Mobile banking overall has rapidly become its own ecosystem in some financial institutions, with the sheer range of functions possible to execute on mobile devices growing from year to year.

As an Insider Intelligence study demonstrates, in 2020 consumers indicated that they actually found mobile banking availability a more important factor in picking a financial institution than having a branch near them — by more than 13 percentage points.

While much of mobile banking is all-digital, there are three points where mobile apps and digital wallets intersect the physical world: contactless payment at point of sale, contactless access at ATMs, and mobile check deposit. The latter, while a link with the past in many ways, remains a critical factor.

Why This Is Important:

In spite of digitization of payments on many fronts, two out of five consumers deposit paper checks with their smartphone or tablet. 42% did so for the first time in 2020 — and most intend to keep using mobile capture.

The latest edition of “Mobile Deposit Benchmark Report,” by Cornerstone Advisors and Mitek, from which the figures above are drawn, calls mobile deposit service “a critical determinant of consumers’ satisfaction with their banks’ and credit unions’ mobile banking capability — and their overall satisfaction with those institutions.”

In fact, an early 2021 consumer study by Ipsos and Forbes Advisor found that mobile deposit ranked as the most important aspect of mobile banking when consumers were asked to give their top three choices.

The Cornerstone-Mitek study makes a critical point about mobile deposit service that can get lost in the bells and whistles of technology: The user experience and design elements of mobile deposit remain very important. But equally important are the policies and rules behind the service.

The emphasis from one year of the study to the next has shifted back and forth, according to Ron Shevlin, Director of Research at Cornerstone Advisors. Part of the study is based on consumer research and the other is based on Cornerstone’s evaluation of specific financial institution mobile deposit services, performed in conjunction with CI&T, a digital strategy and design agency.

“The key point is that, despite the increased adoption of mobile deposit and its importance to mobile banking users, financial institutions shouldn’t become complacent about improving their mobile deposit capabilities,” Shevlin writes. “If anything, banks and credit unions should be doubling down on making their mobile deposit experience a world-class capability.”

Read More: Mobile Banking Apps Failing in Key Areas of CX

What Troubles Consumers About Mobile Deposit Service?

Among the consumers surveyed, 29% said mobile capture is critically needed and 41% consider it important. In fact, two out of five consumers surveyed by Cornerstone say they would use mobile deposit more frequently if the technology could be made easier to use.

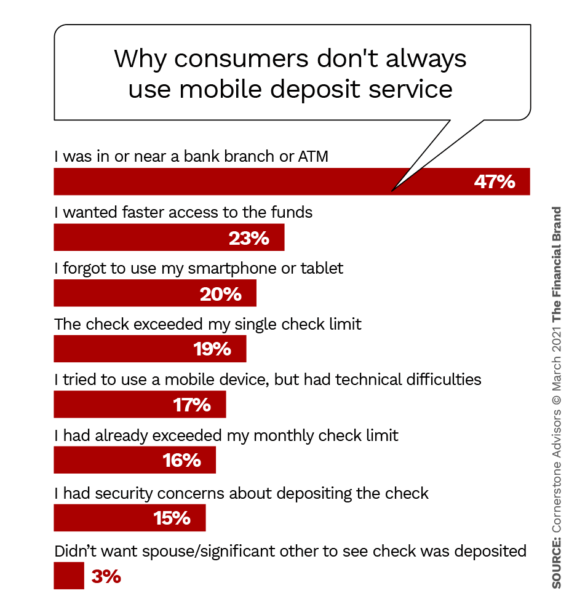

What keeps people from making even more use of mobile deposit? The chart below illustrates that nearly half of those surveyed say they were near an ATM or branch, so they made the deposit there. And almost one in four consumers want faster access to their funds than their financial institution’s mobile deposit policies permit. Yet other reasons point to policy or security concerns.

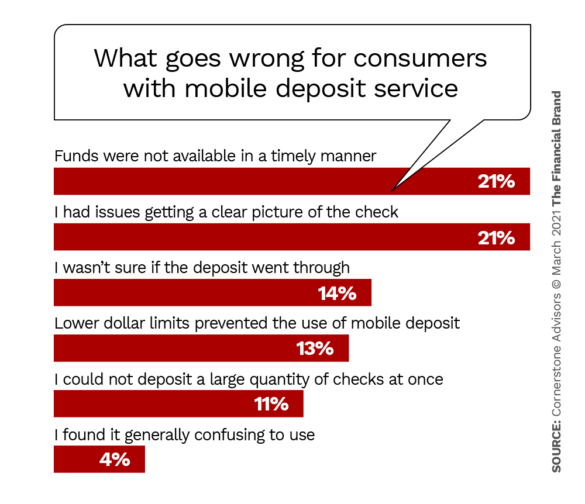

The survey also asked consumers what specific problems they had encountered with mobile deposit. All of them, the report points out, hinge on policy decisions, technical issues, and user experience and design factors — all ultimately within the institution’s control.

Consumers were asked what would get them to deposit more checks with mobile deposit:

- Faster access to cash 52%

- Better ease of use 41%

- Assurance that the check was deposited 29%

- Higher deposit limits 25%

- Improved app security features such as touch ID 19%

Read More:

- Mobile Banking: Financial Institutions Must Clean Up Their Apps

- The Good and Bad (and Ugly) of Big Banks’ Mobile Sales Experience

Lessons To Take From Cornerstone’s Mobile Deposit Rankings

The other part of the Cornerstone-Mitek study is based on live evaluations of deposit accounts for each of the 20 financial institutions examined. The mobile deposit service for each institution was rated based on a framework developed by CI&T. This included a review of policies, which was based on a combination of in-app information, answers from customer service agents, and institutions’ websites.

The top ten institutions, from leader U.S. Bank down, were as follows; the full report ranks 20 large banks:

- U.S. Bank

- JPMorgan Chase

- Fifth Third

- SunTrust (which is now part of Truist)

- Capital One

- Bank of America

- Wells Fargo

- Citibank

- BB&T (which is now part of Truist)

- Santander & BBVA (a tie)

Institutions have moved up and down the rankings over the five years the study has been conducted. The report remarks at length about how U.S. Bank steadily climbed up the rankings as it made improvements.

“The app has evolved so much over the years that it honestly looks like a completely new product — one that is bold, clear and extremely well done,” the report says. The report praised its higher deposit limits, reduced check hold times, and “keen design awareness.”

A Timely Feature:

During the pandemic U.S. Bank added a special button to its mobile app to flag deposits of federal stimulus and tax refund checks. Those don’t count against the bank’s mobile limits.

Overall, “the leaders in the rankings focus on simple UX design and confidence-boosting policies on both limits and short check-retention time of only two days,” the report states. “Financial institutions toward the bottom of the list, however, typically suffered from too much text, a cluttered user interface, and the inability to access tips or help throughout the mobile deposit process.”

The report features a four-page rundown on researchers’ evaluation standards, which makes a good tool for other institutions to perform self-evaluations.

Another Helpful Feature :

A graphical device used by only a few institutions but that evaluators commended is a check capture progress bar.

On the other hand, some institutions took a drubbing for photo functions that resulted in skewed images, confusing typefaces and messages that could sometimes cause depositors worries. Some institutions simply failed to keep pace with the improvements other institutions were making and lagged.

Additional observations from among the institutions ranked:

- Fifth Third: The report points out that the evaluators admired its app’s look and feel, especially its “crisp and clean” display that avoids cluttered text and icons. However, the bank was pulled down by policies. It cut check hold time to five days from 14, but “while that is a good reduction, five is still considered too long.” [Hold times in this context refers to how long a consumer must hold onto scanned checks before destroying them.]

- Capital One was rated highly in part because of the clear process for depositing checks, and the quality of its animated tutorial on how to make mobile deposits. Also setting the bank apart are alerts sent after a deposit is completed.

- Bank of America received points for a function allowing users to keep digital copies of checks within the app for future reference. “This is a unique feature that we have not seen in many competitors’ apps.”

- BB&T moved up in part because it chopped a 30-day check hold period to seven days. “Still not the best, but a world apart from its previous recommendation.”

- Citizens was among institutions commended for higher-than-typical maximums on checks deposited by mobile capture. It has a $20,000 personal monthly limit. However, the evaluators took off points for the bank’s ten-day hold period.