Not to be mistaken for the future Isis mobile wallet (backed by AT&T, Verizon and others), the T-Mobile Mobile Money solution is the latest in a wave of neobank competitors such as Simple, Moven, GoBank and Amex’s Serve. The major difference is that this offering comes with a vast distribution network, an established customer base, significant marketing muscle and more.

When this newest banking solution was announced, some financial executives might be acting like it is the end of the world as we know it, while others may immediately fall into the trap of saying, “It’s no big deal”. The reality is probably somewhere in between. But there is cause for concern.

While this is not the same as turning smartphones into mobile wallets, it is a solution offered by a wireless provider that has distinct advantages over traditional banks and credit unions. It should be a warning to those who see this as “just a solution for the ‘underbanked’ (definition still under discussion)”. It could be much more.

In fact, in some parts of the world, mobile phones have become the de facto way for people to handle day-to-day financial transactions (as opposed to banks). The best known example would probably be Kenya’s M-PESA which is currently used by 20 million people and includes loans and savings products.

So, why should Mobile Money from T-Mobile worry U.S. bankers (in no particular order)?

1. T-Mobile Has an Established Customer Base

Unlike the majority of previous neobank entrants in the market, T-Mobile already has an established customer base to draw from. T-Mobile US provides services through its subsidiaries and operates its flagship brands, T-Mobile and MetroPCS, serving approximately 46.7 million wireless subscribers (Bank of America has 55 million customers).

T-Mobile also isn’t new to the personal finance arena. By separating the costs of wireless services and devices, T-Mobile already provides customers the option of financing smartphone purchases. According to T-Mobile, they have facilitated billions of dollars in loans for customer phones (all without charging a penny in interest).

“One of the main reasons we’re doing this is to deepen our relationship with our customers,” said T-Mobile marketing executive Andrew Sherrard.

T-Mobile’s cellular pricing strategy (cheap and with no contracts) should correlate well with the demographics they are initially trying to reach. While there are definitely mass affluent and affluent customers who use T-Mobile phones, an above average segment of their customer base probably includes customers without access to traditional financial services and who are looking for lower prices.

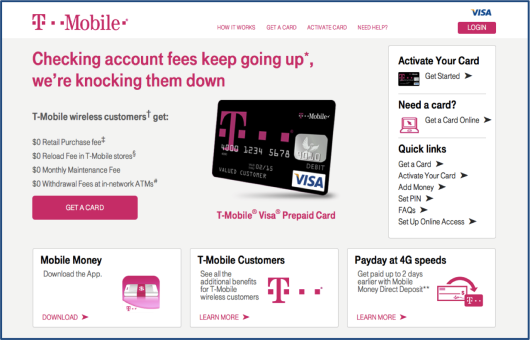

Notice in the website marketing, that the term ‘prepaid debit card’ is deemphasized in exchange for references to a checking account.

2. T-Mobile is Using a Low Cost Pricing Strategy

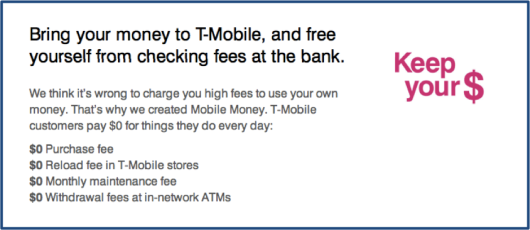

In the mobile carrier’s announcement, T-Mobile emphasized that T-Mobile customers will incur no charges for activation, monthly maintenance, in-network ATM withdrawals, minimum balances or for replacing lost or stolen cards. The company also said there are no overdraft fees.

When discussing fees on the T-Mobile Mobile Money web site, there is no reference to the term ‘prepaid debit card’ emphasizing the comparison to a checking account instead.

It should be noted that Wal-Mart offers a prepaid card with virtually no fees as well, but charges $3 to cash checks up to $1,000 in its stores. T-Mobile’s service does take a fee of 1 percent of the value of government or payroll checks and 4 percent of the value of all other checks, making T-Mobile more expensive for any check over $300 and for personal checks over $75 (these fees are not easy to find on the site or promotion).

A non-T-Mobile customer can sign up for Mobile Money, but would have to pay significantly more traditional fees (allowing for a wireless sales opportunity).

Taking a consumerism positioning (much like has been done by GoBank, Moven, Simple and Bluebird, a comparison to current fees was made today at the introduction of the new product. According to Mike Sievert, chief marketing officer of T-Mobile:

“It’s ridiculous that families, especially those who can least afford it, have to pay so much for basic check cashing services that many of us take for granted. Mobile Money levels the playing field to put money back in consumers’ pockets for important things – like bills, groceries or vacations. The typical household using a check casher to cash their paychecks could save about $1,500 per year, and customers tired of getting hit with overdraft fees can switch and save an average of $225 a year”.

While the T-Mobile offering may take a while to gain traction (since consumers hate to transfer accounts), the emphasis on price, easy availability, mobile functionality, etc. will definitely make customers of all financial institutions aware of what is available in the marketplace. This could put pressure on revenues and require a ramping up of mobile banking innovation.

3. T-Mobile Understands Mobile Money

T-Mobile’s Mobile Money has inked a deal with The Bancorp similar to its other private-label banking arrangements (including one done with Simple). The deal has The Bancorp using its bank charter to support T-Mobile’s new Mobile Money service that the company introduced. Like done with Simple, the agreement centers on a Visa prepaid card issued by The Bancorp and produced by Blackhawk Network Inc. but the Mobile Money product itself is definitely mobile-first.

It is assumed that the back office operations would be similar to what has been associated with Simple, eliminating much of the early testing and trial and error done by Simple and other earlier entrants. In addition, unlike the majority of the neobanks, T-Mobile made no mention of ‘waiting lists’ or a staged introduction.

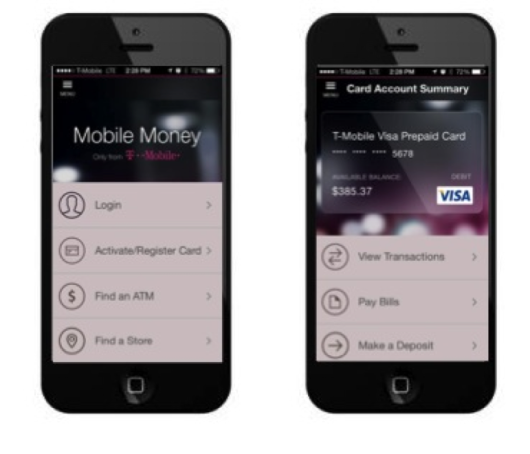

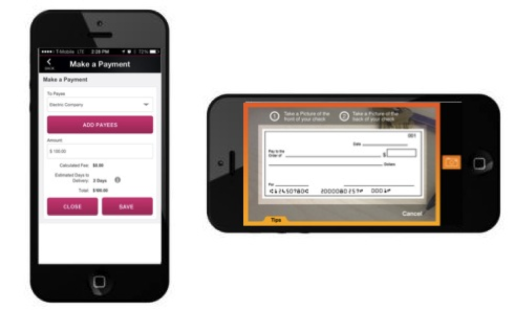

As mentioned, in addition to the debit card, a customer can use their new Mobile Money app on an iPhone or Android smartphone to take photos of checks, make a deposit into an account, pay bills, add funds, view transactions, transfer funds, and find ATMs.

While there doesn’t appear to be any ability to search or sort transactions, budget or access a ‘safe-to-spend’ functionality at this time, the app still appears to have the simplicity in design and ease of use associated with a neobank offering.

Some of the available screen shots appear below:

A drawback to T-Mobile’s service at this time is that it only lets you send money to other T-Mobile card holders and you’ll need to know their phone number and last four digits of their card number. While this may change in the future, it does limit the functionality compared to traditional banks.

4. T-Mobile Is An Aggressive Marketer

T-Mobile is anything but a wallflower in the mobile industry, so we should expect nothing less as they enter financial services. Known for their cheap rates, lack of binding contracts and aggressive marketing, even today’s press release took on the highly competitive personality of T-Mobile’s president and chief executive office, John Legere.

In fact, the headline of the press release read, “T-Mobile Frees Consumers From Outrageous Check Cashing Fees With Innovative New Smartphone Solution”. A favorite quote from Mr. Legere in the press release was:

“We’ve already transformed how Americans use and pay for phones, tablets and wireless service; why stop there? Millions of Americans pay outrageous fees to check cashers, payday lenders and other predatory businesses – just for the right to use their own money. Mobile Money shifts the balance of power for T-Mobile customers and keeps more money in their pockets”.

Not only should bankers expect a no holds barred, in your face, marketing campaign emphasizing T-Mobile’s ‘Un-Carrier’ (or Un-Bank) theme and positioning banks as villains, we should expect a lot of money being allocated to this newest expansion of T-Mobile’s business model. This is because success with their Mobile Money solution can expand their cellular customer base and can also position them advantageously for a future with Isis.

Finally, and potentially most important, T-Mobile owns a marketing channel … the phone. They have the ability to reach their entire customer base at a very low cost through the phones their customers already carry. While they need to be careful about any outbound effort, strong linked video content can help with the marketing efforts either through text or email messages.

5. T-Mobile Has A Physical Distribution Network

It is believed that many of the innovators in the mobile and prepaid space could be negatively impacted by the lack of a physical distribution network. While several may argue that physical presence should not be a major concern for a mobile-first offering, the fact that Mobile Money from T-Mobile is supported by a fee-free ATM network of more than 42,000 machines (compared to 18,000 Bank of America machines) and from 70,000 points of distribution (Bank of America has 6,100 offices) can’t hurt.

Interestingly, while T-Mobile is making a big deal about their ATM network, Simple actually has more locations, with 55,000 Allpoint ATMs, the country’s largest surcharge-free network.

T-Mobile customers can take out cash through retailers, just like customers can now do with any bank debit card and can reload their account at any retailer that supports Reloadit, MoneyGram and Visa ReadyLink as well as at any T-Mobile store or at Safeway markets (other locations will become available).

6. Mobile Money Is Not Just For The Underbanked

Let’s not lull ourselves into a state of complacency. While the format of the service offered by T-Mobile is structured as a prepaid card, customers who sign up for Mobile Money are essentially getting a traditional checking account.

Customers can have money deposited directly to their Mobile Money account or deposit checks by taking a picture with their smartphone. Mobile Money customers also get a Visa debit card that they can use to make purchases, pay bills or withdraw cash from a network of 42,000 ATMs scattered throughout the nation.

In other words, while the talk initially is that the product is for those who have been ‘left behind by the banking system’, the reality is that the target audience could expand well beyond it’s already surprisingly large ‘underbanked’ base to include the digital natives that every bank wants to serve.

In an interview with John Adams from PaymentsSource’s, Gareth Lodge, a senior analyst at Celent’s banking group stated, “The U.S., for a country of its level of development, has a pretty high level of underbanking,” Lodge says, adding the U.S. has an unbanked population of about 12%, compared to about 3% in the U.K. “When you add in the underbanked, the number for the U.S. is estimated to be nearly to 30%”.

That said, T-Mobile noted that they did a pilot in Miami and saw better-than-expected success beyond the original target audience. While it was assumed prepaid customers would primarily be interested in Mobile Money, they were surprised to see 40 percent of the users were more credit-worthy post-paid customers.

How does a traditional bank open the doors to let the ‘lower third’ of their customers leave without having a large number of digital customers leave with them?

7. Timing

Finally, T-Mobile’s timing comes when trust in traditional banks is still low, consumers are becoming more digital and comfortable with their mobile devices, and when more and more innovators in the financial services space are finding better ways to do basic banking.

Companies like Square, PayPal, Google, the neobanks mentioned above and others have benefitted from banks and credit unions falling asleep at the wheel. As long as innovation and product development within traditional banks continues to lag, and there is a market for simplification and improved utilization of new technologies, more entrants will emerge nipping at the edges of what was once the domain of rather staid banks and credit unions.

Unfortunately, while many of these entrants were not considered formidable enough to capture the ‘best’ customers, some believe the proverbial horse is out of the barn and it may be difficult to reign the positioning of trusted financial advisor back again with many households. And, how easy will it be to win back customers lost to mobile-first players when a traditional bank’s offering doesn’t look or function the way a neobank’s mobile banking does.

Note: If you want to ‘kick the tires’ of the new T-Mobile Mobile Money prepaid product, they are already available in participating T-Mobile retail locations and online. They are also be available in Safeway stores in the United States.