Just when powerful new technologies are becoming more widely available to mine and analyze consumer data, regulators and politicians around the world are taking unprecedented interest in consumer privacy. Blame it on Facebook and Google if you want, or the Russians, but consumer concerns about the privacy of their personal and financial data has soared. Officials are reacting.

This puts financial marketers in a bind. The holy grail of hyper-personalization could be stymied if consumers hit the brakes on increased use of their data.

To avoid a pile-up over privacy, financial marketers should rethink their approach to it. They must take a prudent, balanced tack to the collection, handling and use of consumer data. In other words, stop equating it with “compliance.” Instead, re-think of it as part of the customer experience — and a potential competitive advantage.

Why bring this up now? Time to mull it over is running out.

The type of requirements embodied in Europe’s General Data Protection Regulation (GDPR) likely will become more widespread. Already in the U.S., California has passed a very similar law and there are high-level calls for a federal remedy.

“GDPR has put data in the place that it deserves: at the center of the table,” Joseph Lospalluto, EVP of Americas at Smart Ad Server, tells The Drum. “It has been a wake-up call for marketers regarding data use and abuse … and the need for the ad-tech supply chain to be healthier and more transparent.” All companies, he says, need to think of prospective customers as “citizens” — not as “consumers” or as “profiles.”

“It’s hard to apply ethics without making this shift in mindset,” states Lospalluto.

As described by Deloitte in a report on financial privacy, those banks and credit unions that re-imagine privacy in the digital age should gain consumers’ trust and, importantly, their willingness to share data in return for value received.

Compliance is Not a Synonym for Transparency

Consumer ideas about privacy are evolving quickly. Possibly even faster than the speed at which bank and credit unions adopt new technologies such as virtual assistants and artificial intelligence. But though they may lag in the use of AI, many financial marketers already monitor consumers’ web browsing and social media activity.

Because of such sweeping changes in how marketing is conducted, financial institutions cannot focus on compliance alone when addressing privacy, the Deloitte report notes. They need to ensure their data mining and analysis does not alienate consumers.

For example, Deloitte says institutions should be sensitive to what many refer to as the “creepiness factor,” where consumers might find the way companies gather data about them to be too intrusive, such as creating a profile based on an individual’s online activity. Similarly, geolocation technology can be used to detect fraud, but also for other potentially invasive purposes, which some might consider too intrusive.

Many consumers may not be aware that much intimate, yet easily available information can be accessed by their financial services provider. But if they were, would it matter?

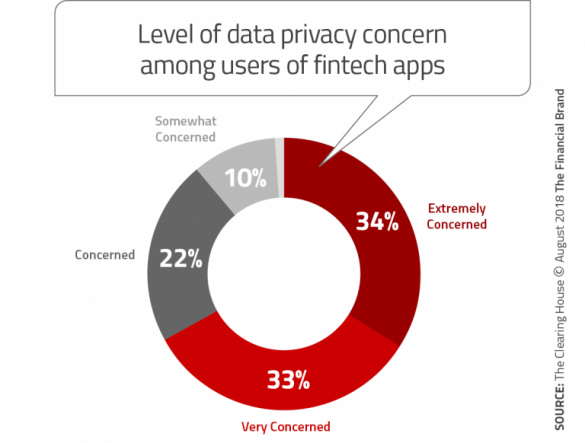

A survey by The Clearing House offers some insights in a closely related area. TCH found that nearly two out of five (41%) U.S. banking consumers already use at least one fintech app, most often relating to budgeting and saving, investment advice, and lending. When asked if they worry about the privacy of the data they share when using financial apps online or on mobile devices, more than two thirds of consumers say they are “very” or “extremely concerned.”

The TCH research also revealed a significant gap between how people think these services interact with their data and how the apps really work. Once fintech users become aware of the fact that the apps draw on their personal financial data, nearly half (47%) of them say they would be less likely to use these services going forward.

The good news: Consumers trust legacy financial institutions more than fintech providers. A.T. Kearney found banks and credit unions lead the next closest option by 13 percentage points for keeping consumer personal information safe.

In addition, three out of five consumers look to banks and credit unions to help educate them about how financial applications access and use personal data.

Read More:

- Bank Brands Should Step Up On Privacy As Facebook Freaks Consumers

- Three GDPR Challenges and Opportunities For Financial Marketers

Boilerplate Policies Invite Backlash

Deloitte suggests that if consumers are made more aware — not just about how their social media postings are used, but about the potential value such monitoring might provide for them — it could make a big difference in their willingness to let financial institutions use their data.

Achieving that kind of privacy transparency is no simple matter, however. The consulting firm identified eight types of privacy issues (shown in the gray box) that come into play in consumer financial services.

Eight types of consumer privacy issues faced by financial institutions identified by Deloitte:

1. Traditional identifiers — e.g. name, address, date of birth, race, gender, Social Security number

2. Behavior and actions — e.g. shopping, financial transactions, browsing habits, etc.

3. Thoughts and feelings — opinions expressed on social media or elsewhere on a variety of topics including companies or brands

4. Images — includes images taken by consumers and also images taken by drones or robotic devices

5. Biological data — e.g. facial features, iris image, voice, gait, and health-related information

6. Personal communications — between consumers and financial institutions or other parties via email, text, social media, and phone

7. Location and space — information about a person’s geographic location

8. Associations/groups — Knowledge of groups consumer belongs to or associates with including political, religious, work-related, or hobby-related

Further, Deloitte examined the privacy policies of 12 large financial institutions and what it found was far short of what would be needed to carry out a proactive privacy communication effort with consumers. All banks in the sample provided identical, boilerplate factsheets on what, how, and why data is shared.

The report concluded that such rudimentary privacy policies may set the stage for a privacy backlash among consumers. It urged financial services firms to create appropriate strategies, policies, and controls to deal with all the new forms of data now in use and in a way that transparently responds to consumer concerns and questions. respond to such provocative questions could be at risk.

Read More:

- Fintechs vs. Traditional Banks: Who Has the Bigger Advantage?

- Top 10 Retail Banking Trends and Predictions

5 Steps to a Forward-Looking Privacy Framework

Deloitte made five recommendations for financial institutions in regard to privacy:

1. Broaden the privacy lens. Go beyond the basic checkpoints and requirements to account for new and often overlapping technologies (e.g. artificial intelligence and geolocation). Be proactive in considering how privacy concerns will evolve in terms of technology, consumer attitudes and regulatory constraints.

2. Review and revamp current privacy policies. Today they are mostly minimal efforts to clear regulatory hurdles. Financial institutions can use more transparency to earn customer trust and demonstrate good faith, by showing people how they could benefit from various types of data collection and analysis.

3. Be good stewards of the data you collect and purchase. Data security is, or should be at the forefront, but quality control, accuracy and relevance are also important. Systematic vetting of data collected would help.

4. Make positive use of emerging technologies and new data sources. Consumers should be kept in the loop as institutions explore new data sources and methods, including what the value proposition is for the consumer, such as tailored offerings, new services, better pricing, or reduced time for service delivery.

5. Set up a chief privacy officer position. These individuals should be empowered to develop new privacy management strategies.

Key Takeaway: Financial institutions will need a more robust, expansive, pragmatic, and forward-looking framework to successfully navigate the changing privacy landscape.

If banking institutions truly want to meet consumers’ expectations and respond to their fintech challengers, they are going to have to shift the way they approach personalization and build new engagement models, based on transparency and trust, observes Peter Matthews, CEO of Nucleus.

Banks and credit unions that are proactive on privacy issues can shape how customers view the value of their data, says Deloitte. In the process institutions can both differentiate themselves from competitors and more effectively serve their customers.