Modest-sized fintech firms and large tech giants continue to make retail banking inroads worldwide, providing services that leverage the best in digital technology to deliver a customer experience that removes cumbersome steps from both routine and more involved banking engagements. Relative financial newcomers like AliPay (China), WeChat (China), Rakuten (Japan), Atom (UK), Monzo (UK), Starling (UK), N26 (Germany) and Revolut (UK) have joined household names like PayPal, Amazon and Google to disrupt the banking ecosystem, leveraging modern infrastructures and innovative cultures.

According to Bain, “Many of the tech giants possess the ingredients of success: digital prowess, large customer bases, organizations well versed in improving the customer experience, and ample leeway to extend their corporate brands into banking.” More concerning may be that some of these firms are generating a level of trust previously reserved only for traditional banks and credit unions. As a result, an increasing percentage of consumers are willing to use financial products offered from these non-traditional firms – especially where the experience is superior to that offered by legacy organizations.

It is expected that demand for products and services from fintech firms and large tech companies will only increase as more consumers become familiar with new digital offerings. This is especially true for younger consumers, who have grown up with digital devices. More and more, people will get annoyed when they’re forced by bank policies and processes to use non-digital channels for everyday banking business, states the Bain research. This includes rudimentary transactions as well as being able to open new accounts or apply for loans.

Playing Catch-Up in Race for Digital Supremacy

At a time when some of the most complex interactions, such as starting a business, applying for an auto loan or home mortgage, sending money overseas and building an investment portfolio have been digitized, it is more important than ever for traditional banks and credit unions to digitize entire engagements, especially the opening of basic banking accounts. This will take a complete revamping of most banking websites, mobile banking apps and back office processes.

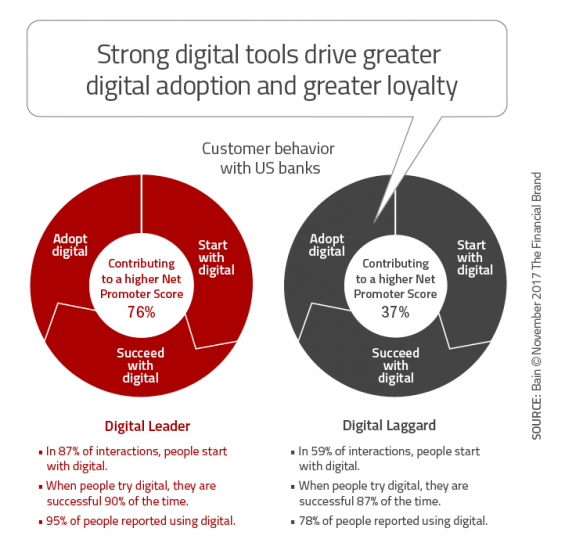

Migration to digital makes good financial sense. According to Bain, “Routine transactions that require bank staff not only cost 20 times more than those done online or through mobile, but consumers also prefer to handle routine banking business digitally.” And while the migration to mobile banking and the use of some digital services have leveled off, there is still significant potential for additional cost reduction and satisfaction improvement.

For instance, while “self-serve” leaders in the Netherlands, Poland and Australia transact the vast proportion of their transactions without ever interacting with a human, 40% of U.S. respondents to the Bain research went to the branch teller at least once in the past quarter to make a deposit, compared with 21% using digital channels and 18% using ATMs. Even within geographic markets there is a significant gap between the leaders and laggards in the quest for digital optimization.

The lower costs and high customer advocacy for digital channels serving routine interactions create a virtuous circle as shown below.

Prioritizing for Digital Differentiation

Not all retail banking transactions are created equal. They include basic transactions such as checking a balance, depositing money and making a withdrawal to the more complex interactions, such as paying a bill, applying for a credit card, opening an account or even resolving a dispute. To compete with small fintech firms and large tech companies, financial institutions much digitize the basic and the more complex transactions, leveraging the historical customer and member insights to create personalized engagements. These are insights none of the fintech firms or large tech organizations possess … yet.

Organizations must remove steps, leveraging insights already known to simplify and remove friction from all processes. Traditional financial institutions also need to break down product silos and rebuild interactions around consumer needs. Cross-functional teams should be built to review interactions from the consumer perspective, knowing that each one requires a different blend of digital and human processes. In each instance, the key is to make the overall engagement as easy as possible for the consumer – instead of simply looking at the engagement from a cost reduction perspective. The best path may not be the most cost efficient, but may be the most effective for generating loyalty and long-term revenues.

![]()

Beyond transactions and customer engagement, the marketing of services also provides traditional financial institutions an opportunity to differentiate from the small fintech firms and large tech companies. This includes both the cross-selling of services through digital channels and the acquisition of new customers and members using improved targeting and retargeting techniques.

Bain found that 25-50%+ of services are bought at competing organizations to the customer’s primary bank (hidden defection). Credit cards, loans, insurance and investments are the most purchased categories at competing organizations, whereas the primary bank tends to keep a higher share of low-value deposit accounts.

According to Bain, “42% of ‘hidden defectors’ said they bought from a competitor bank because they received an offer or saw an advertisement. Only one-fifth were actively researching when they decided to buy the product. Just as striking, more than half would have purchased from their primary bank if the bank had made an offer.” In other words, targeted marketing, using customer and member insights that competitors don’t have, can make the difference.

Going Beyond the Digital Banking Basics

It comes as no surprise that expectations are being impacted by the digital leaders that touch every part of a consumer’s daily life – from shopping at the corner store to booking an excursion around the world. As a result, simply ‘going digital’ is not enough to be competitive in the future. Today’s online and mobile banking apps fall short of most consumer’s expectations. The challenge will only increase.

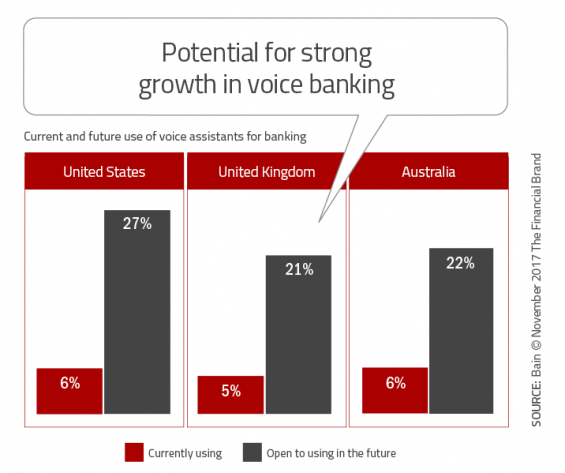

Banks and credit unions must begin to explore emerging technologies that leverage consumer data, advanced analytics and new digital tools, such a voice controlled digital assistants. According to Bain, 25% of U.S. respondents said they use voice assistants such as Siri, Alexa or Google Assistant on their smartphones or Alexa or Google Home at home (almost one-fifth of U.S. respondents). And, while only 5-6% of respondents currently use voice technology for their banking in the U.S., Australia and the U.K., between 20% and 25%+ are open to trying the technology for their banking in the future.

“Banks that master the digital basics will be able to further secure customers’ loyalty by quickly putting the new technologies to practical use in test-and-learn prototypes that can be improved in a few iterations and then broadly rolled out,” states the Bain research. In determining which new technologies should be rolled out, financial institutions must look at the options from a consumer benefit perspective, as opposed to simply as a way to reduce costs.

A Good Defense is a Strong Offense

The best way to prepare for the inevitable increase in competition that the continued expansion of banking services offered by Amazon, Google, PayPal, Facebook and an increasing number of start-up banks will bring is to be proactive in the development of personalized digital solutions. This will most likely involve new partnerships inside and outside of traditional banking organizations and a redefinition of what a banking ecosystem includes.

As succinctly stated in the Bain research report, “If banks don’t reorient their approach and radically accelerate their rate of progress, loyalty will suffer, and they will watch technology firms poach more business. Meanwhile, their economics will erode as too many routine transactions continue to flow through expensive branch and call-center networks.”

There is a great advantage in the customer and member insights that traditional financial institutions possess. The key is to apply these insights in ways that directly and positively impact the digital experience, similar to how large tech firms currently improve shopping, social, search and payments.