Retail bankers could easily conclude that the branch system, though changing, is still working well. After all, deposits have risen sharply since 2007-8 and the total number of bank and credit union branches has fallen only modestly from 2008’s peak.

However, new data from Mintel calls that conclusion into question.

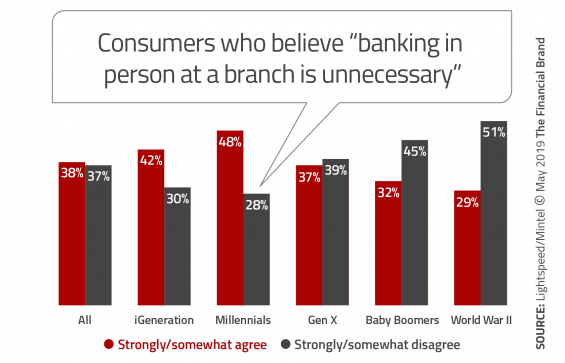

A survey conducted by Mintel in cooperation with Lightspeed (now Kantar) found that 38% of consumers now feel brick-and-mortar interactions are no longer necessary while 37% believe in-person banking still has value. The rest (24%) were undecided.

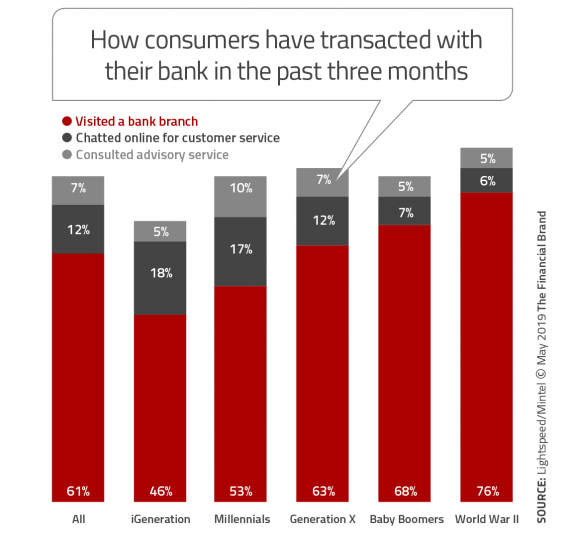

Sentiments about whether a branch is “necessary” are not the same as actually using one. Mintel found that overall 61% U.S. consumers had visited a banking branch within three months of the survey. This varied by generation, ranging from 46% of what Mintel calls the “iGeneration” (Gen Z) to 76% of the “World War II” generation (sometimes called the “Silent Generation” or “Pre-Boomers”).

Further, overall satisfaction with banking providers is high. 85% of all respondents agree they are satisfied with their current provider — 50% of them strongly agreeing, according to Mintel. In addition, 87% of consumers surveyed have a checking account including 72% of Gen Z respondents. As good as all that is, a potential danger for traditional financial institutions is mistaking that high level of satisfaction as an endorsement of the status quo.

Among other indications to the contrary, 20% of all consumer respondents use an online-only financial institution, according to Mintel. The data reveal that these online-only bank users also frequently use one or more traditional institutions.

In addition, separate research from IDology of about 1,500 U.S. online-service-using consumers found that 20% registered for new accounts exclusively on a mobile phone, up from 10% the previous year. While that figure is not banking specific, it does indicate the quickening pace of the digital transformation of commerce.

The Risk of Alienating Branch Customers is Real

Mintel states in its report that retail banking providers are now at an inflection point “where the importance of the very hallmark of the traditional bank — the bank branch — is being seriously called into question.” Even so, banks and credit unions must “delicately navigate the cost-benefit analysis of reducing overhead,” the research firm adds. If they move too abruptly they risk alienating remote or technologically disinclined consumers in pursuit of younger digital-native consumers.

The alienation point isn’t raised often, but is a thorny challenge. A study conducted by The Harris Poll on behalf of Kasasa found the that the top reason (56%) why consumers would not consider opening a checking account with a local financial institution is limited branch and ATM locations. Lack of up-to-date-technology was also a significant deterrent, but much lower (22%), with a slightly higher percentage of Millennials saying this than older generations.

On the other hand, when Mintel probed what would prompt consumers to switch their primary financial provider, only 18% said “Fewer branches.” It was the fifth most-cited reason. (The top two reasons were “increase in fees,” 58%, and “poor customer service,” 52%.)

Clearly the views of both branch lovers and digital lovers are important for the foreseeable future. “Branches won’t go away full stop,” Mintel Financial Services Analyst Christopher Shadle tells The Financial Brand. “It’s a very polarizing issue split fairly evenly among all generations. Some people love that personal touch and feel more secure knowing that their bank is an actual physical place in the world, whereas plenty of other people are completely fine digitally, putting those things on a cloud and interfacing physically as infrequently as possible.”

Read More: Branches vs. Digital: Hitting the Retail Delivery Sweet Spot in Banking

Low Consumer Interest in Advisory Services

Much has been written and said about how bank and credit union branches will transition to primarily advisory and consultative roles as branch transaction volume continues to decline. But can they deliver on this promise? Peak Performance Consulting Group President David Kerstein has written that very few financial institutions have brought their branch, call-center, and field sales teams up to the necessary skill level to fulfill this vision.

Mintel’s survey confirms that few consumers are using banks for advisory services. The question didn’t specify types of advisory service, Shadle says, but left that open to the respondent’s interpretation. It is possible, he states, that people might not consider the retirement and investment advice they are getting through the investment arm of a bank, which may have cannibalized some responses. Still, the numbers are very low — less than 10% of all consumers reported using their bank’s advisory services in the past three months.

“As banking brands continually reassess their return on investment for various business functions,” the analyst writes in the report, “some firms may come to the conclusion that traditional advisory services are too costly an offering for how little they are utilized. Banks must seriously re-evaluate what the future of the branch may hold, as most of the traditional reasons for visiting become replaceable or remotely available through technology.” Shadle states that “perhaps the advisory experience of the 21st century is now better disposed to be delivered through FaceTime or Skype than in person.”

Read More: Trends in Branch Design From Banks Around The World

Digital Banking: Bright Spots and Challenges

While satisfied overall with their bank or credit union, the majority of consumers do not apply the term “easy-to-use” to any retail banking services that Mintel listed in the survey. Less than half (47%) actually think using an ATM at a bank branch is easy, and that’s the highest-ranked service. Shadle points out, however, that people tend to recall problems with products and services, not when things go well.

Online banking was also considered easy-to-use by 47% of consumers, and mobile banking apps scored 41%, just below drive-through ATMs at 43%. So the four banking services rated easiest-to-use in this survey were all digital.

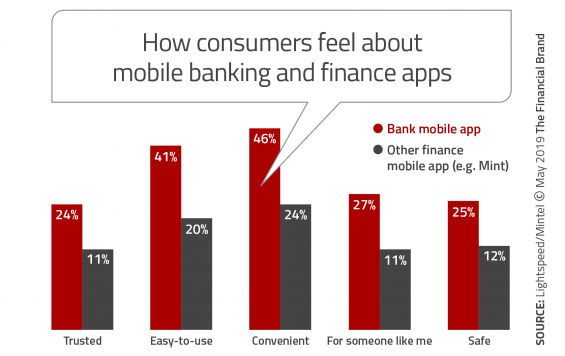

Mintel probed further about mobile banking apps in particular, uncovering a mixed picture. On the plus side almost as many consumers had used a mobile banking app in the previous three months as had used a bank ATM (46% versus 51%). Also, the same percentage of consumers (46%) consider mobile banking apps “convenient.”

On the other hand, given the popularity of mobile banking apps, it’s surprising that only a quarter of consumers surveyed consider a mobile banking app “trusted” and “safe.” At least mobile banking apps have a clear edge over nonbank finance apps like Mint, as the results show.

Several factors are likely reflected in these numbers, Shadle maintains. First, mobile banking apps are a fairly recent tool for conducting banking. Second, the countless examples of data breaches and compromised personal identities, as well as Facebook’s well-publicized data privacy troubles are constant reminder of consumers’ vulnerability.

“The low numbers for trust and safety could be less an indictment of financial institutions and more of the data security environment as a whole,” Shadle observes. Still, Mintel believes this area represents an opportunity for banks and credit unions that deliver a mobile banking experience that is faster, more secure, and more convenient.