Nothing in recent memory has captured the attention of the financial press more than the announcement of Libra, Facebook’s proposed cryptocurrency, expected to be introduced in early 2020. The stated mission of Libra is for the currency to be “a simple global currency and infrastructure that empowers billions of people.” A multipurpose payment tool (not to be confused with the much more highly speculative bitcoin), Libra is proposed as a way to pay people or companies globally without a fee. Eventually, it may also serve as a form of payment contracts, loans and insurance.

Unlike bitcoin, the value of the coin is to be set against an assortment of more stable global currencies, with a single Libra being worth roughly the same as a dollar. While not an insured currency, the Libra will have a reserve during the span of the transaction. Facebook is a founding member, but there will be a nonprofit Libra Association with roughly 100 founding members, including Visa, Mastercard, PayPal, eBay, Lyft, Spotify and Uber, with each expected to invest a minimum of $10 million to fund the project. Facebook does not intend to run the network, and in fact, it wants to include direct competitors like Google or Twitter.

The Libra Association has released a white paper that goes into great depth around the concept. One of the concerns mentioned in the white paper is the security and stability of private currencies. “The challenge is that as of today we do not believe that there is a proven solution that can deliver the scale, stability, and security needed to support billions of people and transactions across the globe through a permission-less network,” the whitepaper notes.

What is important to understand is that Facebook is not creating a payments platform that will directly compete with commercial banks. Instead, it is actually launching a form of currency that competes with central banks.

That does not mean there is no impact on retail banking. For instance, Facebook will probably go straight to retailers and other strategic partners, and bypass a lot of the traditional payments gatekeepers — like traditional financial institutions. There is also the obvious benefit of lower cost international transfers of funds, undercutting banks’ transaction fees, especially internationally.

Read More: Cash Out: Is Currency on the Brink of Extinction?

The Next PayPal or Venmo?

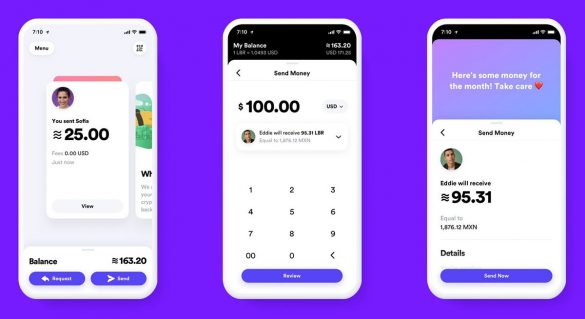

Most assume that Libra’s initial rollout will take place on Facebook’s Messenger, WhatsApp and Instagram platforms for cross-border payments and for those consumers that are unbanked. In addition, given the massive scope of consumers who are Facebook customers, there is no reason that the currency wouldn’t become the primary source of payments between individuals using Facebook, similar to how PayPal and Venmo are used today.

This is even more possible due to the elimination of transaction fees common with credit cards. Facebook has even developed a method of currency storage — a wallet app called Calibra.

Calibra will will have the potential to provide Facebook immense amounts of new data and an advantage over other rivals, including traditional banks. Even though Facebook says that the insight from the wallet app will not be combined with Facebook data for ad targeting, the consumer can still give permission for Facebook data to be integrated with Calibra for added speed and benefits.

![]()

And since Facebook has a relationship with 7 million advertisers and 90 million small businesses, the potential of using data is significant. The combo of Libra and Calibra allows the social network to provide loans, credit, money transfer, and e-commerce with the simplicity that it currently allows for P2P communication.

Ultimately, this could become one of the most functional open banking platforms outside of China.

The Importance of Trust

The success of Libra will depend on trust more than anything else. Trust in both the stability of the currency as well as the privacy of consumer data. “To earn people’s trust, we are going to have to make strong commitments on privacy,” said David Marcus, the head of Facebook’s Calibra division.

This may be a bit of an uphill battle. In theory, spreading the control of Libra across a hundred additional companies is supposed to address the issue of trust, but Facebook’s involvement in the development of Libra can’t be ignored. Recent issues regarding privacy of consumer data could be a challenge to user adoption.

Government Concerns

As is often the case, governments are playing catch-up with regards to this fintech innovation. The government negative reaction to Libra started in Europe, where regulators fear that the system could disrupt the global economy and rival national banks.

In the U.S., the head of the U.S. House of Representatives Financial Services Committee, Congresswoman Maxine Waters, wants Facebook to temporarily stop developing its cryptocurrency. She is joined by her Republican counterpart as well as a growing number of bipartisan House and Senate members.

“There is currently no clear regulatory framework to provide strong protections for investors, consumers and the economy when it comes to cryptocurrencies,” Waters stated. These concerns come at a time when several of the tech giants are under increasing scrutiny around the powers they have regarding customer data and privacy.

Compete or Collaborate?

As a concept, Libra appears as if it has many advantages as a cryptocurrency. First of all, it provides a very low-cost way of transferring money globally for those unbanked people who need it most. It’s being backed by not only Facebook, but also by some of the strongest digital and tech-based firms in the world. The new currency will be entirely digital, accessible at any time on a mobile device or computer. And, most of all, it should be more stable than the speculative cryptocurrencies most of us are used to.

That said, most traditional financial institutions should be wary of the other component of the announcement by Facebook. The integration of the digital wallet Calibra will not only be integrated with the Libra currency, but with an extension of other financial services yet to be named. Is this the real Trojan Horse of the Facebook announcement?

Calibra is just another example of how big tech firms are finding ways to encroach on the turf that has been the domain of legacy banks forever. The big question – how should retail banks respond to the continual onslaught of challenges from firms including Facebook, Amazon, Google, Apple and others? Standing on the sidelines is most likely not the best strategy.

Most tech giants, at least to this point, have not opted for a banking license. They have looked to traditional financial organizations to be a partner in their foray into banking. A recent example is the collaboration between Apple and Goldman Sachs on the new Apple Card. So, is the best response for retail banks to build partnerships with the very firms that are arguably the biggest threat to the industry? Not doing so may risk the insights and engagement of millions of customers.