In the 7th Annual Innovation in Retail Banking Report from Efma and Infosys Finacle, which surveyed over 100 retail banks around the world, approximately three quarters (72%) regarded the threat from technology companies, start-ups, retailers and/or telecom players as high or very high.

In response to this perceived threat of disruption, legacy banking organizations are looking at fintech firms in a new light as we discussed in our article. Possibly more important, however, has been the continued global investment by banking firms in the innovation process overall since 2009.

Innovation Investment Trends

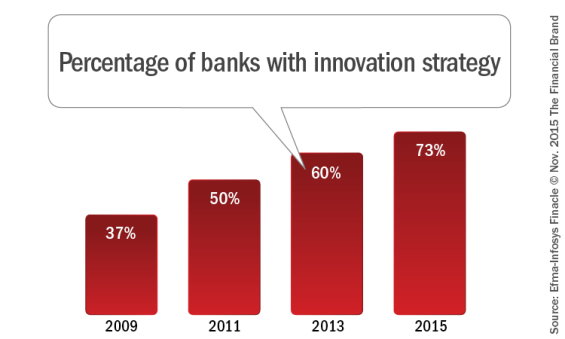

The proportion of banks with an innovation strategy (defined as having clear objectives, processes and measures of success for innovation) has increased from 37% in 2009 to 73% in 2015. When viewing the commitment to innovation from year to year, the proportion of banks increasing their innovation investment over the previous year was 15% in 2009, increasing to 84% in 2015. The biggest increase in commitment to innovation occurred in the period from 2009 to 2011, but there has still been a steady increase in this measure since 2011.

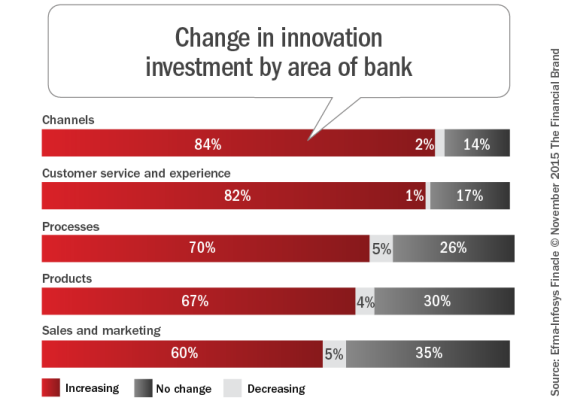

Similar to what was found in the 2014 Innovation in Retail Banking Study, the percentage of banking organizations increasing investments were the most pronounced in the categories of ‘Channels’ (84% in 2015 vs. 89% in 2014) and ‘Customer Service and Experience’ (82% in 2015 vs. 78% last year). While the relative importance of the different areas has changed very little in the last few years, there does appear to be a slight shift in emphasis from channels to customer experience since 2014.

The 2015 survey found a significant divergence in the overall innovation objectives being set by banks worldwide. While 45% indicated a desire to be an ‘innovation leader’, 36% were comfortable being a ‘fast follower’. Interestingly, both of these percentages were lower than last year, as was discussed in our 2014 article on the Efma study. As was noted by this year’s report authors, “Being a fast follower is not necessarily a bad strategy as the first to market is not always the most successful in the long term and you can learn from the mistakes of others.”

According to Patrick Desmarès, Secretary General, Efma, “This year’s global retail banking study demonstrates that banks are eager to innovate, develop formal innovation practices, and increase their involvement with start-ups. This is a step in the right direction, but retail banks must be confident about the value of their innovation investments.”

Michael Reh, Executive Vice President and CEO (Designate), EdgeVerve added, “Digitalization continues to massively shake the business foundations of ‘brick and mortar’ banking institutions. Banks need to proactively disrupt themselves and explore working with innovative start-ups to accelerate change and develop a leading edge in a competitive market. To achieve this, a dual strategy will be critical. Banks need new capabilities to help their businesses grow in new ways. They also need to renew their existing systems, opening them up to benefits of mobility, analytics, cloud computing, and connected systems.”

The Best of Banking Innovation

I was fortunate enough to moderate the two-day Efma Innovation Summit and to be the keynote speaker for Efma’s Global Banking Innovation Awards sponsored by Accenture. More than 200 financial institutions from 59 countries submitted 500 case studies of innovations within 10 categories: Customer Experience, Digital Distribution, Physical Distribution, Digital Marketing, Best New Product or Service, Best Innovation in Payments, Big Data & Analytics, Sustainable Business, Most Disruptive Innovation, and Global Innovator of the Year.

I was fortunate enough to moderate the two-day Efma Innovation Summit and to be the keynote speaker for Efma’s Global Banking Innovation Awards sponsored by Accenture. More than 200 financial institutions from 59 countries submitted 500 case studies of innovations within 10 categories: Customer Experience, Digital Distribution, Physical Distribution, Digital Marketing, Best New Product or Service, Best Innovation in Payments, Big Data & Analytics, Sustainable Business, Most Disruptive Innovation, and Global Innovator of the Year.

”It’s interesting to note that since we launched this award program, many of the innovators recognized by these awards in previous years were from emerging markets.”

— Piercarlo Gera, global managing director of Accenture Distribution and Marketing Services

The winners were selected by a combination of votes from a panel of judges comprised exclusively of senior retail bankers from around the world and online votes from Efma members. Between the presentations done by banks from each continent during the innovation summit, and the recap of winning innovations presented in conjunction with the awards ceremony, it is clear that there are banking organizations globally that have a culture and commitment to innovation. As has been the case at many banking innovation awards events over the past several years, several winners were from emerging markets.

“Innovation is the only way for banks to succeed in an industry that is undergoing a profound transformation, and it’s interesting to note that since we launched this award program, many of the innovators recognized by these awards in previous years were from emerging markets,” said Piercarlo Gera, global managing director of Accenture Distribution and Marketing Services. “This new breed of banks is made of players that invest in digital innovation and are making real impact in terms of customer experience enhancement.”

This year’s winners of the Efma Global Innovation Awards were:

- Denizbank, Turkey – Won the Global Innovator of the Year award for its digital banking model, which includes Facebook banking; Direct Message, which accepts credit applications through Twitter; and its FastPay mobile wallet application. Denizbank was also a winner of the Internal Process Improvement award at the BAI Infosys Finacle competition.

- Idea Bank, Poland – Won two awards – the Most Disruptive Innovation and the Digital Distribution award – for its Idea Cloud, Europe’s first banking cloud. Idea Cloud enables the bank’s small- and medium-sized enterprise clients to administer accounts, payments, documents and client data – as well as conduct ebanking – from a single cloud platform. Idea Bank also won the Innovation in Payments award at the BAI Infosys Finacle competition.

- mBank, Poland – Won the Digital Marketing award for its real-time marketing platform, which enabled the bank to identify an additional 300,000 sales leads per month by analyzing card transaction, Web traffic and geolocation data about its customers and presenting relevant offers to them based on that data.

- Allied Irish Bank, Ireland – Won the Customer Experience award for eMortgage, the first Irish market digitized end-to-end mortgage offering, enabling customers to complete applications, obtain loan approval and upload and sign documents online.

- Intesa Sanpaolo, Italy – Won the Physical Distribution award for its paperless branch model, which digitally produces and stores the bank’s paper documents, minimizes customers’ paper documents, reduces storage costs and enables digital signatures.

- KBC Securities, Belgium – Won the Best New Product or Service award for Bolero Crowdfunding, a crowdfunding website enabling startups and established businesses to obtain financing from investors. Bolero is the bank’s online stock trading platform.

- POLSKI STANDARD PLATNOSCI, Poland – A consortium of several Polish banks, won the Best Innovation in Payments award for its mobile payments standard, which generates a digital code enabling mobile payments, ATM withdrawals and point-of-service payments by phone, and online payments.

- Nedbank, South Africa – Won the Big Data & Analytics award for Market Edge, its data analytics tool that enables merchants to gain insights into their customers’ shopping behaviors using a Web-based platform that provides data on customers’ card transactions, income segment and demographics.

- ICICI Bank, India – Won the Sustainable Business award for its digital village initiative in Akodara, which allows residents to open savings accounts without submitting physical documents, transfer funds by mobile phone and pay for goods without cash. The bank is also digitizing school records and providing digital access to telemedicine, which gives villagers remote access to health care.

Patrick Desmarès, Efma’s secretary general, said, “As we reviewed the 500 innovations submitted this year, we realized that banks are finally entering the age of customer-driven innovation. At a time when competition is intense, banks must offer relevant, personalized and seamless experiences across channels to attract and retain customers. The winning institutions are innovating to provide a better customer experience and develop stronger customer relationships.”

“This year’s winners confirm that banks in all corners of the globe are responding to the universal rise of – and fully embracing – digital, which is absolutely critical today given changing customer behaviors, new regulations and emerging competition from new entrants,” said Gera. “Like with our Fintech Innovation Labs , our objective with this award program is to nurture and foster digital innovation in financial services.”