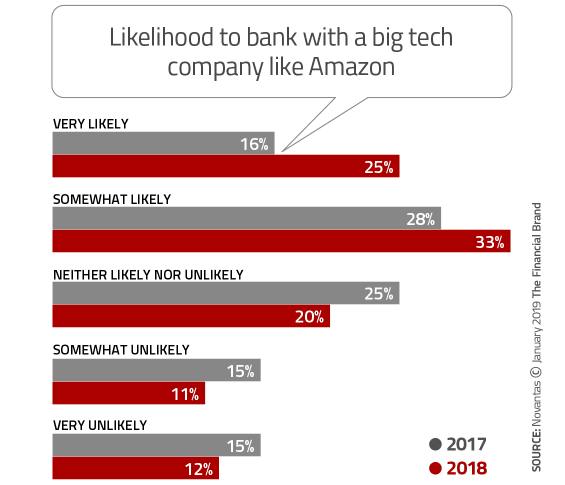

According to a report from Novantas, 58% of potential switchers — those consumers who are looking to move to a new primary financial institution or would consider doing so — are open to alternate providers like Amazon, Facebook, Apple, or Google. That finding represents a startling 14-point increase over the 2017 survey.

“Many U.S. banks are currently facing the same conundrum: how to position themselves to acquire at least their fair share of new customers while continuing to appeal to — and not alienate — their current customer base,” Novantas said in their report, stressing urgency as banking providers seek answers to these challenges.

Part of the problem, according to Novantas, is that financial marketers overestimate the differences between generations, causing many banks and credit unions to drag their feet. Traditional institutions seem to think they can take their time responding to consumers’ digital preferences, assuming that older consumers are in no rush and will stick around. They are sorely mistaken.

In its study, Novantas classified those who have switched banking providers in the last few months as “recent purchasers”. In the survey, nearly two-thirds of these switchers were either Millennials (47%) or Gen Z (15%). But one in five (20%) were Boomers, and an equal number were Gen X.

Traditionally checking accounts formed the core of every banking relationship, and financial marketers regarded them as the most critical piece of the puzzle because they tend to be very sticky. But some direct banks have built themselves — at least initially — on savings deposits, which presents potential risks for traditional banking providers. The report warns that direct banks can use the beachhead they’ve established with savings deposits to cross-sell into transaction accounts. Indeed, about one in three of those who had opened a new transaction account with a direct bank had a savings relationship with that institution beforehand.

This has broader implications than just “Bank vs. Bank”, however. Novantas’ research found that consumers who currently have their primary relationship with a national bank or a direct bank find the idea of opening an account with a non-bank tech firm like Amazon more appealing than do people banking with regionals, community banks, and credit unions. It seems that those who don’t mind the impersonal “take-a-number” approach often associated with megabanks would be just find dealing with a faceless bigtech banking providers, while consumers that value personal service — those banking at smaller institutions — are less receptive to the idea.

However, the report concludes that anyone opening a new account could be easily enticed by such new — and still hypothetical — players. Nearly six out of ten prospective switchers say they would likely go for a tech firm’s account if offered the chance.

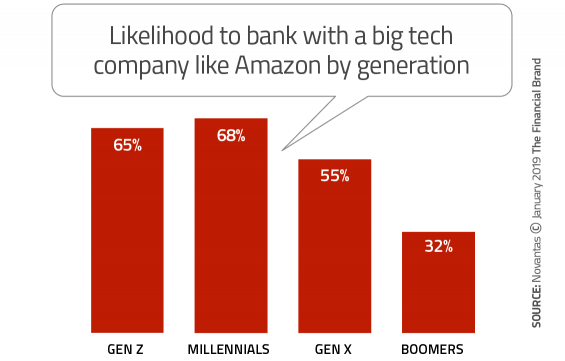

These trends should be more worrisome for smaller institutions, where the generational tendency skews towards older consumers. While Millennials and Gen Z are more likely to move to a tech provider, over half of Gen X says they’d move — and even nearly a third of Boomers would.

The attraction of “the new cool thing” among consumers who increasingly live, work and shop online can’t be underestimated. Research by Epsilon/Conversant found that 67% of online shoppers consider Amazon to be the country’s most innovative retailer — and 78% of Prime consumers do.

Matthew Sharp, VP/Head of Customer Knowledge at Novantas, makes the point that the survey found that many traditional institutions lack any differentiation from others, and that direct banks generally score higher among consumers for being unique or otherwise differentiated from traditional players. That said, Sharp adds that direct banks have their own challenges coming in that regard, with ecommerce players in the wings.

While many consumers — particularly younger ones — see potential new competitors in the banking space as a conflict pitched between traditional providers and disruptors, the battle lines are blurring. The stark contrasts that separated the two camps — digital/new vs. offline/traditional — are fading. For instance, Novantas points out that larger banks are hooking into smart speakers like Amazon’s Alexa, while Amazon and other ecommerce leaders opening physical locations and exploring brick-and-mortar strategies. Even as rumors of an “Amazon Bank” continue to swirl, it’s just as likely that Amazon forges partnerships with traditional providers.

Read More: ‘Amazon Bank’ Is Already Here, Without a Charter or Regulatory Approval

Omnichannel Banking Strategies: A Generational Tug of War

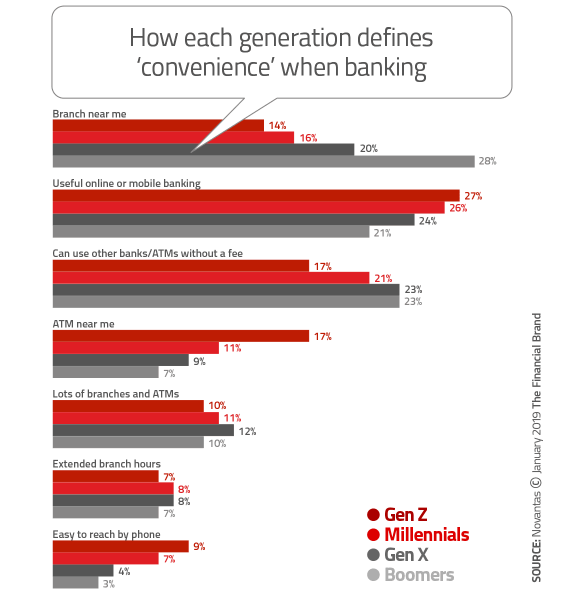

The survey confirmed that two older generations — Gen X and Boomers — still put branches at the top of their convenience pyramid. Novantas also notes that regional banks typically have a higher-than-average number of consumers born before 1980.

Despite a preference among older generations for branches, consumers overall are doing less and less in them. Nevertheless, continuing to serve these consumers means maintaining investments in branch networks and other physical aspects of banking, which is costly and ties up assets.

Part of branches’ appeal is people, a fact not lost on financial marketers who frequently talk about the quality of their service. However, the Novantas report points that even though consumers agree that “bank employees are generally pleasant to work with, the attribute ranks relatively low on overall importance.”

According to Sharp, these findings support the “thin branch” model that some larger institutions have been rolling out in select markets. Of course, many banks and credit unions have been shrinking the branch footprints of their existing networks, and most industry observers agree that the days of huge teller counters and massive drive-up bays are over.

Sharp also says the changing market dynamics in the banking sector could be particularly troublesome for regional banks. “Regionals tend to be a little bit of everything to everybody,” he explains. Sharp says regionals could find themselves caught between the scale of megabanks and the quaint, hyper-local model of community institutions. After all, regional banks have to maintain large, costly branch networks and have slick digital banking tools.

Make Switching Easy With Digital Account Opening (That Works)

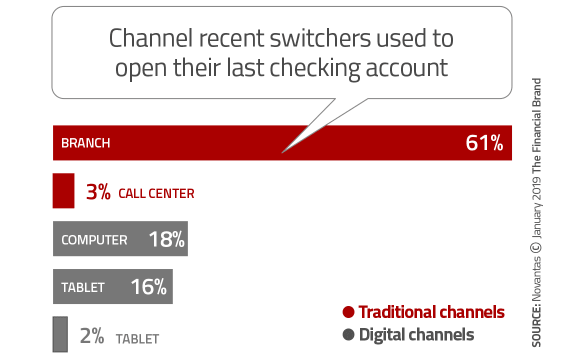

Over half of all prospective switchers say they want to open their next primary checking account digitally. And yet a significant number of respondents in the Novantas study said they were unhappy that they couldn’t complete the account opening process without jumping from digital to brick-and-mortar channels.

While 35% of switchers said that they had started opening their current primary checking account digitally, only a quarter (27%) completed the process completely on their computer, tablet, or smart phone.

Digital opening is becoming a “must-have” and branches that survive will need to be repurposed, according to Novantas. “It will be critical for banks to rev up the digital sales channel in order to achieve acquisition success moving forward,” says the report.