If all chatbots were as successful as Bank of America’s Erica, which has about 19.5 million users, they would be a dominant channel. But so far, they’re not.

Chatbot usage in banking is rising, to be sure — accelerated, like all digital banking applications, by the pandemic. But satisfaction, according to two studies, is not stellar, and, in some cases, may be doing more harm than good.

Some would argue there’s a big difference between “chatbots” and “conversational AI” — the latter being the term for apps that use natural language processing, a subset of artificial intelligence. And, indeed, BofA calls Erica a “virtual financial assistant,” not a chatbot. Although that may be more marketing than science.

Wayne Butterfield, Director at research and advisory firm ISG Automation, says bankers should think of conversational AI as the science behind automated support and chatbots as the tool to deliver it. Whether based on voice or text, chatbots are ultimately tied to a structured database with topics, questions or answers that support a conversation with an end-user.

Solution to an Urgent Need

Chatbots aren’t new in banking. Ally was one of the first banks to introduce chatbots with the launch of Ally Assistant in 2015. It works with the bank’s mobile app and enables customers to make payments, transfers, P2P transactions, and deposits. Other banks such as USAA and Capital One, with Eno, have released chatbots.

As the technology has improved and become more widely available these tools have gained more adoption. But as of early 2020, pre-pandemic, the number of financial institutions that had deployed chatbots had only risen from 4% to 13%, according to Cornerstone Advisors research. 16% of the institutions in that survey said they planned to invest in chatbots in 2021.

While those are not earth-shaking numbers, they do demonstrate forward momentum in chatbot adoption. The pandemic gave that a boost as more banks and credit unions turned to chatbots as they were forced to shutter or sharply restrict call center operations in the early months of the pandemic. Financial institutions that needed quick ways to reduce call center labor and address basic questions adopted chatbots to respond to basic customer inquiries, Butterfield tells The Financial Brand. Several chatbot vendors offered fast-track setup to meet the demand.

While many financial institutions tend to view chatbots as instruments of customer service, they have many more applications ranging from training tools to helping in onboarding and even security.

“We’ve come to assume chatbots are for customer service, but it’s not limited to that. The potential use cases are infinite,” says Ron Shevlin, Managing Director of Fintech Research at Cornerstone Advisors.

Read More:

- True Conversational AI Solutions Eluding Financial Institutions

- 4 Reasons Why Your Financial Institution’s Chatbot Project Failed

It’s About the Quality of the Conversation

With all the recent growth — actual and potential — are these digital-age tools making the grade?

“It’s all about the quality of delivery,” says Shevlin, in an interview. “There are actually some chatbot-type applications that do a good job of fooling people into thinking they are talking to another human.” Chatbots can respond by text, email or voice, depending on the technology used and the institution’s preference. Based on comments from several institutions using chatbots most responses tend to be by text.

Many financial institutions try to point consumers to use chatbots instead of calling a live agent, Butterfield notes. This will help drive many basic requests — like checking account balance inquiries and changes of address — to more efficient automated systems.

Yet chatbots do have limitations and can backfire if they’re poorly designed or implemented. Connections go down, people speak in unique manners, and sometimes the chatbots can’t understand them, whether text-based or voice.

GoMoxie, a provider of live-chat platforms, found in a survey of 1,000 banking customers that 60% have an unfavorable view of chatbots and don’t trust them. A third of this group said chatbots didn’t help in answering their questions.

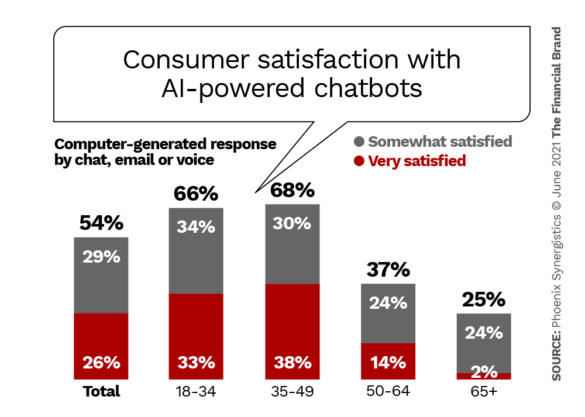

Similar results came from research firm Phoenix Synergistics. In an early 2021 study it found that compared with 66% of banking customers who said they were very satisfied with live-chat technology (in which consumers text with a human versus a bot), only 26% of consumers using AI-powered chatbots said they were very satisfied.

Phoenix Synergistics did differentiate in its questionnaire between chatbots and virtual assistants, and the responses for the latter were higher, with 62% of consumers saying they were very satisfied with their experience.

Some common reasons for poor experiences with a chatbot are:

- The problem isn’t on the list presented.

- It’s challenging to get connected to a live representative.

- The service doesn’t understand them and provide the information they need.

Sobering Truth:

The kiss of death for a chatbot is when it leads a customer in a circle of frustration with no ability for a human agent to intervene when there’s a problem.

“There’s nothing more frustrating than an automated service that doesn’t give you what you want,” Butterfield states.

Read More:

- Chatbots and Cafés: How Capital One Balances Digital, Physical Banking

- Why Contact Centers Are a Key Part of a Human+Digital Banking Strategy

- What Consumers Actually Want From Their Bank’s Mobile App

The Key: Support the Bots with People and Processes

Chatbots that don’t meet the bar for customer service expectations are usually hampered by people and processes, not the technology, Shevlin observes. “This isn’t a technology problem. It’s the policies and procedures the institution puts into place around it. The option to instantly connect with a human being can resolve many of these issues,” says Shevlin.

“If you are bot-only, you are doomed to fail. You must design people into the process.”

— Wayne Butterfield, ISG Automation

There are several key considerations to ensure chatbots are successful.

First, the financial institution needs to build the entire technology around the customer experience, says Butterfield, not cost reductions and operations.

Second, the bank or credit union must be upfront about what the chatbot can do and ensure customers are only being directed to it for the right reason.

Finally, Butterfield agrees with Shevlin: The chatbot should always offer an option for a customer to quickly reach a human when there is a problem.

“If you are bot-only, you are doomed to fail. The technology isn’t clever enough to think outside of the box, it has a process, and anything outside of that will frustrate customers,” says Butterfield. “It comes down to design, you must design people into the process.”