Despite all of the advancements made by the banking industry in providing access to savings, borrowing and investment options through physical and digital channels, the vast majority of consumers continue to feel insecure in their ability to adequately manage their finances. The need goes far beyond post-transaction alerts and pretty graphs. There is a significant need to provide financial wellness tools that include aggregation services, proactive financial recommendations, security and self-service solutions.

As consumer awareness of what is possible with the application of data, advanced analytics and digital technologies increases, so does the demand for more sophisticated financial management tools based on these capabilities. According to consumer research conducted by The Harris Poll on behalf of Fiserv, many consumers struggle with managing their finances and look to their primary financial organizations for help. As is the case with digital banking overall, they want solutions that make money management easier, faster and more secure.

Some of the highlights from the quarterly survey include:

- Consumers are worried about their financial health across virtually all demographic segments. For many, this may mean living paycheck to paycheck … or worse.

- Unsatisfied with offerings from their primary financial institution, most consumers rely on a hodgepodge of paper and digital tools, from monthly statements to electronic tracking tools available online and on mobile devices. There is a need for better options that are real-time, consolidated and easy to use.

- Security options top the list of desired tools for managing finances and protecting identity.

- As consumers become more aware and comfortable with digital apps across industries, they are more comfortable with digital banking solutions, opening the door for organizations that can provide integrated financial wellness applications.

The question is, will banks and credit unions respond to these needs? According to Matt Wilcox, senior vice president of marketing strategy and innovation at Fiserv, “Consumers now expect more from financial institutions. Beyond core banking services consumers are beginning to expect tools to manage their finances. This creates a tremendous opportunity for financial institutions to become a trusted advisor for consumers, creating services centered on helping consumers with their financial wellness and not just their core banking services. Financial institutions have an opportunity to leverage data and the integration of their channel applications to provide a comprehensive financial management solutions for their consumers.”

Consumers Concerned About Financial Health

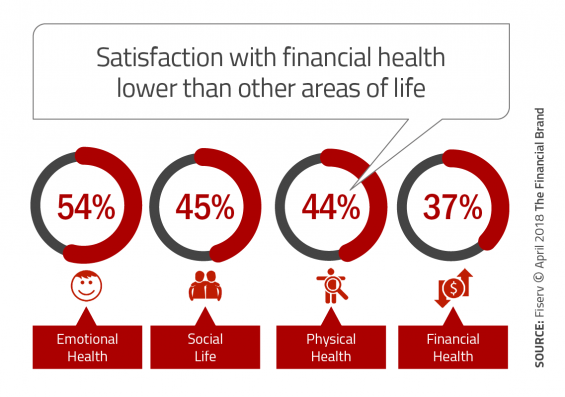

It comes as no surprise that consumers are concerned about their financial health. What may be a surprise is that satisfaction with financial health is lower than physical health, social life and emotional health.

In fact, only 37% of consumers said they were satisfied with their financial health according to the Fiserv research. While consumers with higher incomes and more assets were more comfortable with their financial wellness, 38% of consumers (50% 0f Millennials) would find it difficult – or impossible – to pay back a loan of $500.

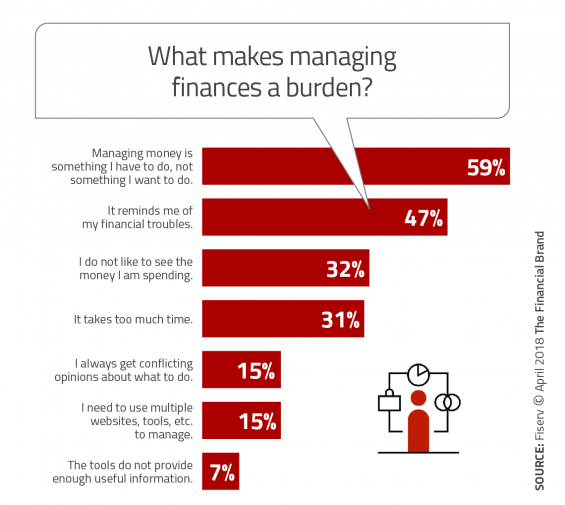

Of the 30% of consumers who think managing their finances is a burden, more than half (59%) perceive the task as an obligation and 47% say it is a reminder of the financial challenges they face. When asked about the burden of managing finances, Millennials were much more likely to feel managing money ‘is a pain’ despite significantly less complex finances.

This was also true for urban consumers (compared to suburban and rural consumers). One of the reasons for this higher stress level was because of a much higher incidence of conflicting opinions being offered.

For financial services organizations, both the concern about finances, and the reasons for feeling managing money is a burden, provide a great opportunity to create and aggressively promote easy-to-use financial wellness tools that can help take the guesswork and fear out of money management. These tools may be as simple as a savings tool to build emergency funds, to financial management educational videos specifically geared to Millennials – created for mobile viewing. Going a step further, the videos can be personalized to a consumers current financial relationships.

Consumers Want Multichannel Solutions

As with the way consumers access banking accounts today, there is a desire to use all channels available to better understand and manage financial wellness. Most consumers still prefer the branch for more complex interactions, while there has been a significant increase in the use of online channels and even mobile when friction is minimized and engagement is easy.

Consumers want features such as account consolidation, real-time access, alerts and mobile or browser apps. Most importantly, people want insight regarding their finances and financial management tools easily accessible in one place … on demand. The Fiserv research found that 34% of consumers wanted the ability to manage all their financial accounts in a single online location or app, with 33% wanting real-time access and 28% wanted alerts regarding bills that are due and money available to spend.

Aligned with the digital channel use of Millennials, the desire for a centralized online or mobile app to manage finances increased to 48% for this segment. This strong desire indicates the stress felt by this segment as well as the belief that such a capability does not exist currently. While some organizations already provide digital tools, most do not actively promote these solutions to the audience that would benefit the most.

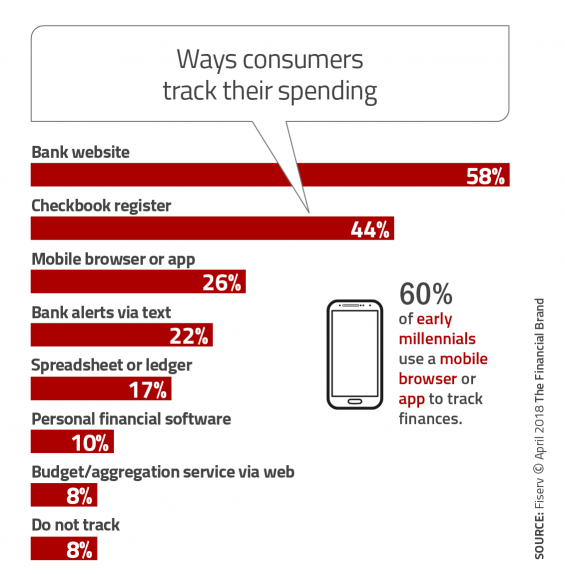

The survey found that 60% of early Millennials already rely on a mobile browser of app to track finances (more than double the marketplace as a whole). It is not just Millennials who are shifting channel use for tracking finances. Overall, the use of traditional offline tools (like checkbooks) have decreased, while the use of mobile browsers or apps are increasing. It should be remembered that ‘tracking’ finances is a bare minimum for personal financial management.

Transaction Alerts Fail to Reach Potential

More and more consumers rely on SMS alerts to inform them about package deliveries, limited time offers from retailers, and even weather emergencies. Despite the power of this tool, only 64% of consumers surveyed indicated that they currently receive transaction alerts on their debit or credit card. Security is the primary reason consumers opt-in for alerts, despite the opportunity to use alerts for a much broader array of financial management purposes.

A sense of security (67%) and previous fraud (43%) are the most common reasons for using transaction alerts, while a third of consumers (33%) cited it as a convenient way to manage transactions.

Managing transactions is one of the primary benefits provided by new digital-only banks as is the ability to provide budgeting and forecasting insights – via alerts – in real-time, based on current and past behavior. Many of these digital banks also allow real-time categorization of transactions, social sharing and an immediate view of monthly trends with a single touch of the screen.

While it is valuable that 43% of consumers have caught fraud due to an alert received, the ability to use alerts for managing finances has vast untapped potential for traditional financial institutions. Beyond negative warnings, these alerts can also provide offers or solutions that can improve a person’s financial health.

Security and Money Management Tools Highly Desired

When surveyed about financial management tools, consumers put security and privacy solutions at the top of their list. This is not surprising since identity theft has become more prevalent and represents one of the ‘uncontrollable’ components of financial wellness.

The research found that 66% of consumers want to see additional tools to safeguard mobile activity. Slightly more than half (56%) are interested in biometrics which is a slight increase from the survey done in 2016. Interestingly, 38% of seniors are interested in biometric solutions to protect their identity.

Potentially indicating both the lack of adequate solutions already available in the marketplace and the trend towards self-service, roughly half of consumers surveyed want self-service capabilities on their mobile device (81% of Millennials indicated the desire for self-service mobile solutions). More than 4 in 10 consumers also want the ability to aggregate account details from multiple financial institutions in a single app (including two-thirds of Millennials).

Using AI and Digital Tech to Deliver Financial Wellness Tools

There is no lack of information in the marketplace to help consumers make better financial decisions, yet the volume of advice – and lack of easy access – makes consumers frustrated and increasingly frightened about their financial wellness. Unfortunately, most tools currently offered by traditional financial services organizations are limited in scope, static in their perspective and focused on past behavior rather than future risks and opportunities.

Consumers are not looking for budgeting tools that require manual input, ongoing management and lack advice as to what actions to financial health. Banks and credit unions now have AI-powered solutions available that can leverage account insights, demographic information, financial goals, stated or inferred behaviors and preferences, credit history, etc. These can be combined with real time market and transaction data to provide recommendations that get smarter over time.

Instead of cumbersome and time consuming budgeting tools, AI-based solutions can create personalized experiences and targeted financial advice that is contextual – in real-time. At a time when there is premium placed on time-saving solutions that improve a consumer’s lifestyle, the market potential for being a leader in delivering digital financial management tools has never been greater.