Financial institutions increasingly find themselves between a rock and a hard place as they strive to remain competitive in consumer banking.

The “rock” is cybersecurity and identity theft. Data breaches seem an almost regular occurrence and ID theft grows more frequent. This makes reducing or preventing fraud a higher priority than ever.

The “hard place” is the demands of consumers. They insist on “pain-free,” seamless digital banking user experiences. Achieving that kind of experience becomes particularly difficult banking for providers because very often the steps needed to prevent digital fraud can detract from the user experience if not set up properly, leading to higher rates of abandonment.

Consumers want it all, and they’ll ditch anybody who can’t give it to them.

A survey by IDology found that a majority of consumers want three things when it comes to opening an account online (percent answering “extremely” or “very” important):

- A secure process: 88%

- An easy process: 67%

- A quick process: 57%

“Customers value security, but they also hate friction,” IDology states in a report. When the firm asked consumers how they felt about additional verification and security checks, three quarters said they strongly opposed added steps.

Dealing with that challenge may be part of the reason financial institutions have been slow in instituting account opening that’s completely on a mobile device. Research by the Digital Banking Report finds that 36% of banks and credit unions say they can do end-to-end mobile account opening now. That’s up sharply from 17% the year before, but, far too many institutions, particularly community banks, still require signatures, documentation, ID verification or even funding in a branch office to complete the account-opening process, according to Jim Marous, Owner/Publisher of the Digital Banking Report and Co-Publisher of The Financial Brand

Costs of Fraud Much More Than Financial

Reducing or preventing fraud is a top priority for seven out of ten financial institutions, according to a Forrester study. Considering that 61% of financial institution leaders reported an increase in fraud in 2018, that high level of attention isn’t surprising. Another firm, Risk Based Security, reports that through just the first six months of 2019, 3,813 data breaches were reported (in all industry sectors), exposing more than 4.1 billion records.

Forrester probed what steps financial institutions require consumers to take to authenticate. Top responses were: Enter date of birth (65%); Answer security questions (65%); Provide current or past address (59%).

The drawback with all of these steps, according to Forrester: All involve data that is either publicly available or could be deduced easily from social media. Further, they potentially annoy consumers by asking them to remember things they may have forgotten and have to look up. Result: poor security and poor experience.

Consumer Habits and Views on Identity Have Changed

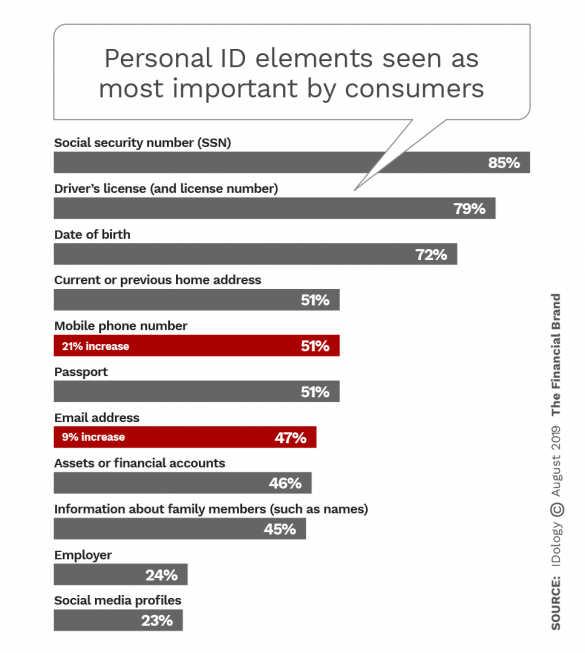

There has been a significant shift in what consumers include as part of their identity. In its study, IDology found that while Social Security number and driver’s license remain the two most important forms of personal identification for consumers, mobile phone numbers jumped in importance over the previous survey. They now rank among the top five identity elements.

As consumers’ sense of identity increasingly ties to their phones, financial institutions must not only work to create a superior mobile experience, but make mobile security and validation a priority, according to the report. The company points out that many organizations send account notifications and one-time passcodes directly to consumers’ mobile phones. That could be problematic as mobile phones are “relatively vulnerable.” Mobile fraud increased by 117% in 2018, according to the report.

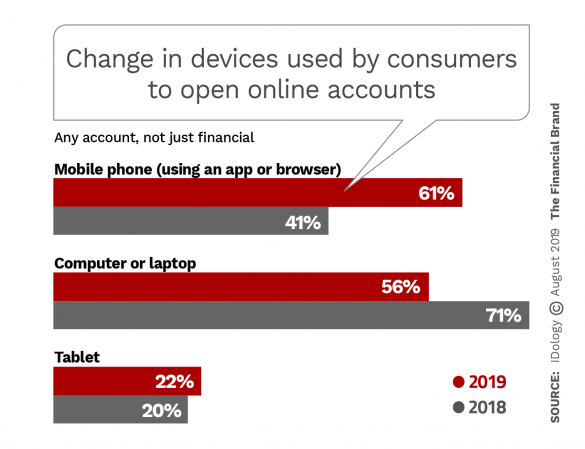

It’s a key issue because more and more consumers are using their mobile phone to open new accounts online. The chart below covers all types of new accounts, not just banking accounts. Mobile account opening exceeds online (PC) account opening. That’s not yet the case in banking, but is an indication of where things are headed.

Note that the figures for opening an account exclusively on one type of device are much lower, but still trending up: For example, 20% of U.S. consumers opened a new account exclusively on a mobile phone in 2018, double the previous year. In many cases banking customers still must come into a branch for either identity, signature, or other reasons to complete a new account application that was started on a mobile device.

Rise in Abandonment Seen in Digital Account Opening

When Apple and Goldman Sachs launched the Apple Card, the ease and speed of the application/enrollment process drew much attention. Some users reported times of three or even two minutes from opening the email invitation to beginning to purchase with the virtual card. While most financial institutions recognize the need for a quick and easy mobile application experience, just 16% allow a customer to open an account on a mobile device in under five minutes, according to Digital Banking Report findings.

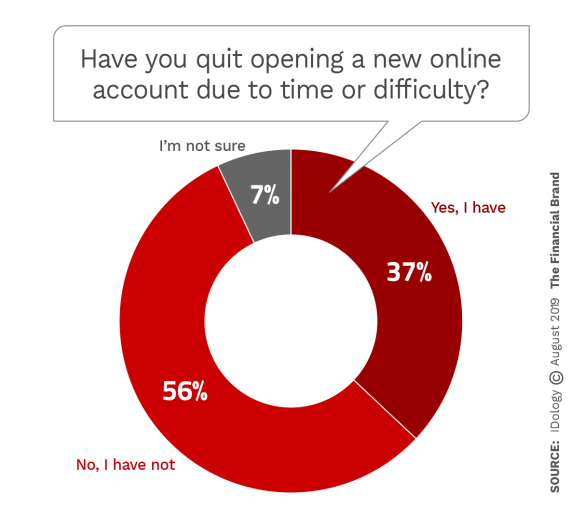

The IDology research confirms how important speed is now. Well over a third of consumers say they walked away from opening a new account either online or by mobile device in the previous 12 months. That response was a 19% increase year over year in online enrollment abandonment, the company states.

The data show that younger consumers are much more likely to abandon a frustrating enrollment process. Just over half (51%) of younger Millennials had done so and more than two out of five (42%) older Millennials had done so — much higher than the 29% of older Boomers who abandoned an application. It would appear that while younger consumers have better digital skills, they have far less patience for a less-than-optimal digital experience.

Some Ways Banks & Credit Unions Can Balance UX and Security

In many ways technology itself causes the disconnect between consumers’ desire for a seamless digital experience and for protection of their identity. But technology also points the way to striking the right balance.

In its research, IDology polled consumers about their comfort with various approaches to streamlining digital account opening. Surprisingly more than half (58%) said they would be very likely to enter the information manually. The problem with that, the company states, is that doing so is tedious and prone to mistakes. However, consumers are open to other approaches including prefilling information (42%) and mobile document capture (34%).

This willingness to use technology to enhance security is particularly relevant to financial institutions. The survey found that a little less than three quarters (71% ) of U.S. consumers say they would be more likely to use a bank or credit union that uses more advanced identity verification methods.

The “Much more likely” response was sharply higher over the previous year, IDology notes.

There are limitations, however. Nearly two in five consumers (39%) were very uncomfortable with having companies use social accounts for ID verification.

Forrester’s report emphasizes the benefits of integrating offline, online, and devised-based fraud prevention measures. As the firm states, to establish a complete view of any given consumer, financial institutions must “connect the dots between offline and online data to intercept abnormalities.”

To avoid detracting from the customer experience, Forrester recommends using implicit factors such as IP address geolocation, and behavioral elements — such as how a person swipes a mobile screen— which would minimize account opening complexity.

Both studies endorse the idea of escalating identity verification procedures as needed, but always streamlining processes as much as possible.