their success in the coming year. “The attendees at the Fintech Mashup event validated what fintech companies around the world have been voicing in recent years – an effective regulatory and compliance strategy is critical to their ultimate success,” said Bruce Wallace, Chief Digital Officer of SVB Financial Group.

Additional weaknesses of fintech firms voiced in the EIU study were the lack of risk management expertise, the difficulty in raising capital, inexperienced leadership and the inability to gain consumer trust or scale in a marketplace dominated by legacy banking organizations. Finally, fintech executives understand the challenge of focusing on a single product when most consumers prefer to have multiple banking needs served by a single (or small number of) financial partners.

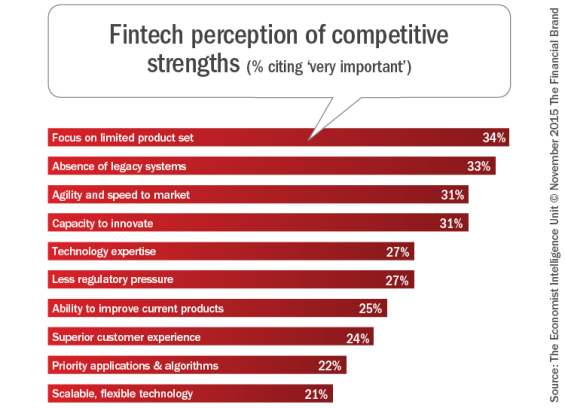

Offering a limited product set is also viewed as a strategic advantage by fintech firms that have the ability to provide a ‘category killer’ for a specific product set. Fintech firms are often able to maintain a laser-like focus on a single product, building excellence in technology as well as customer experience. Fintech firms also value their agility and capacity to innovate.

When the EIU survey explored views from fintech executives on the likely competitive balance between fintech and banks in nine retail product categories over the next five years, it was believed that banks will continue to be the dominant players in all categories. And while fintech

executives believed they will take a small share of business in every category of product initially (deposits being the most vulnerable), the exposure was expected to become more significant over time.

According to EIU, “The danger is that innovative business models take a bite out of every part of banks’ product portfolios— skimming off their best customers and driving down fees. The problem is likely to grow as tech-savvy millennials, who have little loyalty to banks, begin to take larger shares of financial assets. In their worst-case scenario, banks become commodity providers of back-office functions, with lower growth and squeezed margins”.

Banking and Fintech: A Symbiotic Relationship

The EIU asked bankers and fintech executives to assess their own strengths and weaknesses as part of the study. Interestingly, there is a strong correlation between the strengths of banks and the weaknesses of fintech, and, conversely, the strengths of Fintech and the weaknesses of banks.

The most obvious complementary factor is that fintech firms need the scale of customers that the banking industry already possesses. With a much longer tenure and scale, banking firms also have the reputation of stability and trust as well as experience navigating the myriad of regulations and compliance requirements. Lastly, the banking industry, as mentioned earlier, has the capital that is the lifeblood of any growing fintech firm.

Focusing on the weakness of banks (and correlated strength of fintech firms), the report notes that banks are severely constrained by legacy systems that can stifle innovation and the ability to be agile. Beyond the obvious challenges of working with old systems, this inhibits the ability to recruit the level of technological expertise needed to improve products.

“If I were a betting person,” Phil Heasley, CEO of ACI Worldwide told EIU, “I’d say that some really smart banks are going to survive by merging with some really smart fintech firms.“ The EIU report added, “The process could be summed up as ‘keep two cultures, but integrate the technology back office’. This solution can preserve the culture of innovation, marry it to the assets of the bank, and accelerate the combined offering to market”.

To get additional perspectives on the future of banking and fintech, we asked some members of The Financial Brand Crowdsourced Panel for their thoughts on how the transformation of the legacy banking structure and start-up fintechs might emerge. Here’s what they said.

Brett King, CEO and co-founder of Moven, bestselling author and Breaking Banks radio show host

Brett King, CEO and co-founder of Moven, bestselling author and Breaking Banks radio show host

“The banks I know all want to innovate, but silos, culture and process intransigence slow them down. Fintech partners enable banks to ‘bend space and time’ bringing change much faster and cheaper than banks could ever do internally. For fintech firms, the banks could be a great source of revenue.”

Bradley Leimer, Head of Innovation, Santander Bank, N.A

Bradley Leimer, Head of Innovation, Santander Bank, N.A

“The rise of fintech is the kick in the butt that banks needed. Banks must collaborate and learn from successful fintech startups that retain the focus that is often difficult in sprawling financial organizations with many mouths to feed. Banks are still learning how to best serve the connected customer of today. Fintech players are still learning that achieving scale can be difficult, and profitability can be even more elusive. In the end, it is a relationship that can benefit both parties – and most importantly the customer – as new ways to meet common financial needs are explored. Collaboration is the best path forward. ”

Rob Findlay, SVP of Experience Design, Singapore-based DBS Bank and the founder of Next Bank

Rob Findlay, SVP of Experience Design, Singapore-based DBS Bank and the founder of Next Bank

“I see an increasing disparity in this relationship – whilst many banks will try to ‘open’ themselves up to the ways of fintech and the startups that are creating them, the internal tensions (sometimes seperate from the enthusiasm) will make this transformation and cultural change increasingly hard, as the clock ticks by forcing banks to act quicker and with more urgency. Leadership and vision that brings everyone along for the journey is the most crucial element.”

David Brear, Chief Thinker at the international consulting firm, Think Different Group

David Brear, Chief Thinker at the international consulting firm, Think Different Group

“When looking at the impact of fintech players on banking, the main people who should be concerned are not the banks, but the suppliers to banks. What fintech firms provide, in many cases, is ‘Suppliers 2.0″ and a real alternative for banks who are facing more complexity in the market than ever. To allow banks to work with with fintech players significant changes procurement and liabilities policies. In short, the old banks and the new fintech firms working together will teach legacy organizations new tricks and remove the fear factor from fintech.”

Matt Wilcox SVP, Marketing Strategy and Innovation for the Digital Banking Group, Fiserv

“The future of banking is dependent on technology. Even the most traditional aspects of banking from deposits to loans require advancements of technology. The relationship of fintech and banking can be a perfect union to advance the industry and continues to allow banking to be a customer first industry. Many in banking see fintech as a direct threat but I believe 2016 we will see the continued evolution of these two groups working together and finding the right balance for serving customers.”

Simon Taylor, VP, Entrepreneurial Partnerships, Barclays

Simon Taylor, VP, Entrepreneurial Partnerships, Barclays

“It strikes me that everyone thinks the banks don’t want fintech and are threatened by start-ups. It’s true that banks have a lot to lose, but they also welcome efficiency and mobile-first thinking but are hamstrung by legacy regulation and processes. Innovation outside of a bank is a good thing … a learning opportunity and path to partnership that brings better experiences for customers.”

Duena Blomstrom, FinTech and Digital Experience Specialist, Duena Blomstrom Consulting

Duena Blomstrom, FinTech and Digital Experience Specialist, Duena Blomstrom Consulting

“Having spent the past few years empowering banks with fintech-built technology, l never saw the battle, being more symbiotic from my perspective. With that said, the road has been tougher for B2B fintech firms and they have remained calm as the B2C potential unicorns make the headlines. Long term, I believe the threat to banking is not from the direct-to-consumer fintech start-up propositions, but from the non-financial technology giants who are already intelligent brands that have invested in getting the customer’s heart elsewhere and will add ‘Fin’ to their ‘Tech’ at will.”

JP Nicols, President and COO of Innosect, and Co-Founder of the Bank Innovators Council

JP Nicols, President and COO of Innosect, and Co-Founder of the Bank Innovators Council

“Never has more technology been available to so many so cheaply. The growing gap is not between the haves and the have-nots, it is between the wills and will-nots. All banks have budget and regulatory hurdles to contend with, but those who truly want to stay relevant to their customers in these times of massive change are prioritizing the need to change. Very few banks globally will be leaders in product innovation, so fintech partnerships will become increasingly important. Even those that are innovation leaders are still partnering with – not to mention investing in and acquiring – earlier stage companies, just as they are in other industries.”

A Final Thought

As fintech firms grow, they will move from being a start-up to being a financial services firm with the realities of increased regulation and compliance challenges, the need for capital, scale and the expectation that innovation and new product development will continue in an agile manner. Legacy banking organizations can help with these challenges.

“The threat to banking is not from the direct-to-consumer fintech start-up propositions, but from the non-financial technology giants who are already intelligent brands that have invested in getting the customer’s heart elsewhere and will add ‘Fin’ to their ‘Tech’ at will.”

— Duena Blomstrom, FinTech and Digital Experience Specialist

As noted in the Economist Intelligence Unit report, banks and fintech firms have more business interests in common than issues that divide them. Some incumbents will up their game as fintech firms change the face of finance. Banking still has a future, but the industry will have to work harder to meet the needs of the digital consumer at a profit.

While some fintech firms and banks will choose to continue on their current paths, the potential for ‘coopetition’ is significant. In the end, the consumer will be the winner.

Download Report