PNC to Vault to #5 Ahead of U.S. Bank in BBVA Deal Embracing Branches

In a period when use of digital channels has been accelerated by COVID-19, PNC is making an $11.6 billion cash bet on Americans' perceived love of branches for key decisions and new relationships. The deal will take the regional coast-to-coast and into 'near national' status. The potential for more industry-shaking deals now looms.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

In an affirmation of physical banking, PNC Financial Group has struck a deal to buy BBVA USA from its Spanish parent in an all-cash deal that puts a premium on dramatically adding to PNC’s geographic territory while increasing its branch network count by nearly 30%.

This acquisition comes at a time when COVID-19’s acceleration of digital channel adoption and closure of branch lobbies has stepped-up trimming of networks. This overlays the debate over the future of the branch that has been going on for nearly a decade.

Yet in announcing the $11.6 billion purchase of BBVA USA in mid-November 2020, William Demchak, PNC’s Chairman, President and CEO, stressed that this would be a very different kind of acquisition than the markets and securities analysts have grown used to seeing.

“We’re not doing the traditional branch deal where you go in and shut down half the branches serving communities in your market,” said Demchak. “That’s the usual ‘rip branches out’ model. We’re not doing that. We’re actually going to add products and services and capabilities to the markets we’re entering.”

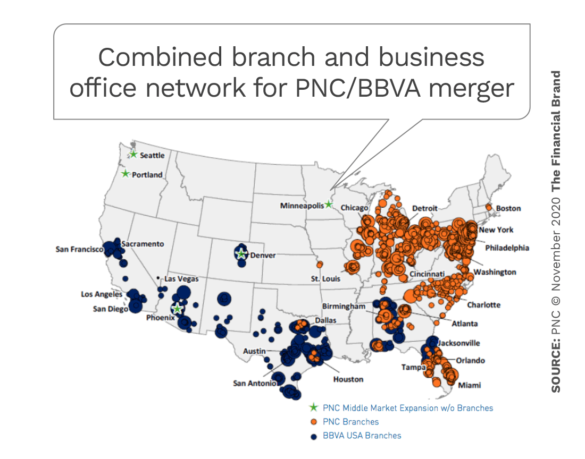

Other than in Alabama and Florida and two parts of the huge Texas market, the two banks have little overlap in their branch systems. PNC’s network sits mostly east of the Mississippi, while BBVA’s covers much of the Sunbelt with a swing up into northern California.

Demchak also said that PNC will be investing in client-facing staff to generate enhanced earnings growth.

Click on the map for a closer look.

By contrast, the combination of SunTrust and BB&T to form Truist in 2019 generated an initial round of branch divestitures that is being followed up with additional closures, now at an accelerated pace.

A Closer Look at a Ground-Breaking Bank Deal

The acquisition, expected to be completed in mid-2021, has been in PNC’s sights for years, according to Demchak. The deal would take PNC, with assets of $461.8 billion as of the end of the third quarter of 2020 to $564.2 billion on a pro forma basis. This would carry PNC past the present #5 institution, U.S. Bank. PNC currently occupies seventh place.

The acquisition would also put the combined entity into 29 of the 30 largest Metropolitan Statistical areas with at least a branch or a business banking office.

PNC/BBVA networks compared in 29 of top 30 Metropolitan Statistical Areas

| Rank | MSA | PNC | BBVA USA |

|---|---|---|---|

| 1 | New York, NY | ✓ | ✓ |

| 2 | Los Angeles, CA | ✓ | |

| 3 | Chicago, IL | ✓ | ✓ |

| 4 | Dallas, TX | ✓ | ✓ |

| 5 | Houston, TX | ✓ | ✓ |

| 6 | Washington, DC | ✓ | ✓ |

| 7 | Miami, FL | ✓ | ✓ |

| 8 | Philadelphia, PA | ✓ | |

| 9 | Atlanta, GA | ✓ | ✓ |

| 10 | Phoenix, AZ | ✓ | ✓ |

| 11 | Boston, MA | ✓ | |

| 12 | San Francisco, CA | ✓ | |

| 13 | Riverside, CA | ✓ | |

| 14 | Detroit, MI | ✓ | |

| 15 | Seattle, WA | ✓ | |

| 16 | Minneapolis, MN | ✓ | |

| 17 | San Diego, CA | ✓ | |

| 18 | Tampa, FL | ✓ | ✓ |

| 19 | Denver, CO | ✓ | ✓ |

| 20 | St. Louis, MO | ✓ | |

| 21 | Baltimore, MD | ✓ | |

| 22 | Charlotte, NC | ✓ | ✓ |

| 23 | Orlando, FL | ✓ | ✓ |

| 24 | San Antonio, TX | ✓ | |

| 25 | Portland,OR | ✓ | |

| 26 | Sacramento. CA | ✓ | |

| 27 | Pittsburgh, PA | ✓ | |

| 28 | Las Vegas, NV | ||

| 29 | Austin, TX | ✓ | |

| 30 | Cincinnati, OH | ✓ |

PNC:

✓ Branch presence ✓ Middle market expansion, w/o branch presence

BBVA USA:

✓ Branch presence ✓ Commercial/private client offices

The following table illustrates how the new PNC will pull ahead of U.S. Bank after the acquisition is finalized.

PNC/BBVA deal will create new #5 U.S. bank

| ($ billions) | PNC as of 9/30/20 | BBVA USA as of 9/30/20 | PNC Pro Forma | U.S. Bank as of 9/30/20 |

|---|---|---|---|---|

| Assets | $461.8 | $102.4 | $564.2 #5 U.S. Bank | $540.4 |

| Loans | $249.3 | $66.2 | $315.5 #5 U.S. Bank | $311 |

| Deposits | $355.1 | $86.4 | $441.5 #5 U.S. Bank | $405 |

| Branches | 2,207 | 637 | 2,844 #5 U.S. Bank | 2,604 |

| Loans to deposits | 70% | 77% | 71% Core funded | 77% |

| Loan Mix: Commercial/Consumer | 69%/31% | 65%/35% | 68%/32% Maintaining commercial expertise | 50%/50% |

Source: Company filings

While that is still far from the trillion-dollar asset levels of JPMorgan Chase, Bank of America, Wells Fargo and Citigroup, it would also carry PNC past Truist. More strategically, the combination would take the merged entity from East Coast to West Coast, with gaps only in the North, making it, in the description of the Wall Street Journal, a “near national” bank in scope.

Read More:

- KeyBank Fighting Megabanks & Big Techs With a ‘Digital-Plus’ Strategy

- How Bank Branching Advocates Feel About Expansion Plans Now

- Trimming Branch Networks? Many Financial Institutions Find It Tough

A Test of Branching’s Future is in the Offing

The branching strategy and stance among the top ten U.S. retail banks varies tremendously according to business model and geographic footprint. JPMorgan Chase has been trimming but also aggressively moving physically into new markets. In an interview with The Financial Brand in mid-2020 Wells Fargo’s Mary Mack, Senior Executive Vice President/CEO of Consumer & Small Business Banking, noted how important branches remain for her institution. Citi, on the other hand, has kept a tight rein on U.S. branches for years, and Capital One has been aggressively shedding traditional branches while adding more of its unique “cafe” branches.

Domestic branch counts for top ten U.S. banks* by asset ranking

| JPMorgan Chase | 5,031 |

| Bank of America | 4,268 |

| Wells Fargo | 5,277 |

| Citibank | 711 |

| PNC/BBVA Pro Forma | 2,844 |

| U.S. Bank | 2,604 |

| Truist Bank | 2,920 |

| PNC | 2,261 |

| TD Group (U.S.) | 1,232 |

| Capital One | 386 |

| HSBC | 160 |

Source: FDIC website, PNC merger announcement

Memo: BBVA as of the same date had 639 domestic branches.

*Table lists banks with significant retail branch operations in U.S. As of 9/30/20 except PNC/BBVA pro forma.

PNC, while it has been trimming branches in established markets, has been launching slimmed down “Solutions Centers” in new markets in a “branch-lite” configuration. The idea is to plant the flag and show presence while promoting for digital growth as well. The markets currently in the branch-lite plan include Houston, Dallas, Boston, Kansas City, Minneapolis, Nashville and Denver. During a fall 2020 analyst event PNC indicated that by yearend a total of 25 solution centers will have been opened and that 25 more would open in 2021.

BBVA, though considered a digital pioneer, in mid-2020 announced plans to expand its Texas branch network with 15 new slimmed-down, reimagined branches originally slated to open in early 2021.

Speaking with analysts during the announcement of the BBVA deal, Demchak noted that BBVA had specific plans and that those plans “we are probably in support of. We’ll go through it piece by piece.”

Demchak stressed to analysts that expansion to new markets and building out in high-growth areas don’t negate the broader evolution of networks.

“None of this changes the continuing trend of thinning branch networks, which we will continue to do,” said Demchak. “Ultimately, the right model, I believe, is somewhere between what we’ve established in our newer, thinner markets today and in our ‘thicker’ markets like Pennsylvania.”

How PNC Will Set Up the BBVA Marriage

Rather than finding savings as a result of slashing branches, Demchak said, the company will save by not acquiring BBVA processing centers. He calls the coming move “lift and shift.” First, BBVA processing will be placed into PNC IT centers and most accounts and data will be poured into PNC’s own platforms.

In addition, he expects to see savings by pulling BBVA under an American owner. BBVA USA had to spend a good deal to continue operating under a global parent, spending that wasn’t necessary to domestic operations.

“That can stop now,” says Demchak.

He told analysts that because the deal isn’t based on eliminating masses of branches to make the numbers work, communities won’t face loss of bank offices in the merger’s wake. He notes that PNC has earned “Outstanding” ratings in Community Reinvestment Act examinations for decades and that BBVA has a strong CRA record as well.

PNC anticipates that part of what will make the deal work is gaining more scale for efforts started by both banks and to add markets for some specialties that PNC offers that BBVA lacks — a large suite of fee-based business services, for example.

Demchak noted that BBVA has invested heavily in customer-facing digital technology, offering “some really attractive products that haven’t been brought to scale yet that we can help with.” One example is BBVA International Money Transfer Service, which Demchak wants to push out to the entire PNC system after the merger.

In-Person Relationships Are Stronger than Digital

In past analyst presentations PNC management has made it clear that it understands that consumers were moving towards digital channels even before COVID forced the issue for many, but that at the same time for many significant banking needs they still wanted to meet with a banker. The bank considers its Solutions Centers to be the best of both worlds.

“We are more convinced than ever that physical presence matters.”

— William Demchak, PNC

In a 2020 discussion with Erika Najarian, Managing Director at BofA Global Research, Demchak discussed the experience of generating new customer relationships via digital channels alone versus through the Solution Centers. He said the latter were higher-quality relationships for the bank.

“We are more convinced than ever that physical presence matters,” said Demchak. “What digital does is allow the frequency by which you have to visit a physical branch to go way down and so we can space them out more than even ten years ago. And that’s what you see us doing.” The bank has also been refining new versions of its Virtual Wallet product through the centers.

“But is the cost of these new customers greater than the cost of building a best-in-class digital banking organization and acquiring customers that cost less to acquire and service?”

— Jim Marous, digital banking advocate

Digital banking advocate Jim Marous is skeptical.

Marous, who is Co-Publisher of The Financial Brand and Owner/CEO of the Digital Banking Report, believes that geographic reach is important for the acquisition of new customers in new areas. “But is the cost of these new customers greater than the cost of building a best-in-class digital banking organization and acquiring customers that cost less to acquire and service?” he asked. “Is the acquisition model steeped in legacy thinking and legacy pricing multiples for branches that generate 60%-80% fewer visits than a decade ago?”

Marous feels that PNC, a pioneer with the original introduction of its Virtual Wallet over a decade ago, has lagged other institutions in development of digital services since.

He describes PNC as a strong but risk-averse organization. “While the organizations may marry well, I am not convinced the innovative culture of BBVA is transferable,” said Marous.

Is Chime a Highly Promoted Loser?

For his own part, Demchak is skeptical about the actual performance of some digital brands that cultivate a trendy image in the industry.

During the bank’s third quarter 2020 earnings call an analyst asked Demchak about the success of Chime and other neobanks at attracting customers exclusively online. Demchak responded at length.

“I wish we had the opportunity to basically not have to make any money and grow customers by giving stuff away,” said Demchak. “There’s nothing that they have that we don’t have, nothing that they have that we can’t produce if we wanted to have it.”

He added that “they’re all running on third-party banks, which is a whole other issue that drives me insane. … They find very low-balance customers and I just don’t think, long term, that model works.”