Have you ever wanted to buy a ticket to an event or for travel and realize that the pricing for the ticket differs based on the day, time or location of the event? Have you ever searched for a product or service online only to realize that the price of the product changed in the short time you contemplated the purchase? This is the power of ‘dynamic pricing.’

According to Crealytics, “Dynamic pricing is an e-commerce and retail strategy that applies variable pricing instead of the more typical fixed pricing. As more data is analyzed, optimal prices for goods or services are recalculated. The time between price changes depends upon the business and item, but can be as often as every day or even every hour.”

Instead of having prices dependent only on supply, demand and potentially location, dynamic pricing relies on advanced analytics on the product and, more importantly, the customer, to determine the optimal price for revenue management and relationship building.

While the roots of this concept go back decades, the power of dynamic pricing multiplied due to digital technology. Instead of physically changing the pricing on thousands of items (including changing displays), dynamic pricing can be applied in real-time … online. Done well, the most sought after customers of an organization receive the best pricing, generating better conversion rates.

Dynamic Pricing in Banking

Accustomed to the way pricing is handled by sports teams, entertainment venues, airlines, hotels and even companies like Uber and Regal Cinema, consumers expect personalized interactions and offers from all industries. This increasingly includes banking, where switching providers is becoming more commonplace. In fact, according to research from Accenture, 45% of consumers say the top reason that they would stay loyal is if their bank offered discounts on purchases of interest.

The increasing use of advanced analytics, including artificial intelligence and machine learning, provides the opportunity for banks and credit unions to develop personalized, real-time offers, matching immediate consumer needs with best-fit messaging and offers. This strategy is far superior to traditional product ‘packages.’

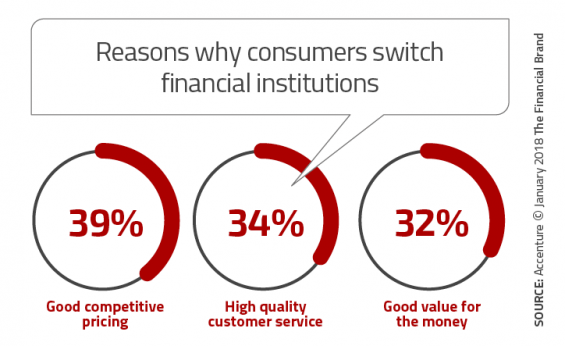

Pricing is the number one reason why consumers say they switch banks, according to a study from Accenture and Nomis. Competitive pricing (39%) was considered a key reason for switching, followed by high quality customer service (34%) and getting a good value for the money (32%).

Consumers expect today’s digital pricing models to adjust to real-time market conditions. Dynamic pricing should provide the right price, to the right consumer, at the right time. It should be contextual in nature, leveraging consumer demand and even location. Lastly, dynamic pricing should be integrated across channels.

Consumers expect today’s digital pricing models to adjust to real-time market conditions. Dynamic pricing should provide the right price, to the right consumer, at the right time. It should be contextual in nature, leveraging consumer demand and even location. Lastly, dynamic pricing should be integrated across channels.

The benefits of a dynamic pricing strategy mentioned by Crealytics include:

- Immediacy: Using real-time data allows an organization to improve the balance between conversion projections and margins. Using digital channels, the impact of different pricing models can be measured immediately, allowing for adjustment.

- Competitiveness: Old-time bankers like myself remember doing price shopping of competitive banks and credit unions to be reviewed by the asset/liability committee. While the shopping of local rates and prices has definitely moved beyond shops done by phone, advanced analytics can now be applied to make the needed changes in pricing immediately in response to changes by competitors. This is exactly what Amazon does 2.5 million times every day.

- Improved Cross-Sell and Conversion Rates: Increased customer and member insight can help financial organizations understand how someone has responded in the past, allowing for ‘loss leader’ pricing that will yield broader relationship ‘wins.’

- Pricing Flexibility: Does your organization want increased margins, better overall revenues or a maximized number of new customers? Dynamic pricing, combined with digital delivery, provides the flexibility to price each household accordingly.

- Improved Understanding of Trends: Do market conditions result in more consumers visiting specific website locations? Dynamic pricing allows an organization to aggressively price specific services based on localized market trends.

The ability to price based on an overall relationship (including personal, small business, wealth management, lending, and commercial accounts, etc.), is logical to today’s digital consumer. Organizations can build a strategy so that valuable customers and members never say, “I have very large relationships with your bank/credit union. Why should I get the same price/rate as everyone else?”

The key to dynamic pricing, however, is the ability to open an account immediately … on digital channels. As the name implies, dynamic pricing is a ‘point-in-time’ pricing, with the benefits negated if a consumer can’t open an account immediately, using the channel of choice.

Read More: A Business Case for Dynamic Pricing in Banking

Three Stages of Pricing Maturity

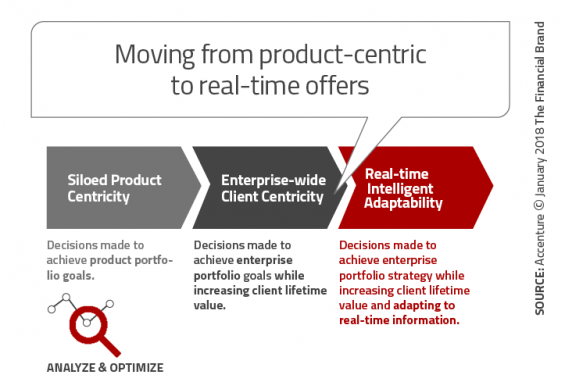

The Accenture research proposes that financial institutions fall into one of three stages of pricing and offer management maturity: product-centric, customer-centric and moment-centric. Each impacts the dynamics of the revenue model as well as the overall customer experience. According to Accenture, “Optimal pricing remains a primary goal across all stages as real-time offers are increasingly personalized, contextualized and dynamic through stage three.”

- Product-Centric: The first stage is where most banks and credit unions work from (90% of organizations are at this stage). In this stage, prices are based on product goals. This often ignores individual customer needs and the optimal customer lifetime value. ‘Next best offer’ strategies often are in this stage of pricing.

- Customer-Centric: This second stage of pricing maturity maximizes customer lifetime value across all product lines. This stage uses data and analytics to understand consumer needs, expectations and price sensitivity, predicting customer value. Some organizations use this model for individual products but not across all products. Product bundles are often part of this model.

- Moment-Centric: A real-time stage of pricing, Stage 3 enables conversations and offers based on immediate data and activity. Unlike the somewhat static nature of Stage 1 and Stage 2 pricing, this stage includes models that are continuously modified, immediately, based on interactions and activity. Application programming interfaces (APIs) will be key enablers in this stage.

Customer Insight, AI and Personalized Pricing

Understanding that most organizations are currently in an early stage of pricing maturity, there is a lot of work to be done to satisfy the increasingly demanding digital consumer. The digital consumer expects a personalized experience that reflects their needs and current relationship. Most banking organizations have the tools to meet these needs.

The foundation of dynamic pricing is a unified database or accessibility to the entire consumer relationship for analytic purposes. Using the insights and machine learning, models can be built to reflect the interactions of different data sets and the impact of different pricing scenarios on loyalty and organization revenue.

Finally, organizations need to move from models to mobility, pushing the pricing solutions to every channel the customer may interact with. In addition, banks and credit unions need to enable the opening of a new account through all channels without requiring moving to a branch or other channel.

There are a lot of non-banking examples of the power of dynamic pricing. It’s time to provide this level of personalization and relevance to bank and credit union customers/members.