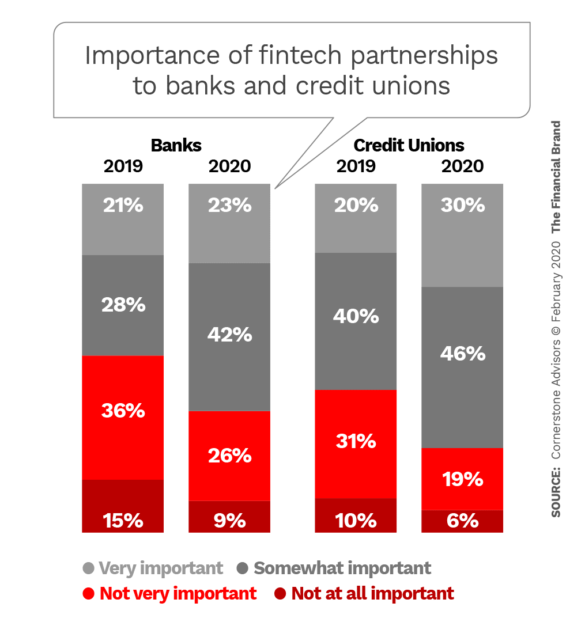

Significantly more banks and credit unions are saying that forming working relationships with fintech companies will be a priority in the year ahead, according to a Cornerstone Advisors survey.

Those fintech relationships may take the shape of partnerships, collaborations or investments by the financial institutions in the tech players, and seem motivated by both necessity and perceived opportunity. Tapping third-party expertise to provide digital account opening capability — increasingly seen as table stakes to keep doing business — represents a continuing factor in this search for allies, but added to this is the desire to find innovative new products and services to sell.

This trend comes at a time when many banks and credit unions are interested in emerging technologies like artificial intelligence and application programming interfaces to serve their renewed interest in consumer financial services and other needs. However, progress implementing the technologies has been slower than expected. Some banks and credit unions may be looking to short-cut the evolutionary process, using affiliation with a fintech in order to benefit quickly from the fintechs’ advanced technologies.

These conclusions come from a review of the findings in the latest edition of Cornerstone’s “What’s Going On in Banking” study. The consulting firm surveyed 300 senior executives at mid-sized financial institutions, including banks (52%) and credit unions (48%), with the focus on business plans for the year ahead and the role technology would play in implementation of those plans.

Teaming Up with Fintechs Higher on Execs’ Priority Lists

The survey found that 65% of banks and 76% of credit unions want a fintech affiliation in 2020, up from 49% and 60%, respectively, in 2019. For purposes of this study, fintechs include solely business-to-consumer and business-to-business startups — not established companies such as mainstream core system vendors.

Cornerstone dug into both why each type of institution seeks fintech affiliations and what purposes they want the affiliations for.

Regarding the first, Steve Williams, the firm’s president and co-founder, suggests this: “Banks and credit unions are acknowledging that fintechs often have better design capabilities than what exists at banks or their major industry vendors. They see partnering as very much a chance to ‘bolt in’ a better customer experience to their legacy back end in a time frame that can allow them to stay competitive.”

More specifically, among banks the objectives rank as follows, according to those who rated each as a very important priority:

- Improve customer experience 77%

- Create new capabilities or competencies 51%

- Strengthen existing core competencies/competitive positions 48%

- Reduce operating expenses 44%

- Reduce fraud 37%

- Expand product line 36%

- Reach new consumer segments 29%

- Expand geographic reach 22%

Among the credit unions, the ranking order differed somewhat, perhaps reflecting credit unions’ traditional focus on consumer financial needs:

- Improve the member experience 81%

- Strengthen existing core competencies/competitive positions 56%

- Create new capabilities or competencies 54%

- Reduce operating expenses 41%

- Reach new consumer segments 33%

- Reduce fraud 31%

- Expand geographic reach 31%

- Expand product line 23%

Cornerstone explored both areas of current fintech affiliation and what institutions planned over the next two years.

Among the top three current areas of affiliation for banks are:

- Digital account opening 31%

- Fraud and risk management 28%

- Lending and credit 26%.

For 2020-2022, however, here are the top three bank priorities:

- New banking products 39%

- Payments 35%

- Lending and credit 31%

Among credit unions, the top three current areas of affiliation are:

- Digital account opening 39%

- Lending and credit 29%

- Fraud and risk management 28%

In 2020-2022, here is how priority stacks up:

- New banking products 44%

- Payments 43%

- Lending and credit 39%

Read More:

- Why Fintech Challengers May Not Conquer Banking After All

- Fintech Adoption in North America Lags Global Acceptance

- Innovation Lessons That Respond to Fintech Challenges

Behind the Numbers: Renewed Interest in Consumers’ Business

Something that has been exerting some gravitational pull on institutions’ fintech affiliation and technology decisions is a renewed interest on the part of banks in consumer financial services.

“Over the past few years,” the report states, “it was really beginning to look like mid-size banks were ceding the retail market to megabanks and credit unions. It looks like 2020 might be the year that community banks try to reclaim consumers’ banking business.”

This goes beyond gut feel. The consulting firm has hard numbers from its research indicating increased interest. For example, 56% of banks had high interest in mortgage lending, up from 33% in the 2019 edition of the survey. High interest in home equity loans rose to 39% in the new survey, versus 22%. High interest in auto lending hit 13%, nearly double 2019’s 7%.

What’s behind this shift? Ron Shevlin, Cornerstone Director of Research, points to three primary forces: the economy, demographics and lending realities.

The first and second are intertwined, in his view.

“The state of the economy is the best it’s been in a long time —and that means consumers are more confident in borrowing, and their improved credit scores mean they’re more credit-worthy,” says Shevlin.

Digging a bit deeper, he says that increased credit standing in part relies on demographics.

“The Millennial generation is what — 70 million strong?’,” he continues. “Over the past ten years, as half of them have turned from 20-somethings into 30-somethings, their life stages have changed. Their incomes are rising, as are their credit scores. This means greater demand for deposit and credit products.”

What Shevlin means by the third factor of “lending realities” is that most community banks rely heavily on consumers for the deposits that fund their commercial lending.

“This leaves them no choice but to put greater emphasis on consumer banking services,” Shevlin concludes.

Another factor is the industry’s ongoing consolidation. Mergers and acquisitions undertaken to build bigger, more efficient banks will change their nature over time.

“The newly larger players will have more scale in which to compete more effectively in the retail market,” according to Shevlin.

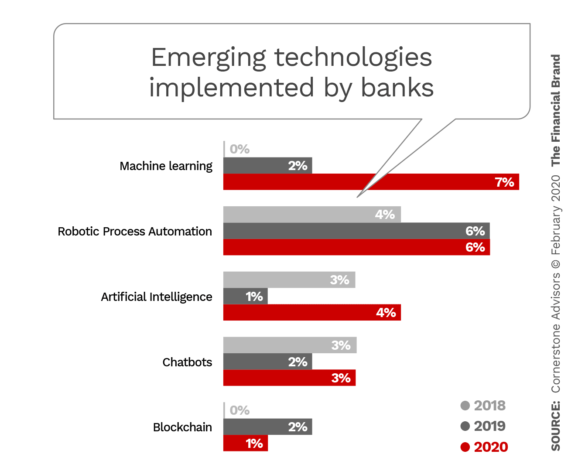

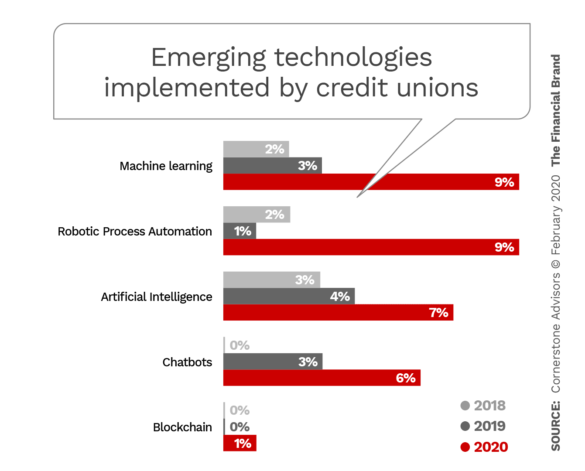

Use of Some Emerging Technologies Remains Fairly Slow

“2019 will go down as the year when pundits called for more transparency in artificial intelligence and machine learning,” the report states. “But when you see that the percentage of banks and credit unions that have deployed these tools are in the single digits, you begin to realize that there’s nothing to make transparent.”

Indeed, for some of the “usual suspects” among leading-edge tech, as shown in the following two charts, actual adoption going into 2020 remains barely noticeable, although credit unions are generally a bit ahead of banks in these areas.

“Most mid-size banks and credit unions don’t have the skillsets in house to address AI opportunities, and even if they did, they’d have to integrate with their vendor solutions,” Shevlin says. “Credit unions are ‘ahead’ — if that’s what you want to call it — of banks because they’re more retail-focused, and most of the well-thought-out use cases for AI are retail-focused.”

Another factor raised in the report is a concern that three out of five bank respondents had about AI in general. This is the likelihood, in their minds, that its use will be regulated in the future. This compliance layer could be imposed due to concerns over potential bias in the algorithms used, or the possibility that biases could be “learned” inadvertently, over time, by AI systems. Credit unions split over the possibility of regulation. Those who doubted that would occur tended to think AI is too complex for regulators of supervise.

Shevlin personally agrees with the latter group.

“Over the next decade, AI will be assimilated into existing bank (and other industry) applications and systems,” says Shevlin. “In effect, if will be difficult — if not impossible — to determine what part of an application is AI and what part isn’t.”

Read More:

- How Banks and Credit Unions Can Grow Deposits with AI

- How Personalization Strategies Can Backfire on Financial Marketers

There are additional technologies that are seeing higher rates of adoption and greater interest for 2020.

Status of emerging technologies among banks

| Have already deployed | Planning to invest and/or implement in 2020 | Have discussed at board or exec team level | Not on the radar | |

|---|---|---|---|---|

| Cloud computing | 32% | 22% | 37% | 9% |

| Application Programming Interfaces | 21% | 26% | 33% | 20% |

| Video collaboration/marketing | 21% | 21% | 35% | 23% |

| Machine learning | 7% | 13% | 36% | 45% |

| Robotic process automation | 6% | 11% | 24% | 59% |

| Voice technologies (e.g., Alexa) | 5% | 10% | 41% | 44% |

| Artificial Intelligence | 4% | 11% | 44% | 41% |

| Internet of Things | 4% | 4% | 43% | 48% |

| Chatbots | 3% | 13% | 43% | 40% |

| Virtual (or augmented) reality | 2% | 1% | 20% | 77% |

| Blockchain | 1% | 2% | 32% | 66% |

Source: Cornerstone Advisors survey of 300 community-based financial institution executives, Q4 2019

Status of emerging technologies among credit unions

| Have already deployed | Planning to invest and/or implement in 2020 | Have discussed at board or exec team level | Not on the radar | |

|---|---|---|---|---|

| Application Programming Interfaces | 53% | 24% | 14% | 9% |

| Cloud computing | 47% | 29% | 18% | 6% |

| Video collaboration/marketing | 20% | 33% | 35% | 12% |

| Machine learning | 9% | 22% | 47% | 22% |

| Robotic process automation | 9% | 19% | 34% | 39% |

| Artificial Intelligence | 7% | 19% | 54% | 19% |

| Chatbots | 6% | 23% | 54% | 16% |

| Voice technologies (e.g., Alexa) | 5% | 24% | 49% | 22% |

| Internet of Things | 3% | 13% | 46% | 37% |

| Blockchain | 1% | 7% | 51% | 41% |

| Virtual (or augmented) reality | 1% | 4% | 34% | 60% |

Source: Cornerstone Advisors survey of 300 community-based financial institution executives, Q4 2019

And for retail bankers and marketers specifically, there are three key areas where Cornerstone probed for future plans.

Selected bank and credit union tech plans, 2019-2020

| Modify/Improve | Add New or Replace | |||

|---|---|---|---|---|

| 2019 | 2020 | 2019 | 2020 | |

| Consumer Digital | ||||

| Digital account opening | 39% | 46% | 36% | 33% |

| P2P payments | 25% | 40% | 35% | 29% |

| Mobile banking | 46% | 56% | 19% | 17% |

| Online banking | 48% | 50% | 17% | 18% |

| PFM | 19% | 22% | 14% | 16% |

| Digital bill payment | 29% | 40% | 12% | 11% |

| Remote deposit capture | 27% | 35% | 11% | 11% |

| Marketing | ||||

| CRM | 32% | 32% | 25% | 21% |

| Marketing automation | 32% | 38% | 16% | 18% |

| Profitability/pricing | 29% | 33% | 9% | 8% |

| Analytics | ||||

| Reporting/dashboard | 52% | 55% | 16% | 21% |

| Data warehouses | 39% | 42% | 15% | 17% |

| Data analysis business intelligence | 41% | 51% | 15% | 18% |

| Predictive analytics modeling/decisions | 35% | 44% | 15% | 17% |

| Fraud/risk analysis | 50% | 62% | 12% | 12% |

Source: Cornerstone Advisors survey of 300 community-based financial institution executives, Q4 2019