Banks and credit unions have been struggling to strike the right balance between digital and physical channels for the better part of two decades. Ever since online banking emerged in the late 90s, retail financial institutions have wrestled with their retail delivery models — a problem that was exacerbated with mobile banking when the iPhone debuted in 2007.

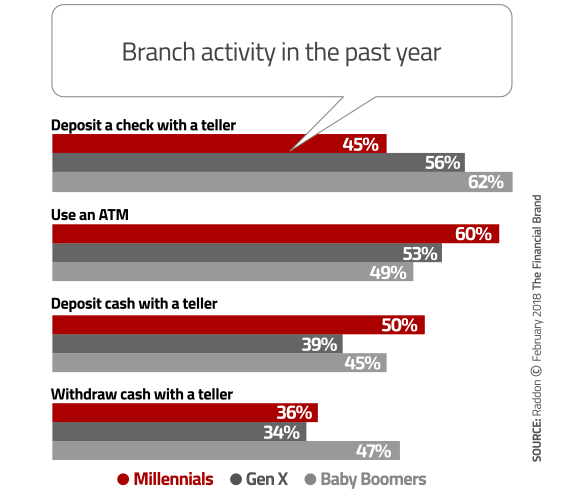

According to a study by Raddon, a Fiserv company, the vast majority of consumers have visited a branch in the past 12 months, mostly to deposit checks with a teller. Somewhat surprisingly, 42% say they visited a branch to withdraw cash from a teller — something that can done faster at an ATM.

![]()

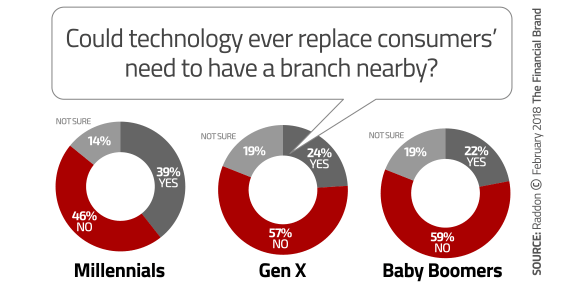

Despite all the talk about turning branches into consultative sales hubs, it doesn’t look like it’s actually happening. Consumers are still using branches for ordinary transactions rather than activities such as account opening or getting financial advice. So it seems obvious that branches are here to stay. In fact, most consumers — particularly those whose use a community bank as their primary institution (70%) — don’t believe that digital channels will ever negate the need for branches.

Branches, Digital, or Both?

Assuming branches are staying, then how much should you invest in them? The answer varies for each bank or credit union based on their target audience(s). Raddon suggests segmenting your consumer base by both behavioral habits/preferences and by generation.

Using consumers’ responses to questions about their financial behaviors, Raddon breaks consumers down into three broad groups: Conventionals, Digital Consumers and Pioneers.

Conventionals (35%) — Consumers who prefer to conduct their banking business face-to-face at traditional providers, such as banks and credit unions. They believe in banks, although they are aware that differences exist among institutions. Most importantly, they are distrustful of technology companies entering the banking space to provide financial services.

Digitals (35%) — Consumers who prefer traditional financial providers, but avoid face-to-face transactions in favor of electronic or digital channels. While they believe that technology companies will impact financial services, they feel they will still have to rely on traditional providers in the future.

Pioneers (30%) — Digitally focused, but they have a sunny outlook on the potential of technology companies. They are fairly ambivalent about banks; while they like to conduct business both face-to-face and digitally, they think all banks are the same. They see a future without traditional providers; they might use banks and credit unions, but they will not rely upon them.

Even among the 60% who say they like to bank with digital channels include a caveat that, hey, sometimes face-to-face is best. And depending on your institution’s market, the Conventional segment could make up a bigger percentage of your base than you might think, with more than one-third saying that they prefer to conduct most of their banking in-person.

If You Close It, Will They Still Come?

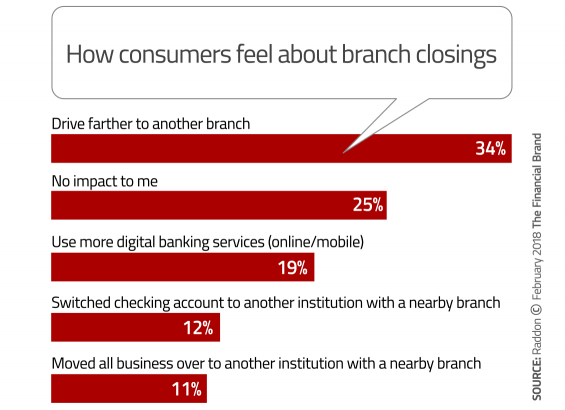

Consumers — even those Raddon classifies as Digitals and Pioneers — still visit the branch, although the frequency of branch visits is declining. But what happens if the local branch goes away? If their branch closed, about one-third of consumers said that they would just drive a bit further to the next closest branch. Another third will just up their usage of ATMs or online or mobile banking. But traditionalists and older consumers may switch to a financial institution with more convenient locations, with 18% saying that they would move all of their accounts to another bank or credit union.

What consumers said they would do *if* their local branch closed and what they *actually* did when a branch closed was generally aligned. However, some took more action than they thought they would. Driving further to another branch apparently wore a certain percentage down, and more than twice as many consumers ditched their financial institutions than hypothetically said they would.

Four Trends to Keep an Eye On

Raddon identified a couple of trends that can help you find the retail delivery sweet spot — how to balance your investment in branches versus digital.

1. P2P payments are growing in importance. Facebook is giving way to Snapchat. Twitter is giving way to Instagram. And for the younger generation, PayPal is giving way to Venmo. There’s a sharp drop off in Millennials using PayPal in favor of Venmo. And while banks and credit unions need to be aware of changing consumer preferences—there is also opportunity at hand in the P2P space, with 21% of Millennials (and Gen Xers) saying they use a financial institution-sponsored P2P payment service.

2. Wearables for banking. As cool as the Apple Watch may be, not that many consumers own one. According to Raddon, only 7% of survey respondents own a smartwatch. Those are small numbers, but of the consumers who do own one, 28% say they use it for banking and 20% say they use it to view checking account balances. These numbers could spike sharply upward if (when?) the world migrates to digital payments on a wide scale basis. Someday soon, people could be swiping watches instead of plastic credit cards.

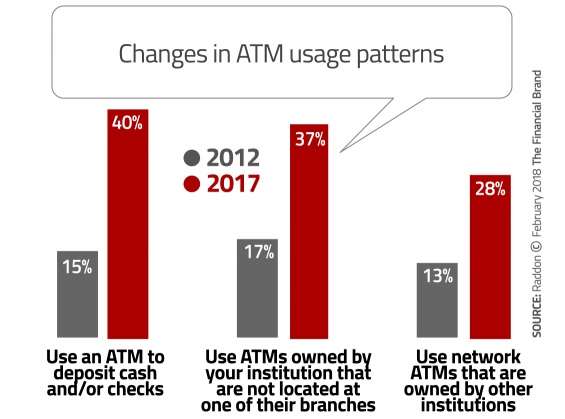

3. ATMs on the rise. ATM usage is up. Consumers are relying on ATMs — both those located in your branches as well as those owned by other banking providers — in increasing numbers. More than twice as many consumers hit a foreign ATM in 2017 versus 2012. And the number of consumers using their institution’s ATMs outside the branch also doubled in five years.

4. Appetite for new types of checking accounts. Consumer checking account expectations are changing. Free checking accounts have just about disappeared — and consumers don’t seem to care, at least not as much as they did five years ago. In 2012, the most wanted features for primary checking accounts were no service charges and free checks. In 2017, consumers say that the most important features are having a mobile app and only about a third say “free” is a coveted feature.

- Has a mobile app (41%)

- Free with direct deposit (32%)

- Free maintaining minimum balance (31%)

- Account pays interest (30%)

- Cannot be overdrawn because you can only spend funds in the account (12%)

Although the percentage of consumers with checking accounts has remained pretty stable over the last decade, there are a couple of checking account alternatives that are becoming popular with Millennials. One is the prepaid debit card. Millennials are twice as likely as other age groups to use these reloadable cards.

The other is a “no overdraw” account where you can’t write checks, but can use a debit card, online bill pay and mobile payments (including P2P transfers/payments). Again, Millennials were twice as likely as to use this account.

Granted, the actual usage of prepaid debit cards and no overdraw accounts is pretty small today. They are niche products, but they are also an educational opportunity says Raddon. And educating consumers can help you build loyal consumers.