Investments in technology and innovation will have the potential to increase efficiency, manage evolving risks and meet consumer expectations that are required for sustainable success. According to a study from EY, banks and credit unions are working hard to become more digitally mature, transitioning from regulatory and transaction-driven organizations to innovation-led firms that will be in a better position to withstand future marketplace challenges.

But the most successful organizations will not move forward alone. “Banks must do less themselves and make extensive use of an ecosystem of industry utilities and a diverse range of partners to support investment, deliver better services, drive out costs, manage risks and protect their organizations,” states the report.

Other highlights from the report include:

- 59% of banks surveyed anticipate that their technology investment budgets will rise by more than 10% in 2018.

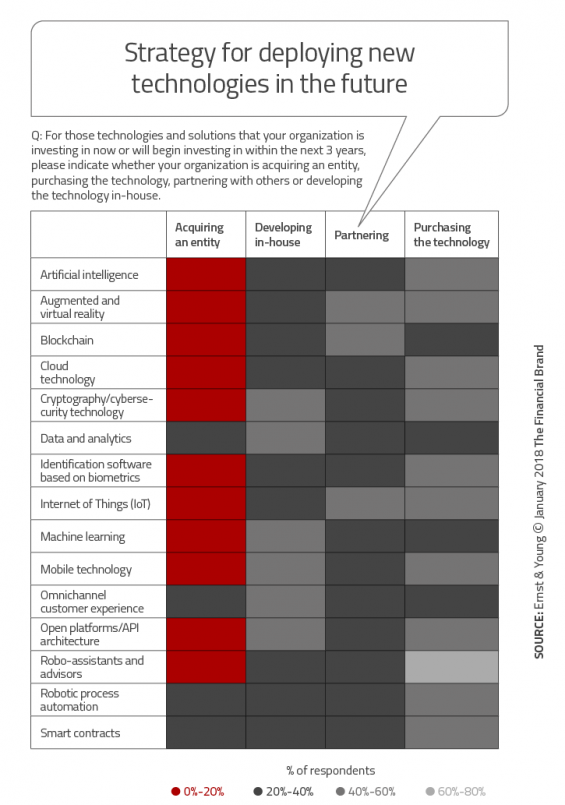

- For banking providers that are beginning to invest or increasing their investment in new technologies, 44% plan to purchase the technology from a third party, while only 17% plan to acquire an entity to onboard the technology.

- 70% of banks cite strengthening their competitive positioning as a key reason for investing in technology by 2020.

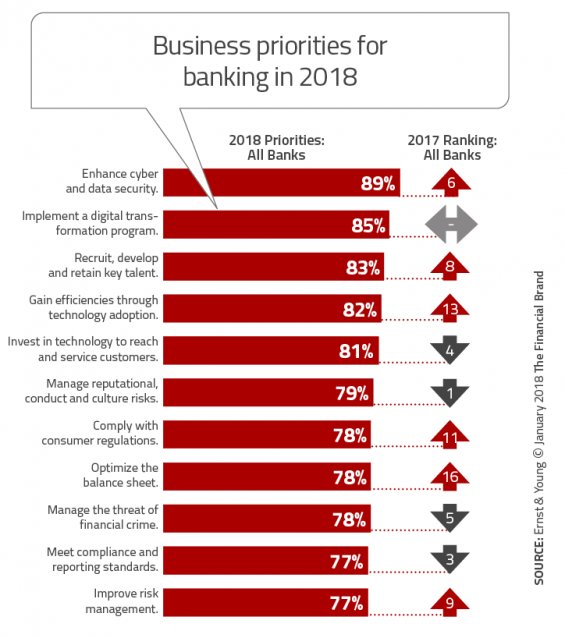

- Enhancing cyber and data security is the number one priority for banks, with 73% of banks planning to invest in technology to mitigate cybersecurity threats, supporting enhanced cyber and data security as a business priority.

- Recruiting, developing and retaining key talent (83%) also garners significant attention as banks strive to integrate cyber experts into their organizations amidst a skill set shortage.

Poised for Change

Many financial institutions believe the worst of times are behind us, with capital positions improved at organizations of all asset classes. At the same time, while the cost of compliance is significantly higher than before the banking crisis, there is reason to believe the cost of regulation has stabilized and will decline due to changes made by most firms.

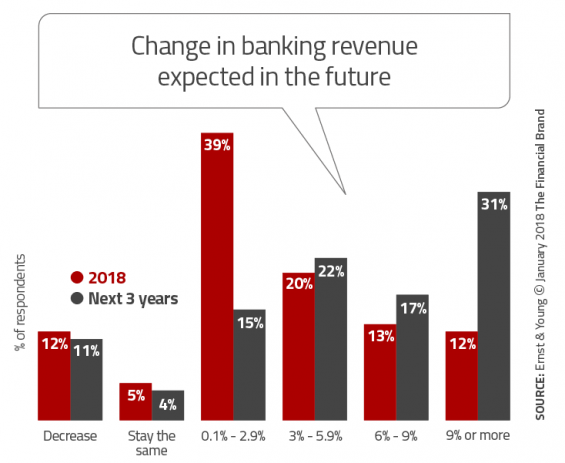

This has lead to the majority of bankers surveyed by EY expecting revenues and profitability to improve in the near term (12months – 3 years). This expectation of higher revenues has many firms considering larger capital investments in core systems, purchasing assets and entering into partnerships or joint ventures.

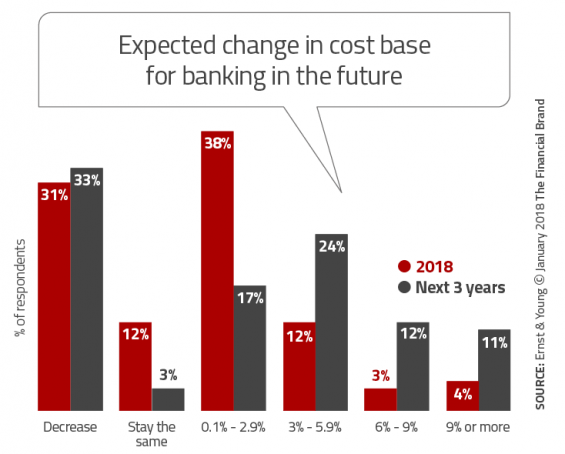

Despite this optimism, there could be storm clouds on the horizon if significant changes in business strategies are not embraced. These strategies include those that focus more on technology and innovation. In addition, while almost all organizations have reduced their cost structure, the cost base of legacy financial services organizations still exceed those of fintech and big tech firms by more than 25, according to the EY research. This disparity can’t continue.

Read More: Thrive or Survive? Tech Strategies Will Determine Banks’ Future

Accelerating Competition

Consumer demand for improved delivery of financial products and services is far outpacing the ability for traditional financial institutions to deliver these experiences. The expectations are being set by new market entrants, including digitalbanks, fintech firms, big tech organizations, e-commerce and telecommunications firms, and even platform banking providers.

Consumers like fintech offerings primarily because the solutions are simpler, more convenient, more transparent and more readily personalized. In other words, they have the advantages delivered by other digital industry leaders. For example, adoption of fintech firms as providers of money transfer and payment services rose from 18% in 2015 to 50% in 2017 according to EF, with 65% of consumers anticipating they would use such services at some point in future.

These challenges will not go away in the future and the consumer will no longer accept their financial services organization playing ‘catch up.’ This is why so many Millennials and Gen Z consumers are selecting one of the ‘Big 5’ banks as their primary financial institution – they want the newest and best in digital solutions.

Shifting Business Priorities

The survey revealed that enhancing cybersecurity has become the top priority for banks in the coming year. This should not come as a surprise given the massive breaches experienced in and out of financial services in 2017. Adding to this challenge will be new problems, such as how to find the right talent to fill both cybersecurity and advance analytic positions. Another major shift in priorities was seen in the desire to increase efficiency through new technologies.

Investments in Technology No Longer Optional

Financial institutions of all sizes must seriously consider becoming more digitally mature, investing in back-office processes and infrastructure as opposed to front-end tactical projects that only impact the consumer experience on a superficial level. This will require banks and credit unions to build from within and partner externally to become more digitally enabled. Some of this shift is seen when bankers were asked about technology investments in the coming year.

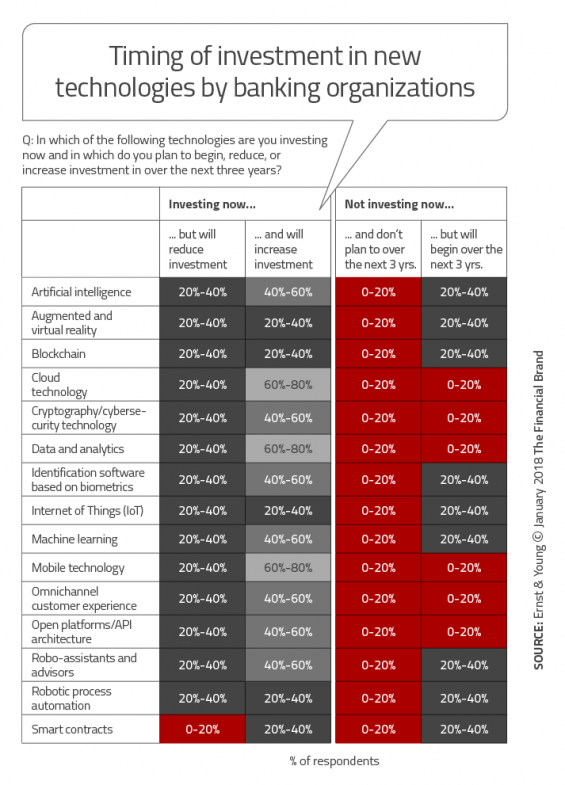

The top 4 reasons behind investment in technology in 2018 were, strengthen competitive positioning and grow market share (70%); acquire, engage and retain customers (67%); generate cost savings and operational efficiencies (62%); mitigate cybersecurity threats (58%). When firms were asked about the timing of technology investments, artificial intelligence, cloud technology, data and analytics and mobile technology received the most focus.

Responses revealed that few banks currently consider themselves as either maturing or a digital leader; however, more than

60% — the largest organizations — aspire to be one of the two by 2020. Despite this ambition, few organizations will achieve digital maturity on their own.

According to EY, “Digital maturity also means that banks have a clear ambition for the type of organizations they want to become, a plan to get there and, critically, enough self-awareness to understand that they can’t do it alone. Implementing this ambition requires banks to step outside both traditional lines and agile lines of project management, and define new best practices for bringing about innovation-led change in their organizations.”

Banks that are investing or beginning to invest in new technologies over the coming three years are adopting multiple approaches to onboarding the technologies’ capabilities. By availing themselves of a new ecosystem of technology providers, incumbent banks will benefit from nimbler innovation.

Unique Opportunity for Banking Industry

Similar to how a squirrel will collect food during the warmer months to ensure survival during the cold winter, financial organizations have the opportunity to use the positive performance and optimism today to be better prepared for the inevitable downturn expected due to increasing market pressures.

It is time for banks and credit unions to protect against the vulnerabilities caused by digital disruption. ” Banks that actnow to embrace an era of innovation-led change and deliver leaner, more scalable and digital business models can deliver

sustainable double-digit returns, even through the gathering storm,” concludes EY.