Similar to consumer digital banking, there is a tremendous opportunity to increase engagement, deepen banking relationships and generate revenue from moving small business relationships to digital channels. Despite a willingness to pay for digital banking services, however, financial institutions too often give away small business digital banking services. There is also a negative perception of digital banking services from small businesses that must be overcome.

To assess the missed revenue opportunities provided by small business, RateWatch and Simon-Kucher & Partners have conducted annual studies on product design and pricing of mobile banking applications for small business customers. The current report provides insights beyond the mobile channel to include digital banking as a whole. The study also looks at the selling process for small business digital solutions.

The report reveals insights into the small business customer, including their mobile usage, banking behaviors and utility scores on 24 different banking services. It also shares insights on their willingness-to-pay and estimates the likelihood-to-purchase at a series of price points for any given service bundle.

Behavioral segmentation is used to identify six distinct clusters of small business customers which helps in the determination of product use, pricing and positioning.

The following are key findings based on the small business customers surveyed:

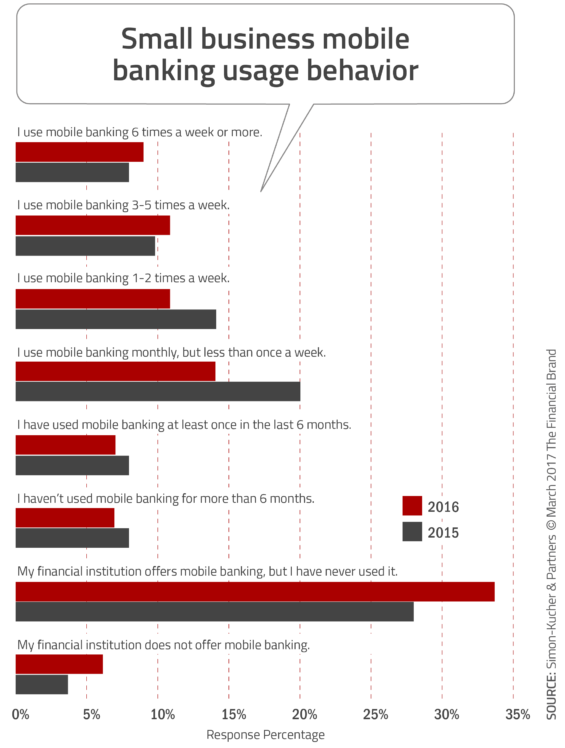

- 34% have never used mobile banking, even though their financial institution offers it

- 69% do not have a positive perception of mobile banking services offered by their institutions

- Certain small business clusters have significantly higher willingness to pay for digital services than others

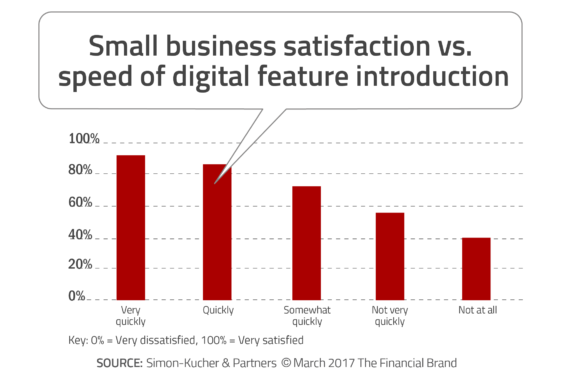

- Customer satisfaction is directly correlated with the rate at which digital innovations or new digital features are introduced

- There is a lack of ‘leader’ features and high variance across all digital banking services, suggesting a bundling approach that is logically coherent but still allows for customization

“The small business customer is a huge untapped market for financial institutions,” said Jamie Zussman, a business development associate for RateWatch. “This report provides data and a framework for how financial institutions can deepen their understanding of this segment and create compelling packages and services for them.”

“We need a systematic and structured approach to designing, pricing and selling mobile banking solutions,” said David Chung, a director at Simon-Kucher & Partners. “When these steps are managed separately, we find sub-optimal products that fail to meet revenue and profit goals and fall short of addressing customer needs.”

Small Business Experience Gap

The research found that there is a gap between what small business owners want from their digital banking experience and what financial institutions are offering. This gap in delivery has impacted everything from digital banking utilization to the revenue potential from this important segment. It was also found that small business customers surveyed said their satisfaction with mobile banking is correlated directly with the rate at which digital innovations or new digital features are introduced.

When we asked Chung about the user and usage trends of mobile and online channels by small businesses, he stated, “On mobile, the increased usage of heaviest users is likely due to banks increasing their incentives to move transactions to their most cost-efficient digital channels,” says Chung. “We’re seeing channel-based pricing where channels with a lower cost to serve are priced lower than full-service channels.”

And what about the decrease in mobile users? Chung believes consumers will abandon mobile when they can’t see the value in it: “If they don’t see the value of the services offered through mobile, they will opt to use those channels less.”

To improve the utilization numbers of both online and mobile banking, Chung says financial institutions must focus on CX.

“A consumer’s continuous utilization of a digital application is largely driven by its intrinsic value,” Chung explains. “That simply means the institution must create the right experience within the application with the right features at a fair price will guarantee the increase in usage.” Regarding the apparent dissatisfaction with digital channels overall, “This indicates that current services are not delivering the desired value,” Chung says. “Banking providers need to rethink their product offering and design approaches to define how to better serve their customers.”

What features or functions will make the perceived value of online and mobile banking for small businesses stronger? Chung says financial institutions should add more features and services to help small businesses manage their cash flow more conveniently.

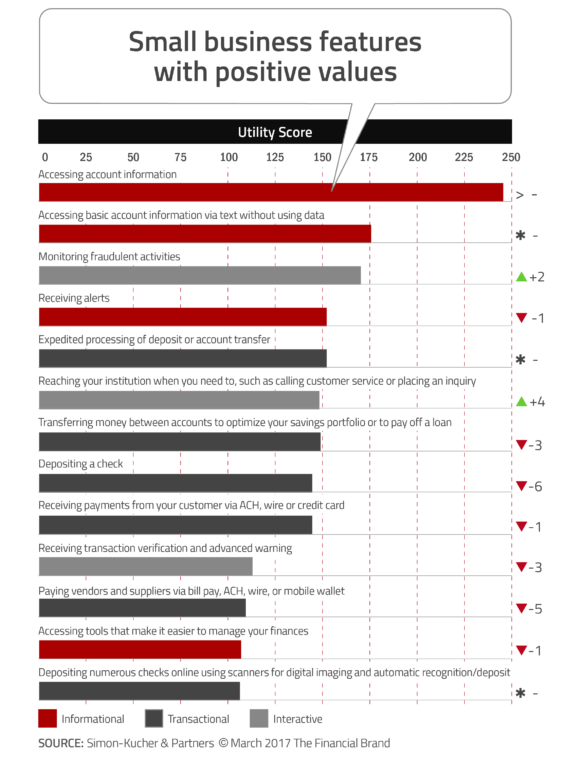

“This will increase the value perception of online and mobile,” says Chung. “Look at the top ten most valuable features. They don’t shift much from year to year, which suggests that the existing offering is not quite meeting expectations — neither in value perceptions, value delivered, or price perceptions.”

Chung specifically notes a couple of features that tested fairly well in their research, including monitoring for fraud and improved digital payments solutions.

“They want the ability to pay their vendors and suppliers via bill pay, ACH, wire, or mobile wallet, and receive payments from customers the same way,” Chung says. “Both types of payments would add to the convenience of cash management and monitoring for small businesses.”

Chung says there is still a lot of room for banks and credit unions to improve the ways in which they monetize their mobile banking offering for small businesses.

“They need to do a better job onboarding small businesses onto their mobile services, whether it be through better value communication or enhanced training,” he says. “They need to understand customer needs, design and package products targeted at those needs, price them fairly based on willingness to pay, and communicate value effectively through sales and engagement channels.”

Closing the Revenue Opportunity Gap

According to Simon-Kucher, almost 75% of banks are not able to generate the amount of revenue they deserve from small businesses. The research finds that organizations often believe that their products are commodities and that they lack pricing power, especially in an era of consumer activism and regulatory intervention. A low rate environment, as well as high consumer and media scrutiny of pricing changes, compound their pricing challenges.

As a result of the above forces, financial services organizations are generating 25% less profit on average. Simon-Kucher believes the key to small business success is the integration of various products and innovations into a single product portfolio ecosystem. The result of product bundle optimization is a win-win-win situation where customer experience is improved, front-line sales find it easier to sell products, and price becomes a secondary question. A structured framework provided in the research includes:

- Step 1: Understanding customer needs, using segmentation based on behavioral attributes.

- Step 2: Designing and pricing the offering to define the price tags for bundles and individual features.

- Step 3: Selling the bundles leveraging customer behavioral economics combined with digital brochures and tools.

With numerous ‘urgent’ priorities, most banks are struggling to keep up with banking transformation. At a time when revenues and an improved customer experience are top priorities, using product portfolio modeling can provide the best solution. “Financial institutions must recognize the hidden value of their digital solutions in order to effectively monetize their portfolio. By taking measured steps to assess their offering, pricing, and sales approaches, they can more easily meet the challenges of the rapidly evolving digital banking landscape,” concluded the research study.

About the Report

A survey with a panel of 215 US-based small business1 managers was conducted as the basis for this report. The pool of respondents spanned 20 major industries. 85% of the respondents are directly responsible for their business’ day-to-day banking activities and are well-versed on digital banking usage behavior and preferences. All survey responses were collected in the third quarter of 2016. A range of statistical and analytical methods, including factor analysis, cluster analysis, MaxDiff analysis and conjoint analysis were employed to develop key insights. The research is available for purchase here.