With all of the conversation about the importance of a strong digital banking experience, banking executives may assume that the banks that are considered best-in-class by Forbes would also have the best digital platforms. This correlation would make sense if that was all that it took to be considered a standout organization. Unfortunately, it is never that easy.

While a digital banking experience is definitely important, it isn’t the only criteria a consumer considers or the only criteria that should be considered by industry observers. Consumers who already have an established relationship with an organization, or those who rely on more than just the digital channel to transact business will obviously consider other criteria.

For Forbes, the ‘America’s Best Banks 2018‘ ranking criteria included ten metrics related to growth, profitability, capital adequacy and asset quality. Metrics included return on average tangible equity, return on average assets, net interest margin, efficiency ratio and net charge-offs as a percent of total loans. Forbes also factored in nonperforming assets as a percent of assets, risk-based capital ratio and reserves as a percent of nonperforming assets. Finally, they also consider the all important operating revenue growth.

So, how strong is the correlation between digital experience and ‘best bank’ rankings? Which organizations do the best delivering digital experiences? Most importantly, how far does the banking industry still need to go with their digital banking delivery?

The 27-page ‘Best Digital Experiences in Banking 2018’ report from digital strategy and design agency Extractable hoped to answer some of these questions. Their work with more than 100 financial services organizations was used to build the template for the research. Their heuristic review of the user experience of the top 50 U.S. banks looked at these 6 key areas:

- Digital User Experience

- Analytics and SEO

- Key Digital Features and Functionality

- Visual Design and Branding

- Digital Content

- Digital Marketing

Being a ‘Best Bank’ Means Having the ‘Best Overall Experience’

In an effort to determine the correlation between the ‘best banks’ as ranked by Forbes and the digital banking experiences delivered by these organizations, Extractable specialists in user experience (UX), design, and analytics conducted a high-level review of the retail banking sites of the top 50 organizations.

They scored the organizations from 1 (poor) to 5 (most innovative) based on the best practices in the 6 categories listed above. A score of ‘4’ was still considered ‘exceptional’ by the evaluation team. These scores included both quantitative and qualitative criteria during a narrow snapshot in time, since the marketplace dynamics change almost every day.

Interestingly, there is not a strong correlation between ‘best banks’ and ‘best digital experiences’ overall. In fact, the top five best digital experiences overall were from institutions that were ranked in the 40s or 50s by Forbes (still very good banks). Instead, the top overall digital experiences were from organizations that have made significant investment in the digital channel or are organizations publicly committed to a strong customer experience in all channels … or both.

Of concern is the reality that all of the top performing organizations hovered just a bit above or below the ‘good’ score of 3. In addition, the industry average for the rest of the 50 top banks was just a bit better than ‘fair’. There is obviously a lot of work still to be done by all banking institutions.

According to Craig McLaughlin, CEO of Extractable, “We were surprised by how little correlation there was between the “best banks” and the banks with the best digital experiences. Half of the top ten banks fell into our bottom ten for digital experience, and none of the Forbes’ top 10 banks were in our report’s top ten. While there is a need to focus on the bottom line, consumers expect more from their banking providers today, and organizations need to put the user first – with digital at the center of an omnichannel strategy.”

Read More: New Study Shatters Myth That Digital Channels Are Killing Branches

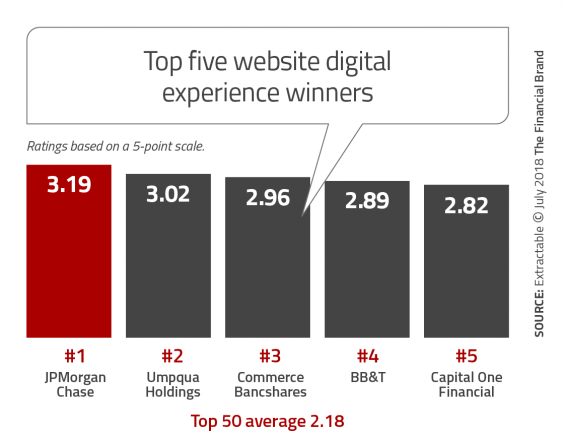

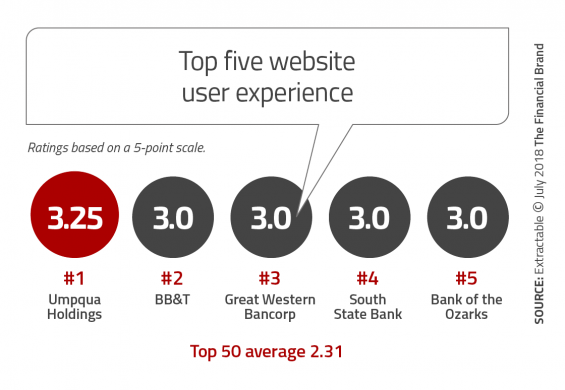

Taking the Digital User Experience from ‘Meh’ to ‘Wow’

In Internet slang, ‘Meh’ is used as an expression of indifference, with no positive or negative emotion. As visual emoji, it is usually shown as either an expressionless face or a shrug of the shoulders. This is the rating received by the top five banking organizations for user experience (UX).

With the exception of Umpqua, the rest of the top five banks got a 3 rating (good). These rankings we only 30% higher than the less inspiring 2.31 average given to the entire top 50 banks by Extractable as they considered such qualities as:

- Responsive design (78% of the sites were responsive)

- Site architecture

- Navigation

- Friction

- Layout and organization

- Customer journey

The biggest overarching flaw seen in most of the banking sites was the lack of a well designed digital application form. Even those organizations that provided the opportunity to begin the opening process digitally usually didn’t allow the consumer to finish the process without visiting a branch (friction) or start and stop the process with saved entries.

“There are so many bad account application processes out there,” stated McLaughlin. “We think this is representative of why many organizations scored so low in general. They’re just missing the mark on basic table stakes like this.”

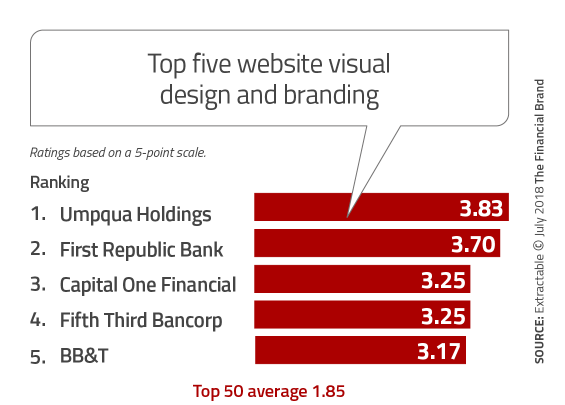

Great Visual Design Doesn’t Mean ‘Differentiation’

When it comes to visual design, the top five banks far outperformed the average, with Umpqua and First Republic Bank approaching the ‘exceptional’ score of 4. The scores of the top five banks exceeded the industry average (1.85) by between 75% and 100%.

One of the reasons the average score of the industry was so low was due to the level of ‘sameness’ between organizations. With many organizations using a relatively common layout, in conjunction with readily available stock photography, differentiation from one bank to the next was almost non-existent.

According to Extractable, one of the ways that organizations can set themselves apart could be through the use of less traditional banking colors. While there are strict branding standards at most banking organizations, that shouldn’t restrict the digital site from using an alternative palette, while maintaining other branding components. This can also be achieved with alternative fonts.

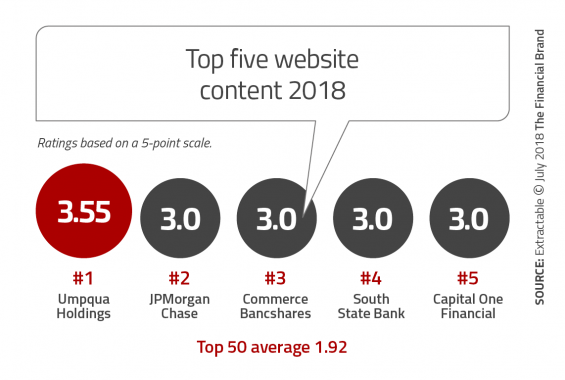

Going Beyond ‘Digital Brochures’

As fewer consumers visit physical branches, digital engagement increases in importance. Without strong digital engagement, cross-selling, satisfaction and loyalty will all be negatively impacted. The upside potential of an aggressive content strategy will allow organizations to support everything from financial education to alternative languages (only 4 of the top 50 banks had a Spanish language alternative site).

The Extractable research found that the top organizations again were mired in the ‘good’ range of scores, with the average institution getting ‘fair’ scores. It is clear there is a tremendous opportunity to do better than simply using websites to provide product descriptions and rates akin to old-school rack brochures.

Organizations should look to other industries to see how brand stories are told, comparison tables are integrated and expanded communities of customers are served. Many non-banking institutions are also having increasing success with mobile-ready video content and dedicated blog postings.

Where Should We Start. Where Should We Head.

Look at your mobile phone. If you do not have your applications set to download update automatically, you will most likely see at least a few that need updating every day. This is because true digital organizations are in a constant state of improvement. Is your organization working continuously — like this — to improve the digital experience?

According to Extractable, UX journey mapping is an effective way to identify customer needs and pain points. Done well, it is a combination of visualization and storytelling that will determine how different customers use all of your channels. Journey maps can help you understand individuals and segments, identifying both opportunities and threats as they relate to digital engagement and satisfaction.

Customer data is at the core of this process, tracking and monitoring consumers as they engage with your organization. Data is also needed to build an effective digital-first design that can evolve versus over time as opposed to always needing to be rebuilt. There is no better way to prepare for the digital future.

The goal is to create a consistent, seamless experience across all form factors, screen sizes and path. This includes being able to support voice banking sooner than later. The consumer has already embraced digital voice devices – they will soon expect to be able to do banking with these devices.

Finally, all of the efforts should focus on improved personalization of digital engagement, from design to digital marketing to content strategies. According to McLaughlin, “We saw very little effort at personalization, and most sites only addressed different audiences at a structural, high level. In most instances, there was little or no differentiation of content or messaging for different segments or personas.”

Ron Shevlin, Director of Research at Cornerstone Advisers agrees, “The Extractable study makes a point of covering the importance of personalization as a primary criteria for digital marketing. But, this had the LOWEST average score. This is where the story is – digital marketing STILL sucks.”