People are used to effortless financial transactions these days: Paying tolls without stopping at a toll booth. Getting financing for a purchase just as they are checking out, without any long application form involved. And paying for all kinds of services — Lyft, DoorDash, Instacart, etc. — without ever having to pull out a credit card or cash.

It’s all part of the era of “invisible” banking, where people can go about their daily activities without having to think much, if at all, about the financial services component of any particular experience.

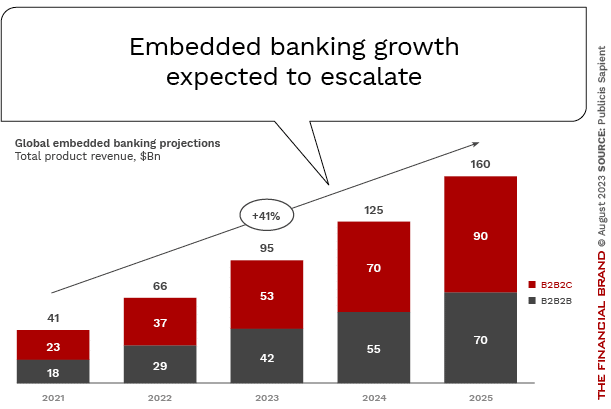

This trend — called “embedded finance” — is poised for explosive growth. The consulting firm Publicis Sapient projects that revenue from embedded finance will climb to $160 billion by 2025, nearly quadruple the $41 billion it generated in 2021.

A New Business Model:

Embedded finance is becoming an important way for people to consume financial services — making it a key strategic issue for banks.

Most of the early leaders in embedded finance are digitally native fintech challengers, in part because they have fewer regulatory constraints than traditional financial institutions. Payments and buy now, pay later offerings are the two areas of embedded finance where these players have gained the most traction.

But new use cases are popping up as more businesses look to adopt an embedded finance strategy. Interest is so significant that, according to EY, the firms driving this trend — including online marketplaces, retailers, manufacturers and software companies — will play an outsize role in influencing the future of financial services.

The rise of embedded finance threatens to undermine the most important sources of revenue for traditional financial institutions — from credit card transactions to lending of all kinds.

Banks and credit unions must adapt to a new way of doing business in response to this trend. The first step is to conduct a strategic evaluation to assess how they can best enable the emerging embedded finance ecosystem to drive their own growth.

Revenue Gain or Revenue Drain? Banks Face a Binary Choice

The threat is daunting: Embedded finance allows agile fintech players and platforms like Shopify to own the customer relationship. At best, it relegates traditional financial institutions to low-margin utility roles. At worst, it is possible to exclude them completely.

Consider, for example, that Apple Pay Later is currently being run on Apple’s own balance sheet. Though the tech giant partners with chartered banks like Goldman Sachs and Green Dot for other types of financial services, its buy now, pay later entry is an exception. This is notable because federal BNPL rules don’t exist, so Apple doesn’t have to get entangled in financial regulatory minutia to extend this form of consumer credit.

Thoughtfully embracing embedded finance gives financial institutions a fighting chance to reinvent themselves before it’s too late. By becoming banking-as-a-service providers, banks can find new customers and revenue streams via powering financial products inside the platforms of all types of nonbank companies.

Banks and credit unions also have a major advantage they can exploit in pursuing embedded finance: the established relationships they have with many businesses.

Some are already capitalizing on this advantage. Citibank has started promoting the concept of embedded finance to merchants it has as banking customers — and, importantly, it makes implementation easy.

Its Citi Retail Services unit now offers “Citi Pay,” an assortment of payment options that merchants can provide to their customers as part of the online shopping experience. Credit evaluations are nearly instantaneous. (Citi says merchants also will be able to offer these credit options at the physical point of sale in the future.)

Time is of the essence in developing an embedded finance strategy, though. Banks and credit unions are at risk of being disintermediated, and McKinsey estimates the negative impact on banking revenue could be as much as 50%.

Embedded Finance Tackles the Biggest Challenges Banks Have

Banks and credit unions embracing embedded finance will gain key competitive advantages in the following areas:

- Customer expectations: Digital experiences from the likes of Uber and Amazon have raised customer expectations for convenience and personalization. Embedded finance matches these new demands by delivering a financial service — whether that is a payment, a loan or something else — as a seamless part of an existing customer journey.

- Products and services: Standalone financial services interactions seem fragmented and friction-filled compared to embedded experiences. Banks risk losing relevance if they are doing business only with people who come to them directly for a specific service — especially given that, with increasing frequency, competitors will be at their fingertips right as they are about to make a purchase. People won’t even have to fill out an application. Instead of expecting customers to come to the bank, what banks need to do is go where the customers are. And that means adopting an embedded finance strategy.

- Fintech and big tech competition: Nonbank challengers are leading embedded finance innovation. With their nimble tech stacks, they can rapidly embed finance in customer journeys. Big tech platforms also leverage embedded finance, and they can do so at massive scale. More financial activity is poised to move outside of the walls of traditional banks and credit unions, and consultants warn that the margin squeeze could potentially be catastrophic.

- Customer insights: Traditional banks and credit unions will be missing out on valuable customer insights as more financial life occurs in embedded scenarios. Banking apps won’t capture key activities and associated revenue opportunities. Data and distribution advantages will accrue to platforms offering embedded financial services, not old-guard banking institutions.

- Brand loyalty: Without embedding, banks and credit unions will struggle for discoverability as financial activities vanish into platform experiences outside of traditional channels.

- Platforms: Transitioning from product-centricity to platform-centricity will position banks and credit unions to thrive. They will gain the speed, agility and ecosystems needed not only to take advantage of embedded finance, but to innovate into the future.

Read more:

- How Embedded Finance Is Blending Banking and Commerce

- The Future of Banking as a Service and Trends in Embedded Finance

8 Action Items: How Banks and Credit Unions Should Respond

Here are some ways financial institutions can strategically respond to the threats posed by embedded banking:

- Invest in technology: Launch embedded banking offerings via application programming interfaces, or APIs, to stay competitive. Overhaul technology architecture to be API-driven, cloud-based and modular. Legacy monolithic tech stacks inhibit fast and flexible embedding of financial services.

- Make selective acquisitions: Collaborate with or acquire embedded finance providers to quickly gain capabilities and credibility.

- Form ecosystem partnerships with nonfinancial platforms: Rather than viewing nonfinancial platforms as competitors, explore partnerships with them. Integrating financial services into these platforms allows banks and credit unions to expand their reach and tap into new customer segments.

- Focus on customer experiences. Become an orchestrator of financial experiences rather than a manufacturer of products. This enables participating in embedded ecosystems versus trying to own the entire value chain.

- Rethink the back office: Build organizational agility through DevOps teams, lean development and rapid iteration cycles. Match the speed of innovation seen in fintech and platform players.

- Embrace open banking: Open banking initiatives enable the secure sharing of customer data with third-party providers. By embracing open banking, financial institutions can foster innovation, create new revenue streams, and develop more personalized products and services.

- Target niche markets: Rather than competing directly with embedded finance offerings in broader markets, financial institutions can identify and target niche customer segments with specialized services and personalized offerings. Rethink brand positioning and marketing around enabling seamless financial experiences versus pushing products.

- Move from a ‘risk avoidance’ mentality to a ‘risk management’ mentality: Accept lower margins on commoditized embedded infrastructure services while pursuing differentiated premium offerings.

A mix of strategic partnerships, capability building, rethinking existing processes and products and transforming the organizational culture and tech stack are required for incumbent banks to thrive in the world of embedded banking.

Read more:

- Think Agile is Only for Tech Companies? Think Again.

- The Best Way for Banks to Respond to Embedded Finance

Examples of Banks with an Embedded Finance Strategy

Banking executives should view embedded finance as an opportunity to reinvent their core business, build new growth engines, and offer more interoperable products and services. For financial institutions with a proactive strategy, embedded finance can accelerate rather than undermine growth.

Here are some examples of traditional financial institutions that have introduced embedded banking solutions.

- JPMorgan Chase: By offering an embedded BNPL option for Chase credit card holders, JPMorgan retains its leadership position as consumers increasingly expect flexible financing.

- Citibank: Citi Pay quickly integrates into participating retail partners’ existing payment platforms. Customers of the retailer get more payment options, including revolving lines of credit and installment loans. The key to the ease of implementation is the use of APIs and standardized development kits, or SDKs.

- Wells Fargo: This megabank enables retail partners to embed its credit card application into their transaction flow. Through its co-brand credit card SDK and a set of APIs, Wells Fargo makes it easy for merchant partners to integrate and offer credit seamlessly within their own ecosystem.

See more coverage of embedded finance.