The well-known saying “Keep your friends close and your enemies closer,” has taken on a different twist in banking. The fintech upstarts that once were considered enemies, are now increasingly becoming co-collaborators, if not exactly friends. They hold the key for traditional financial institutions to seize on two rapidly expanding trends reshaping banking: embedded finance and banking-as-a-service.

According to new findings from Economist Impact, a unit of The Economist, many banks do not look at fintech upstarts as competitors anymore, but rather as potential partners to help build out their own digital capabilities. However, bank executives are seeing an increasing threat from embedded finance and BaaS services being offered by non-financial firms including technology companies and telecommunications providers.

“In some ways big tech has a bit of an advantage because they have that looser regulatory compliance area,” says Drew Propson, head of Technology and Innovation in Financial Services at the World Economic Forum, as quoted in the report. “Additionally, they can utilize data collected from various parts of their business whereas banks can primarily collect data through their financial services operations.”

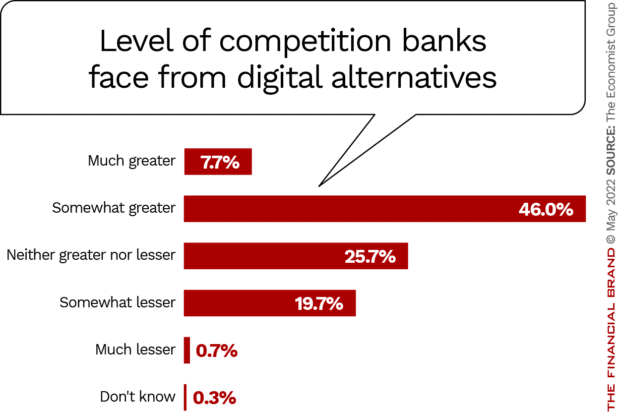

Just over half of the 300 C-suite bankers polled worldwide for the survey, commissioned by tech vendor WS02, said they have been facing “somewhat” or “much “greater” competition over the past three years from digital competitors.

Embedded Banking on the Rise

Pressure from non-financial companies will continue to grow, predicts McKinsey, as companies “of all types and levels of maturity — including retailers, telcos, big techs and software companies, car manufacturers, insurance providers, and logistics firms — are considering and preparing to launch embedded financial services to serve business and consumer segments.”

Simply put, embedded banking refers to payment or lending services that are provided directly to consumers by companies that are not financial services firms, according to a glossary prepared by Alloy Labs. Embedded finance encompasses financial services beyond payments and loans.

Banking, Simplified:

Embedded finance is growing because it gives consumers an 'all in one' experience instead of having to use several different financial apps.

“For customers, the appeal is ease of use: a small business can get a bank account from its accounting software, or a consumer can pay via the retailer,” says McKinsey. “Companies’ embrace of embedded finance … aims to retain customers and increase their so-called lifetime value.”

Read More: The Future of Banking as a Service and Trends in Embedded Finance

Banks Struggle with Digital Capabilities

Unfortunately, many banks and credit unions lack the capabilities to compete in this new world of embedded finance and the closely related banking-as-a-service business. In the Economist Impact survey, only a little more than a quarter (27%) of survey respondents say their organization has the necessary technology tools — “to a great or large extent” — to create new digital products and services internally or externally.

In addition, a primary obstacle to the development of improved digital services and products is insufficient understanding of consumer needs, according to 22% of the respondents.

Read More:

- Why KeyBank Believes ‘Embedded Banking’ Is the Future of the Industry

- How BaaS Turns Traditional Banks Into Digital Deposit & Loan Machines

- Two Big Trends That Will Change Banking Forever

The Potential of Fintech Partnerships

Perhaps ironically, partnering with fintech firms can help banks remain competitive against nonbanking companies that get into embedded finance. Backing that up, only 12% of bankers polled by Economist Impact reported increased competition from fintechs, while nearly half reported partnering with a fintech in the last year.

“Previously seen as a potential competitor to traditional banks, fintechs are now among the lowest-rated reasons for greater competition, indicative of a more symbiotic relationship between incumbents and upstarts, and a rise in partnerships to stave off non-financial firms,” the report states.

The “staving off” essentially means that a bank or credit union makes the strategic commitment to “join ’em rather than fight ’em.” By taking advantage of fintechs’ tech capabilities, the incumbent becomes the “bank in the background” for payment or loan services embedded in a non-banking product, getting a cut of the revenue stream. It’s much the same decision traditional institutions have been making about becoming a banking-as-a-service provider, leveraging their charter to provide insured deposits and other capabilities to neobanks.

Writing on the Wall:

Banks wonder whether revenue from embedding their products through partners would offset the potential loss of relationships. But if embedded finance continues to grow, they may have little choice.

McKinsey notes there have been several fintechs that have emerged specifically designed to partner with banks to intermediate BaaS and embedded banking relationships, citing names like Treasury Prime, Synctera, Unit, and Bond. While some banks are still reluctant to engage in partnerships with these or other fintechs, this stigma should be overcome in order to remain competitive, especially for banks that do not have massive in-house tech capabilities.

“Many banks are concerned that distributing their products through partners threatens their client relationships, but if end users begin adopting embedded finance in significant numbers, banks may have little choice,” McKinsey says. “The good news is that enabling partners to distribute banking products can be a low-margin, high-volume business for banks. Banks often struggle with their cost structures, which are frequently based on legacy technology and enabled through manual processes and operations.”

Listen In: How Banking-as-a-Service has Made Webster Bank Future-Ready

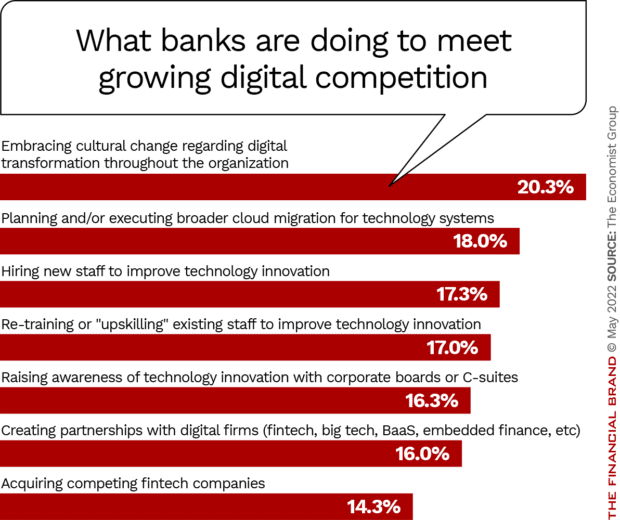

Creating a Digital Culture Within Banking

Banks and credit unions can remain competitive in an increasingly digital world by fostering a culture of innovation internally. in most cases this will require both hiring new staff as well as re-training or “upskilling” existing staff to improve technology innovation.

“Cultural encouragement is crucial,” says Nicole Sandler, Head of Digital Policy at Barclays, in the Economist Impact report. “It makes us better at understanding the needs of our customers and clients, and it creates a sense of belonging and value that enables our colleagues to perform at their best.”

Beyond collaboration with fintechs and creating an internal culture of innovation, the report advises traditional institutions to embrace new technologies such as APIs and cloud computing.

“Having a cloud strategy in place is fundamental to be able to adopt to market trends and interact with cloud-based businesses and providers,” the report states. “After that, analytical tools and AI and machine learning are the new systems that must be adopted.”

Ultimately, embedded finance and BaaS look likely to be here to stay and not a trend banks or credit unions can afford to ignore.

“BaaS may well be a land grab,” McKinsey concludes. “If so, banks will need to develop a BaaS strategy today, with a realistic understanding of their cost structure and the path to transformation. They should also clearly see the impact that a significant increase in customer demand for integrated banking experiences will have on their businesses.”