You can probably count on one hand how many times Elizabeth Warren, U.S. senator from Massachusetts, has agreed with Jamie Dimon, chairman and CEO at JPMorgan Chase.

During a mid-2021 hearing of the Senate Banking Committee, Warren called Dimon “the star of the overdraft show. Your bank collects more than seven times as much money in overdraft fees per account than your competitors.” After talking over Dimon’s attempts to respond, Warren finally demanded, “Mr. Dimon, will you commit right now to refund the $1.5 billion [in overdraft fees] you took from customers during the pandemic?”

The response of the largest U.S. bank was unambiguous: “No.”

But during early December 2023 hearings that brought top officials of the eight largest U.S. banks before the committee, Warren was on a different mission. She wants to kill the cryptocurrency business. The Massachusetts senator was hunting for allies.

First, she looked at Brian Moynihan, chairman and CEO at Bank of America, and asked him if his institution has systems in place to flag terrorist financing so it can be reported to law enforcement and shut down. “Yes, we do,” he answered.

She then asked Dimon the same question. “We have extensive systems in place — but no system is foolproof,” he said. Warren asked for a show of hands from the banker panel and every one of the eight has anti-money-laundering and anti-terrorist financing programs in place — as you’d expect. Warren was making a point.

“Today’s terrorists have a new way to get around the Bank Secrecy Act: cryptocurrency,” said Warren. “Last year, an estimated $20 billion in illicit crypto transactions funded every kind of dangerous criminal. North Korea has funded at least half its missile program, including nuclear weapons, using the proceeds of crypto crime. And Israeli officials have confirmed that Hamas received millions of dollars through crypto transactions, including large sums from Iran.”

She asked Dimon how that could be. He explained that he’s long been opposed to cryptocurrency, especially given that many of the reasons it is used are illegitimate.

“If I was the government,” said Dimon of crypto, “I’d shut it down.”

Warren clearly approved of Dimon’s response, and then said that federal money laundering enforcers have called for an update to banking law to rope in crypto. She and others in the Senate want to get that done.

“Crypto lobbyists are working overtime to block any legislation. They claim crypto is distinct and shouldn’t have to comply with the Bank Secrecy Act, even if that means letting terrorists, drug traffickers and ransomware criminals and rogue nations move billions of dollars totally unrestricted.”

— Sen. Elizabeth Warren

She went down the panel and asked Charles Scharf, CEO and president at Wells Fargo, if crypto firms should have to comply with the same rules his bank must? “Absolutely, Senator,” he said. “Absolutely,” said Moynihan. “Absolutely, positively, and certainly,” said Dimon with a grin, as Jane Fraser, CEO quickly chimed in. The rest of the bankers also said, “Absolutely.”

“When it comes to banking policy, I am not usually holding hands with the CEOs of multibillion dollar banks,” said Warren, “but this is a matter of national security.”

Four Other Notable Moments from the Hearing

The main theme of the hourslong hearing was the pending “Basel Endgame” regulations that would substantially increase the capital that the largest banks must maintain. The proposal, published in July, could increase capital requirements on the megabanks by 16% or more. But committee members could raise any matter they chose, and sometimes this led to surprising exchanges. Four of note:

1. JPMorgan Chase’s Dimon Would Privatize FDIC

Having spent more than two decades at the helm of what is now the nation’s largest bank, Dimon often serves as both a spokesman for his own institution and a statesman of sorts for the entire industry.

Late in the hearing Sen. John Fetterman, a junior Democratic committee member from Pennsylvania, began quizzing the bankers, notably Moynihan and Dimon. He suggested that the new capital rules would be an appropriate intervention with the industry in the wake of the banking crisis of early 2023.

Moynihan, cordially, wasn’t having it. He noted that the big banks were going to absorb a big bill for FDIC’s cleanup.

“In a week or so, we’ll cut a check for $2.1 to $2.2 billion to pay for the costs of the cleanup,” said Moynihan of BofA’s share alone. He pointed to numerous stress tests that major banks have to pass each year as well as multiple capital rules that already apply. He added that major banks were a source of strength to the regulators’ efforts during the crisis period. When Fetterman suggested the Silicon Valley Bank’s failure almost took the banking system down, Moynihan pointed out that the situation was resolved.

After a bit more of this, Dimon jumped in.

“There were specific things that happened at Silicon Valley Bank that should be addressed by regulations, and the most important one is excessive interest rate risk,” said Dimon. “That’s got nothing to do with Basel III.”

Then Dimon segued in an unexpected direction.

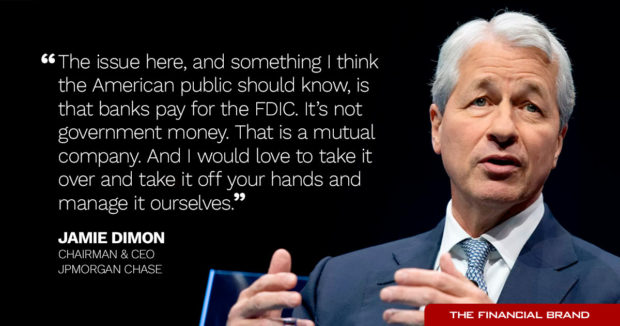

“The issue here, and something I think the American public should know, is that banks pay for the FDIC. It’s not government money. That [FDIC] is a mutual company,” said Dimon. “And I would love to take it over and take it off your hands and manage it ourselves.”

Fetterman said he didn’t see how it mattered whose money it was, but then moved on to ask about something else: Why companies like JPMorgan Chase do share buybacks and why they pay dividends.

“Would it be easier just to hold onto a lot of that money, and lend it out?” he asked the banker.

Dimon explained that the bank did all the proper lending it could, and simply continuing to lend beyond that would produce losses and cut profitability.

“I don’t think you should be asking people to do stuff that’s unprofitable for their shareholders,” said Dimon. “That’s more like a charity. There’s tons of that. It’s the shareholders’ money.”

Read more: Timeline & Explainer: How a Historic Week Unfolded for U.S. Banking

2. Senate Banking Chairman Favors Stringent Capital Standards

Ohio Democrat Sherrod Brown, chairman of Senate Banking, is no fan of megabanks, as he generally made clear in his opening statements. “Mistakes you make affect the whole economy,” he told the panel. “And we all remember how 2008-2009 certainly affected American taxpayers.” Investors, not taxpayers, should be on the hook when bank risks don’t pay off, he said, and that’s why the biggest banks need strong capital requirements.

In fact, Brown objected to an extensive industry ad campaign to get Congress to review the federal banking regulators’ Basel III Endgame proposal. While much of the campaign has been running in out-of-home venues in Washington, D.C., Brown noted that the campaign has even run spots on Sunday Night Football. The general thrust is that increased capital burdens will wind up trickling down and costing small business customers as well as consumers.

Brown expressed his skepticism. “You know that those glossy ads don’t tell you that your banks have been reducing your lending to small businesses, veterans and homebuyers for years,” sniped Brown. “Long before the new capital requirements were proposed.”

“Working Americans are tired of arrogant executives gambling with other people’s money and riding off into the sunset without any consequences,” Brown said.

The flip side, expressed by Tim Scott, the Georgia Republican who is ranking member of the committee, is that the increased capital burden will make certain services too heavy to continue and in general put funds on the sidelines that could otherwise go into business and personal loans.

Dimon objected to the way regulators handled Basel III overall.

“I feel that ‘propose now, study later’ has become a troublesome new theme in Washington,” said Dimon.

Citigroup’s Jane Fraser said that raising capital requirements by double digits “on an industry that all participants believe is well-capitalized is a bad idea in any environment.” But she said it was especially ill-advised at a time when many consumers need additional credit. Fraser suggested that when banks can’t extend further credit, borrowers will turn to less-regulated nonbanks, “which carries its own risk for consumers and the financial system’s stability.”

One committee member, Mike Rounds, a South Dakota Republican, speculated that growing use of buy now, pay later services was a sign that consumers are already having trouble. He complained that the typical family of four in his state spends $900 more each month for normal living expenses before a combination of rising interest rates and the return of inflation arrived.

David Solomon, CEO of Goldman Sachs, pointed out that Federal Reserve stress tests have confirmed that all eight of the institutions appearing at the hearing — Morgan Stanley, State Street and BNY Mellon were also represented — have enough capital to survive a severe global recession. He also observed that in the wake of major interest rate increases, the U.S. economy had shown more resilience than he had expected, raising the question of whether the extra capital is necessary. He also pointed out that the costs of the extra capital will likely be passed to customers.

Brown posed a no-win question to the banker panel at one point: “Do any of you have any reason to believe that your firm would not be able to achieve the increased capital requirements if Basel III was adopted as proposed?”

Saying “yes” would mean that raising more capital would be a problem, something no CEO would want to say in such a forum. On the other hand, saying “no,” by not stepping forward when asked the question, effectively suggests acquiescence.

3. Are Emerging ‘Branch Deserts’ Just a Mirage?

Sen. Bob Menendez, a N.J. Democrat, complained to the bankers — three of whom are not from consumer-oriented banks — about the downward trend in U.S. bank branches.

“This has left more and more residents in banking deserts, facing difficulties in carrying out basic financial tasks such as paying bills and depositing checks,” said Menendez.

“I understand that part of this is mobile and online banking,” said Menendez. “But there are many who do not have the ability to do that.”

BofA’s Moynihan said that roughly 30% of the bank’s branches are in low- and moderate-income neighborhoods. He said it was important to understand that previously unbanked people were increasingly being served by big banks. Moynihan and other bankers spoke of the expansions that their branch systems were undergoing. He said that there was a balancing between branching and bringing more people into the digital fold.

“97% of our low- and moderate-income customers use digital banking, which is more convenient, safer and reaches them where they are,” Moynihan said.

Read more about branch expansion:

- Why Bank of America Is Covering the Country with Branches

- JPMorgan Chase Defends Contrarian Branch Strategy as Deposit-Gathering Machine

4. Warning to Banks: Stay Out of Politics

In a standalone discussion, Sen. J.D. Vance, an Ohio Republican, criticized institutions on the panel over stances that they have taken on controversial issues. He trotted out a chart on an easel, presenting the eight banks and which issues, listed across the top of the chart, that they had weighed in on. Among the issues were debates over the controversial Georgia voted ID law, gun control and abortion rights.

“Nobody elected you,” said Vance. “Stay out of public policy unless it affects your core business interests — because if you don’t, it’s going to be a lot harder for us to see you guys as neutral arbiters and neutral actors in the American financial system. It’s going to be much easier for us to see you as political actors.”

The consequences? If banks take sides in political issues, that makes Vance, at least, less willing to work for changes banks want, such as a tax break or for more reasonable regulations.

“I’m one Republican who wants to have a good relationship with you, but the more you guys insert yourself into these fights,” said Vance, “the less good that relationship will be.”